Part 2 continues the analysis from Part 1, moving beyond structure and market size to examine what lies ahead for India’s logistics industry.

Having understood the sector’s scale, segments, and competitive landscape, we now turn to the forces that will shape its next phase of growth. This section explores emerging opportunities, policy support, technology-led disruption, structural bottlenecks, and long-term investment implications—bringing clarity to where the industry is headed and how sustainable that growth trajectory truly is.

Opportunities: Unlocking Growth Potential

India's logistics sector presents numerous growth opportunities driven by structural reforms, technological adoption, and changing consumer behavior:

1. Infrastructure Development and Government Initiatives

The Indian government has launched several transformative initiatives that are reshaping the logistics landscape:

PM Gati Shakti National Master Plan is perhaps the most ambitious integration initiative, bringing together 44 ministries and 36 state/UT governments on a single digital platform. This ₹11.17 lakh crore initiative encompasses 434 projects focused on improving multimodal connectivity. The program has already evaluated 115 highway projects (~13,500 km) worth ₹6.38 lakh crores, dramatically reducing project delays and improving interministerial coordination.

National Logistics Policy (NLP) aims to reduce India's logistics costs from the current 13-14% of GDP to 8% by 2030, aligning with developed country benchmarks. The policy focuses on creating seamless multimodal transportation, standardizing warehousing facilities, and improving cross-border trade efficiency.

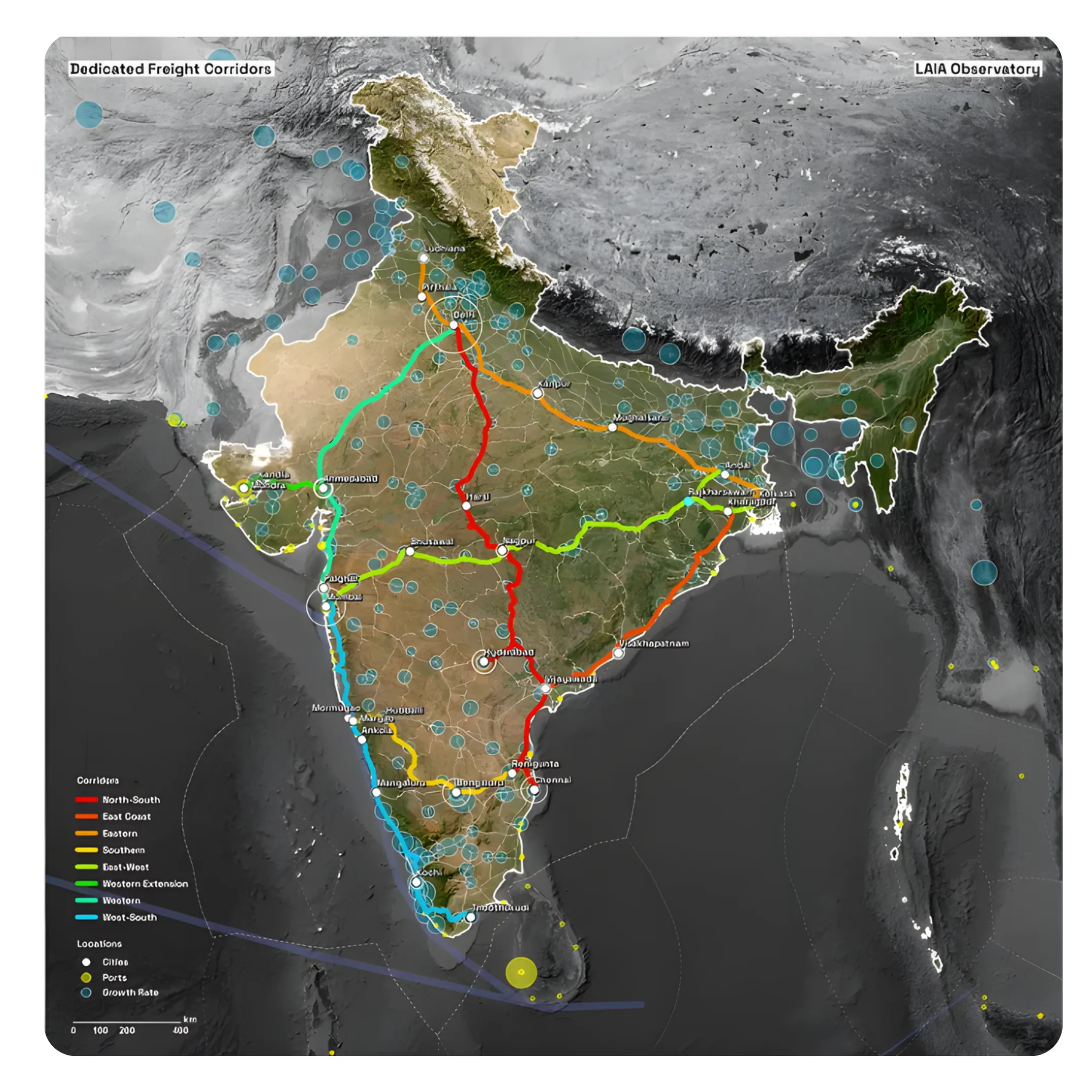

Dedicated Freight Corridors (DFCs): The Eastern and Western DFCs are now 96.4% operational, with 2,741 km commissioned out of 2,843 km. Average daily train movement has surged from 247 trains in FY24 to 352 trains in FY25. Three additional corridors (East-Coast, East-West, and North-South) are in the planning stage, with ₹45,000 crores sanctioned for the next phase.

Multimodal Logistics Parks (MMLPs): 35 MMLPs are planned under the Bharatmala Pariyojana with investments of approximately ₹46,000crores. These parks will handle around 700 million metric tonnes of cargo upon completion, dramatically improving transshipment efficiency.

Sagarmala Programme: This port-led development initiative has completed 272 projects worth ₹1.41 lakh crores out of 839 identified projects. The program has resulted in a 118% rise in coastal shipping and a 700% increase in inland waterway cargo, significantly easing road and rail congestion.

2. E-commerce Boom and Changing Consumer Behavior

India's e-commerce sector maintained strong growth with quick commerce accounting for about 65% of e-grocery orders in FY25, up from just 13% in 2022. This shift is creating massive demand for:

- Urban fulfillment centers with rapid processing capabilities

- Last-mile delivery infrastructure in Tier 2 and 3 cities

- Reverse logistics for returns management

- Technology platforms for real-time tracking

3. Manufacturing Growth through PLI Schemes

The Production-Linked Incentive (PLI) scheme has attracted ₹1.46 lakh crores in investments, enabled ₹12.5 lakh crores in production, and generated 9.5 lakh jobs across 14 sectors. This manufacturing boom creates sustained demand for:

- Inbound logistics for raw materials

- In-plant logistics and inventory management

- Distribution networks for finished goods

- Export-oriented freight forwarding

4. China+1 Strategy and Supply Chain Diversification

Global companies are actively diversifying supply chains away from over-dependence on China. India's relatively lower US tariff exposure (compared to China who faces significantly higher tariff exposure in key export categories compared to India) positions it attractive for foreign manufacturers. This trend is driving demand for:

- Industrial parks with integrated logistics

- Cross-border freight services

- Specialized warehousing near ports

- Customs clearance and compliance services

5. Technology Adoption and Digital Transformation

The logistics sector is rapidly embracing digital solutions:

- AI and Machine Learning: For demand forecasting, route optimization, and predictive maintenance

- IoT and Telematics: Real-time vehicle and cargo tracking

- Blockchain: Secure documentation and smart contracts

- Automation: Robotics in warehousing, automated sorting systems

- Data Analytics: Supply chain visibility and performance optimization

Mahindra Logistics, for example, reports that AI-driven logistics optimization and automated warehousing are becoming industry standards, improving operational efficiency significantly.

6. Green Logistics and Sustainability

Environmental consciousness is driving investment in green logistics:

- Electric Vehicles: Blue Dart operates a fleet of 549 electric vehicles for last-mile and long-haul deliveries

- Sustainable Aviation Fuel (SAF): Airlines and express carriers are incorporating SAF to reduce carbon footprint

- Green Warehousing: Solar-powered facilities, rainwater harvesting, energy-efficient designs

- Carbon Offsetting: Tree plantation initiatives (Aegis has planted over 888,000 trees)

As per industry forecast, the green logistics market in India is projected to expand at a CAGR of over 6% from 2025 to 2029.

For a deeper look at how disciplined execution and strategic shifts can reshape a company’s trajectory, read A Year of Execution and Strategic Transformation at Laurus Labs Ltd.

Challenges and Regulations: Navigating Complexity

Despite tremendous opportunities, the logistics sector faces several structural challenges:

1. High Logistics Costs

India's logistics costs at 13-14% of GDP remain significantly higher than the developed country average of 8-10%. This stems from:

- Modal Mix Imbalance: Over 60% reliance on road transport compared to a more balanced modal mix in many developed economies

- Fragmentation: Small operators lack economies of scale

- Infrastructure Bottlenecks: Inadequate multimodal facilities, port congestion

- Indirect Costs: Higher inventory carrying costs, theft, damage due to poor handling

2. Regulatory and Compliance Burden

While GST implementation simplified interstate movement by eliminating checkpoints, it introduced new compliance requirements:

- E-way Bill Compliance: Mandatory for interstate movement

- E-Invoicing: Now required for all businesses with turnover above ₹5 crores

- RCM on Rent: Reverse Charge Mechanism on rental premises has increased costs for logistics companies

- Vehicle Age Restrictions: Several cities prohibit entry of diesel commercial vehicles beyond certain age

- Environmental Regulations: Stricter emission norms requiring fleet upgrades

3. Skilled Workforce Shortage

The industry faces acute shortage of:

- Drivers: VRL Logistics identifies this as the single most important constraint affecting transporters nationwide

- Supply Chain Professionals: Limited talent in logistics management, data analytics, and automation

- Technical Staff: For maintaining modern automated warehouses and vehicles

4. Infrastructure Gaps

Despite improvements, significant gaps remain:

- Last-Mile Connectivity: Poor road conditions in rural and remote areas

- Warehousing: Shortage of modern, Grade A warehousing facilities

- Multimodal Integration: Limited seamless connectivity between road, rail, and ports

- Technology Infrastructure: Inconsistent digital connectivity in smaller towns

5. Fuel Price Volatility and Operating Costs

Fuel constitutes 27-30% of operating costs for road transporters. Price volatility creates margin pressures, though companies like VRL have established direct refinery tie-ups and company-owned fuel stations to mitigate this risk.

6. Taxation Challenges

GST Structure: While GST has simplified interstate movement, certain aspects remain complex:

- Transportation services attract 5% GST with limited input tax credit

- Reverse charge mechanism on various services

- Compliance burden for small operators

Other Taxes: States impose various local taxes, tolls, and fees that impact profitability

Innovation and Technological Disruption

The Indian logistics sector is witnessing unprecedented technological innovation:

Digitalization Initiatives

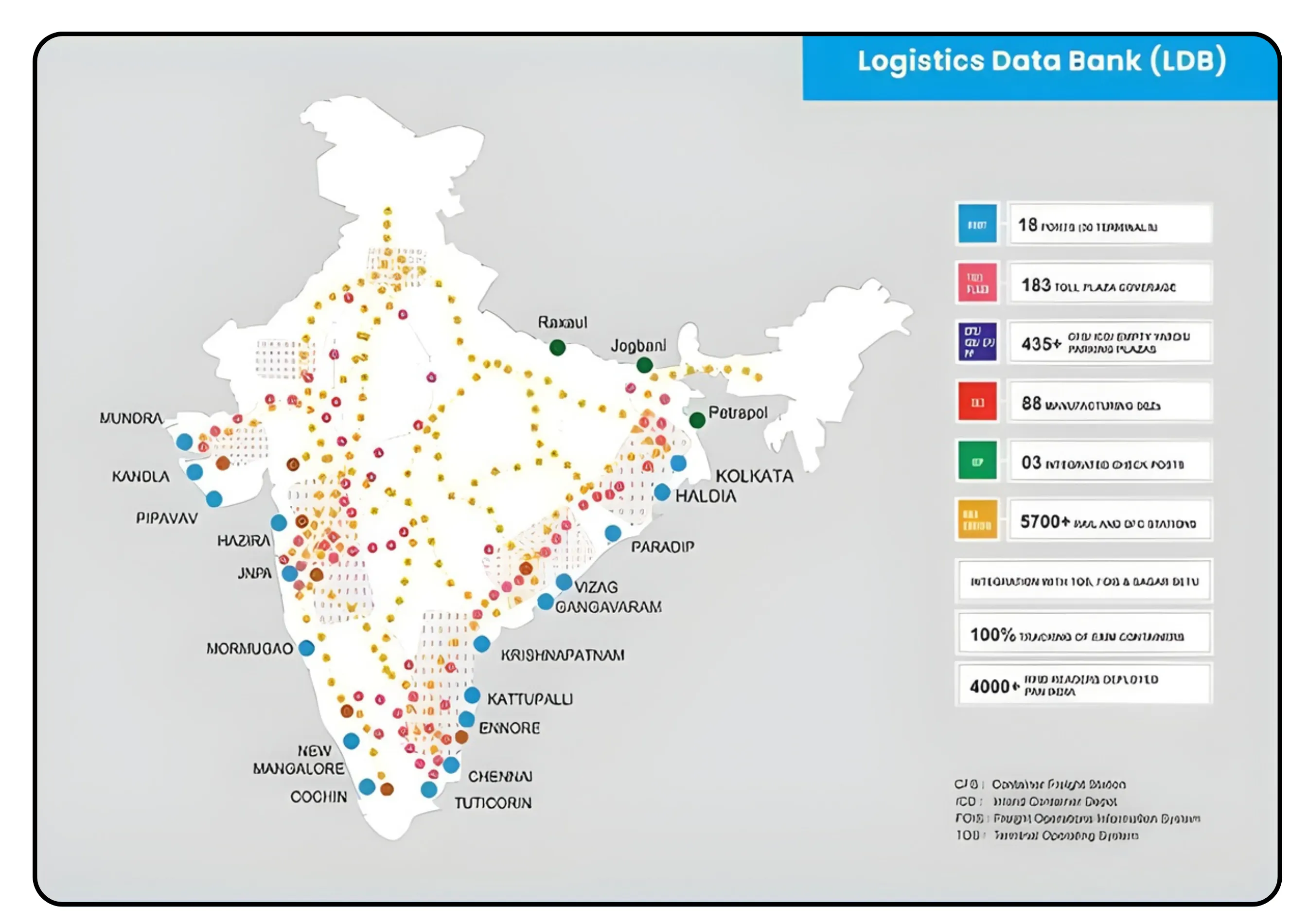

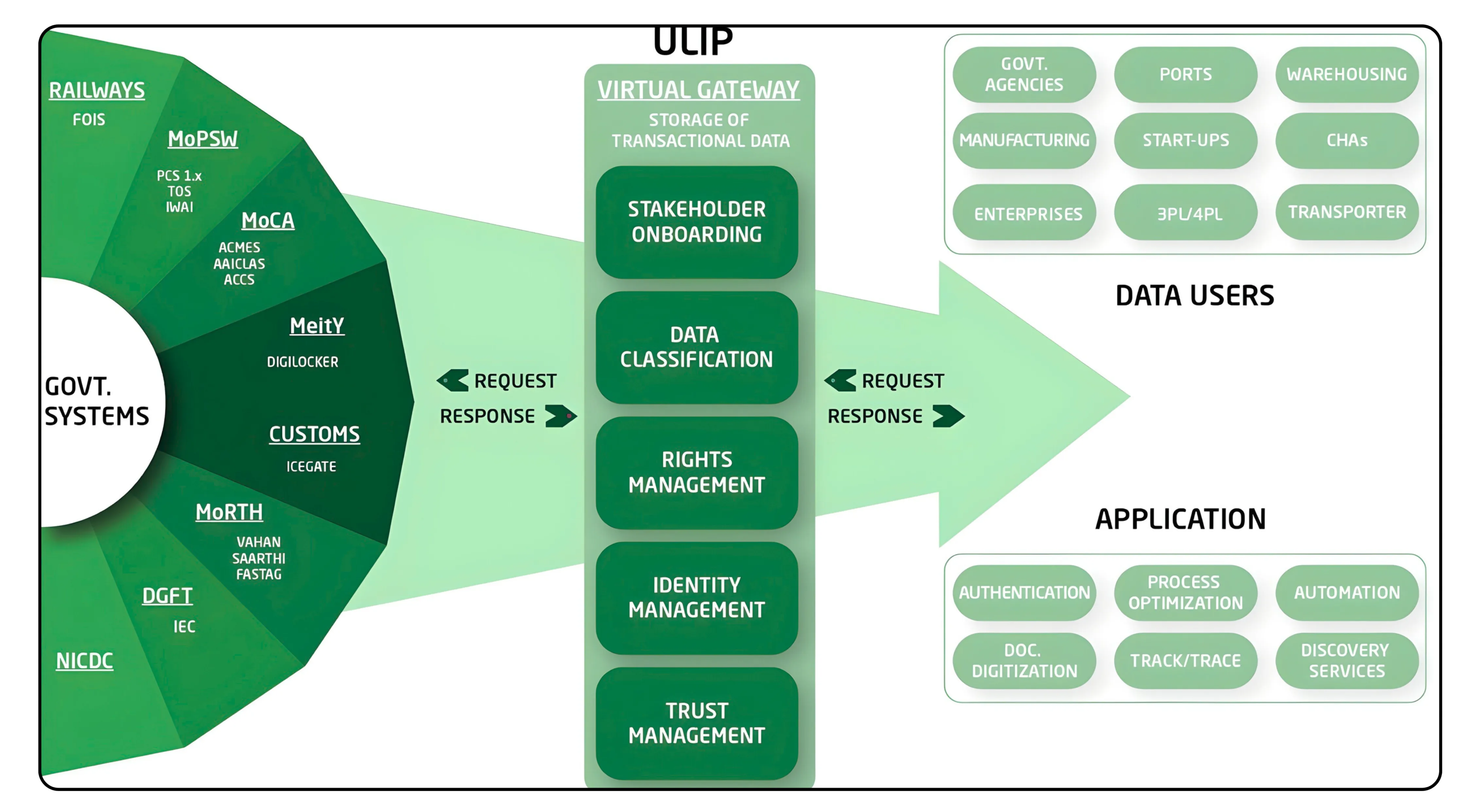

Unified Logistics Interface Platform (ULIP): Integrates 33 logistics-related systems across 10 ministries, enabling real-time cargo tracking through GST data. Over 930 private companies are registered, facilitating end-to-end visibility.

Open Network for Digital Commerce (ONDC): democratizing e-commerce by enabling small sellers to compete with major platforms. Hit a record 1.6 crore orders per month, creating new opportunities for logistics providers.

Drone Delivery and Future Tech

Blue Dart launched the Med-Express Consortium under the government's 'Medicine from the Sky' initiative, using drones to transport temperature-sensitive medical supplies to inaccessible regions. This showcases the potential for:

- Drone-based last-mile delivery in congested urban areas

- Medical emergency supplies to remote locations

- Disaster relief logistics

Automation and AI

Leading companies are deploying:

- Autonomous Vehicles: Pilot projects for self-driving trucks on highways

- Warehouse Robots: For picking, sorting, and inventory management

- Predictive Analytics: For demand forecasting and capacity planning

- Digital Twins: Simulating warehouse operations to optimize layout and processes

Geographical Growth Opportunities

Metro Cities: Gateway to Growth

India's metro cities (Mumbai, Delhi, Bangalore, Chennai, Hyderabad, Kolkata) continue to generate the highest logistics demand due to:

- Manufacturing concentration

- Port connectivity

- Consumer density

- Technology adoption

Companies like Blue Dart operate at full capacity in Mumbai terminals, indicating sustained demand.

Tier 2 and Tier 3 Cities: The New Frontier

The most exciting growth opportunities lie in smaller cities:

- Consumer Growth: Rising incomes and digital penetration in cities like Surat, Coimbatore, Vizag, Jaipur

- Manufacturing Expansion: Industrial clusters emerging in tier-2 cities

- E-commerce Penetration: Quick commerce expanding beyond metros

- Infrastructure Development: Government focus on regional connectivity

VRL Logistics added 97 new branches in FY25, primarily in tier-2 and tier-3 locations, driving tonnage growth. Mahindra Logistics reports strengthening regional connectivity as a key strategy.

Coastal and Port Cities

With 14 major ports and over 200 minor ports, coastal cities offer tremendous potential:

- New Mangalore, Kandla, JNPA (Navi Mumbai), Haldia seeing capacity expansions

- Sagarmala program enhancing port infrastructure

- Coastal shipping gaining traction as a sustainable alternative

Aegis Logistics commissioned new terminals at Mangalore (75,230 m³ capacity) and JNPA (1,01,900 m³ capacity) during FY25, indicating strong port-centric growth.

Border and Hinterland Regions

Cross-border trade with Bangladesh, Nepal, Bhutan, and Myanmar presents opportunities, though geopolitical considerations (like the India-Pakistan trade freeze) remain factors.

Potential Clients: Who Needs Logistics Services?

The client base for logistics services spans virtually every sector of the economy:

Manufacturing Sector

- Automotive: OEMs and component suppliers requiring inbound, in-plant, and outbound logistics

- Consumer Durables: Appliances, electronics needing distribution networks

- Industrial Equipment: Heavy machinery, capital goods requiring specialized handling

- Textiles and Apparel: Fashion logistics with seasonal spikes

FMCG and Retail

- Packaged Foods: Distribution to millions of retail outlets

- Personal Care and Cosmetics: Temperature-controlled warehousing and distribution

- Modern Retail Chains: Just-in-time inventory management

E-commerce

- Marketplaces: Amazon, Flipkart, Meesho requiring nationwide fulfillment

- Quick Commerce: Blinkit, Zepto, Swiggy Instamart for hyperlocal deliveries

- D2C Brands: Direct-to-consumer businesses needing integrated solutions

Pharmaceuticals and Healthcare

- Drug Manufacturers: Temperature-controlled logistics, regulatory compliance

- Medical Equipment: Specialized handling and installation

- Hospitals and Clinics: Regular supply chain for consumables

Agriculture and Commodities

- Food Processing: Cold chain from farm to processor

- Fertilizers and Seeds: Seasonal distribution to rural areas

- Commodities Trading: Bulk transportation of grains, pulses

Industrial and B2B

- Chemicals: Specialized hazardous materials handling (Aegis Logistics' strength)

- Metals and Mining: Bulk cargo movement

- Energy: LPG distribution, petroleum products

To understand how an asset-driven model works in capital-intensive sectors, read Seamec Ltd Operating an Asset-Driven Offshore Services Business for a closer look at execution, utilization, and return dynamics.

Capital Expenditure and Return on Investment

Industry CAPEX Trends

The logistics sector requires substantial capital investment across multiple areas:

Warehousing Infrastructure: Grade A warehouses cost approximately ₹2,500-3,500 per square foot to develop. With companies expanding footprints significantly (Mahindra Logistics operates 5 million sq ft of BTS warehouses), individual facility investments can range from ₹50-200 crores.

Fleet Acquisition: Modern commercial vehicles cost ₹30-50 lakhs each. VRL Logistics operates 6,115 owned vehicles representing an investment of approximately ₹2,000-2,500 crores. Companies balance owned vehicles with hired fleet based on ROI considerations.

Technology Systems: ERP, WMS, TMS, and tracking systems require ₹10-50 crores for large operators, with ongoing maintenance costs.

Automation Equipment: Conveyor systems, sorting machines, AGVs (Automated Guided Vehicles) for warehouses can add ₹20-100 crores per facility.

Return Profiles

Different logistics segments offer varying return profiles:

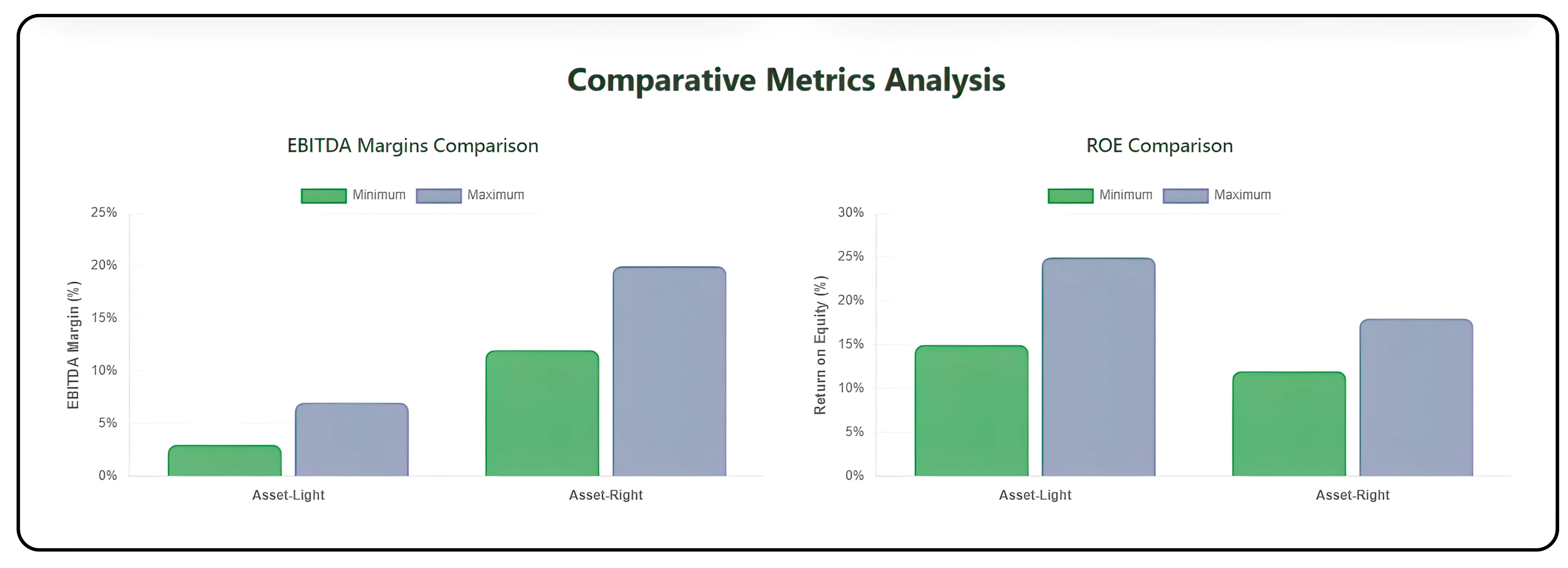

Asset-Light Models (Freight Forwarding, Brokerage):

- Lower capital intensity

- EBITDA margins: 3-7%

- ROE: 15-25%

- Faster scalability

Asset-Right Models (Owned Fleet, Warehouses):

- Higher capital requirements

- EBITDA margins: 12-20% for specialized services

- ROE: 12-18%

- Better control and customer stickiness

Example Returns from Major Players (FY25):

- Blue Dart: 16% Return on Equity, 6% Return on Investment

- Aeg Vopak: 15.56% Return on Net Worth

- TVS Supply Chain: 4.7% ROCE (Return on Capital Employed)

The organized players demonstrate that while logistics is capital-intensive, professional management and scale can deliver attractive returns.

A Sector Poised for Transformation

India's logistics industry stands at an inflection point. The convergence of supportive government policies, infrastructure investments, technology adoption, and formalization is creating a once-in-a-generation opportunity. While challenges like high costs, fragmentation, and skilled workforce shortages persist,the long-term structural direction appears constructive, subject to execution.

For businesses, the message is clear: partnering with organized, technology-enabled logistics providers can unlock significant supply chain efficiencies and cost savings. For investors, the sector offers attractive growth prospects backed by structural tailwinds. For job seekers, logistics presents diverse career opportunities from technology roles to operations management.

As India marches toward its goal of becoming a $5 trillion economy and eventually a developed nation, a world-class logistics infrastructure will be non-negotiable. The foundations are being laid today, and the companies and professionals who participate in this transformation will reap substantial rewards in the decades to come.

Turn research into action, trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.