Seamec Ltd operates in the offshore marine services segment, providing specialised vessels and crews that support the maintenance, repair, and construction of subsea oil and gas infrastructure. Its work includes inspection and upkeep of underwater pipelines, platforms, risers, and related offshore assets, activities that are essential once an oilfield is already producing.

Incorporated in 1986 and later integrated into global offshore ecosystems through ownership under the Technip Group, Seamec acquired technical depth and operating discipline early in its life. Since returning to Indian ownership, the business has increasingly aligned itself with long-duration domestic offshore activity, particularly projects led by ONGC and large engineering contractors.

Today, Seamec functions as an asset-led operator. Its revenues are driven not by volumes or pricing power in a conventional sense, but by vessel availability, technical capability, and contract tenure. Offshore contracts are typically structured around daily charter rates, with earnings determined by how consistently vessels remain deployed across operating seasons. Periods of dry-docking, weather-related downtime, or technical issues can therefore create visible fluctuations in quarterly performance, even when long-term demand remains intact.

A notable feature of Seamec’s evolution has been its increasing focus on higher-value subsea work, particularly inspection, maintenance, and repair (IMR) activities. These services command better margins than basic support work because they require specialised vessels, certified crews, and strict compliance with safety and operational standards. Over time, this shift has contributed to structurally higher operating margins compared to the pre-COVID period, when the fleet was older and service mix was less favourable.

Listed on the National Stock Exchange and BSE, Seamec Ltd has a market capitalisation of ₹ 2,821 Cr, and it’s a niche offshore oilfield services company in India.

From an equity market perspective, Seamec Ltd’s share price has historically tracked vessel deployment cycles and charter hire visibility rather than short-term quarterly earnings, with investors often focusing on operating stability over headline growth.

Business Model and Operations

Seamec Ltd earns its revenues by deploying specialised offshore vessels under time-bound charter contracts. The economic engine of the business is simple in structure but demanding in execution: each vessel generates income when it is operational, certified, and deployed at sea. Idle days, whether due to weather, dry-dock schedules, or technical issues, translate directly into foregone revenue.

How the Fleet Earns

Seamec’s fleet primarily consists of diving support vessels (DSVs) and offshore support vessels (OSVs). These vessels are used in the post-exploration phase of offshore oil and gas activity, where existing fields require continuous upkeep rather than discovery drilling.

Core Services Overview

| Service Area | Description |

|---|---|

| Inspection, Maintenance and Repair (IMR) | Inspection, maintenance, and repair of subsea pipelines, platforms, risers, and mooring systems supporting producing offshore oilfields |

| Subsea Construction Support | Vessel and crew support for subsea construction and installation activities, including positioning and handling of underwater infrastructure |

| ROV Support Services | Deployment support for remotely operated vehicles used in inspection, intervention, and underwater maintenance tasks |

| Offshore Accommodation and Logistics | Accommodation and logistical support for offshore crews engaged in long-duration marine and subsea operations |

IMR work forms the economic backbone of the business. Once an offshore field is operational, inspection and maintenance are non-discretionary. Pipelines corrode, equipment degrades, and safety standards mandate regular intervention. This creates recurring demand that is less sensitive to short-term oil price movements than exploration activity.

Contract Structure and Revenue Visibility

Contracts are typically awarded on a charter hire basis, where the client pays a fixed daily rate for the vessel along with crew and defined services. The duration can range from a few months to multiple years, depending on project scope.

Two aspects of these contracts are central to understanding Seamec’s financials:

Utilisation matters more than pricing

A modestly priced vessel that operates consistently often generates better economics than a higher-rate vessel with intermittent deployment.

Downtime risk is asymmetric

While operating costs such as crew and maintenance continue during downtime, revenue does not. This explains why quarterly earnings can swing sharply even when annual demand remains intact.

Penalties may apply in certain contracts, particularly with large public-sector clients, if vessels are unavailable due to breakdowns. As a result, preventive maintenance and fleet reliability are not just operational priorities but financial safeguards.

Cost Structure and Operating Leverage

Seamec’s cost base is largely fixed in the short term. Crew wages, certification costs, insurance, and maintenance do not scale down easily when a vessel is idle. This creates operating leverage in both directions: margins expand meaningfully during periods of high deployment, but compress quickly when utilisation drops.

The company has partially mitigated this risk by upgrading its fleet over time. Newer vessels typically incur lower maintenance costs and are better suited for higher-margin work, improving profitability across a full cycle.

Subsidiaries and Non-Core Activities

Beyond offshore services, Seamec has exposure to bulk carriers and has previously ventured into infrastructure construction through joint ventures. These activities provide optionality but remain secondary to the offshore services segment, which continues to drive the bulk of capital employed and cash generated.

Financial Performance and Five-Year Trends

Seamec’s financial statements over the last five years reflect a business emerging from a prolonged downcycle into a phase of higher utilisation and improving financial stability. The numbers show improvement, but not in a straight line, and that unevenness is central to understanding the company.

Related reading: ABS Marine Anchoring Growth with Long-Term Offshore Contracts explores how long-term offshore contracts drive stability in asset-led marine businesses.

Profit and Loss Overview

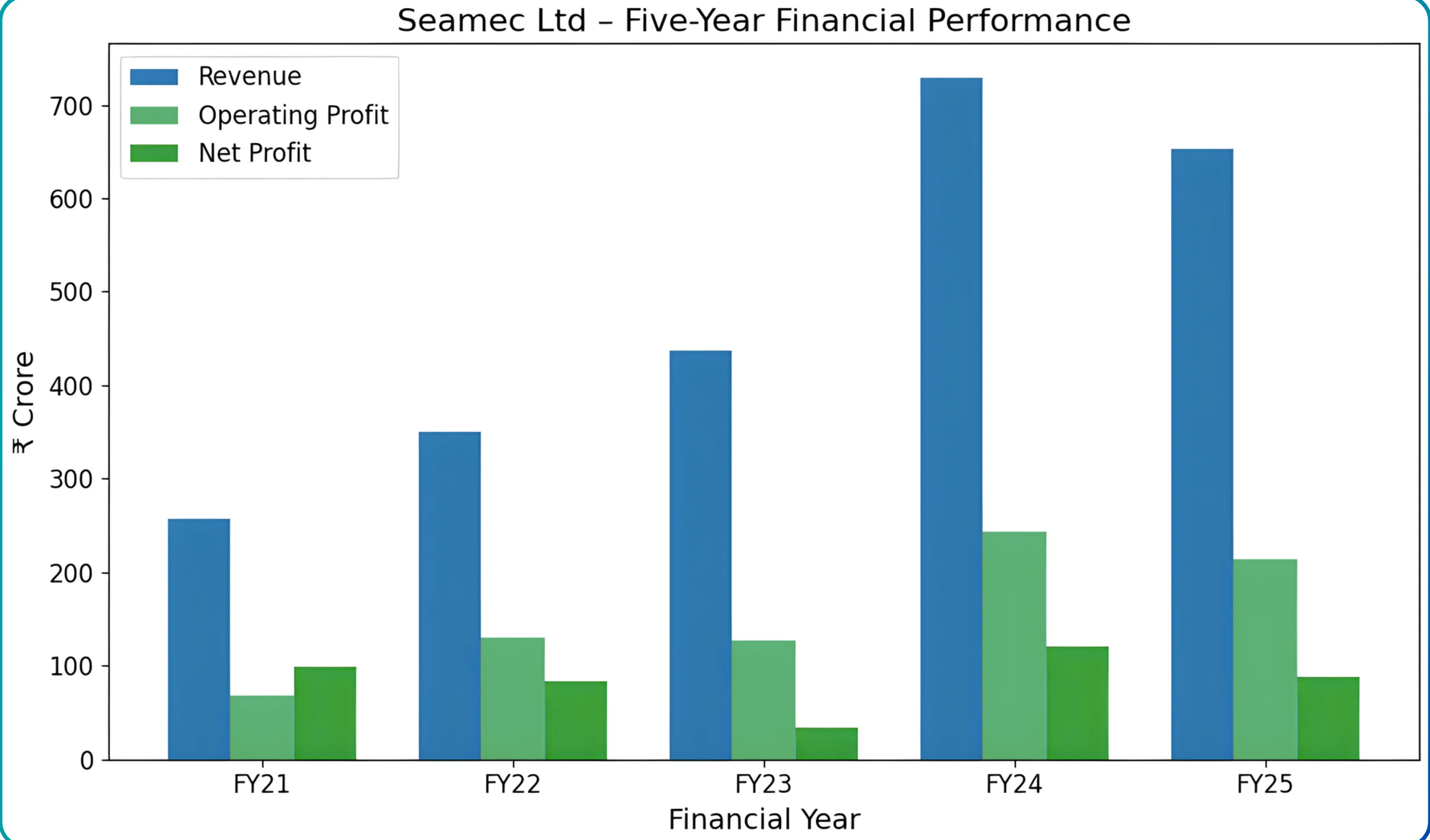

Table: Profit and Loss Summary (₹ crore)

| FY | Revenue | Operating Profit | OPM % | Net Profit |

|---|---|---|---|---|

| FY21 | 257 | 68 | 26% | 99 |

| FY22 | 350 | 130 | 37% | 84 |

| FY23 | 437 | 127 | 29% | 34 |

| FY24 | 729 | 243 | 33% | 121 |

| FY25 | 652 | 214 | 33% | 88 |

Over the past year, profitability has remained sensitive to deployment timing, reinforcing the importance of viewing quarterly results in conjunction with longer-term operating trends.

Revenue growth during this period has been driven primarily by higher vessel deployment rather than incremental pricing. FY24 marked a clear step-up in scale as newly inducted vessels and improved utilisation came together, while FY25 saw a moderation in topline largely due to timing and operational factors rather than a deterioration in demand.

Operating margins tell a more important story than revenues. Since FY21, margins have remained structurally higher than pre-COVID levels, consistently operating in the high-20s to low-30s range. This reflects a combination of better fleet quality and a higher proportion of inspection, maintenance, and repair work, which typically commands superior economics.

Net profit, however, remains volatile. The divergence between operating profit and reported earnings is largely explained by depreciation and, to a lesser extent, tax variability. This reinforces the need to interpret profitability through operating metrics rather than headline PAT alone.

Recent Financial Performance: Q2 FY26 and H1 FY26 Snapshot

Recent quarterly numbers highlight the inherently uneven nature of Seamec’s operations. Q1 FY26 benefited from strong vessel deployment, reflected in higher revenue, EBITDA, and cash profit. This momentum moderated in Q2 FY26, where revenue and profitability declined sequentially, largely due to timing of contracts and operational factors rather than a structural slowdown.

On a half-year basis, however, the picture is more stable. H1 FY26 revenues were broadly in line with the previous year, while EBITDA and cash profit showed improvement, indicating that operating efficiency and cost control remain intact despite quarterly volatility. Seamec’s performance is best assessed over multi-quarter periods, where deployment cycles and operating leverage become clearer, rather than through isolated quarterly comparisons.

Balance Sheet and Capital Structure

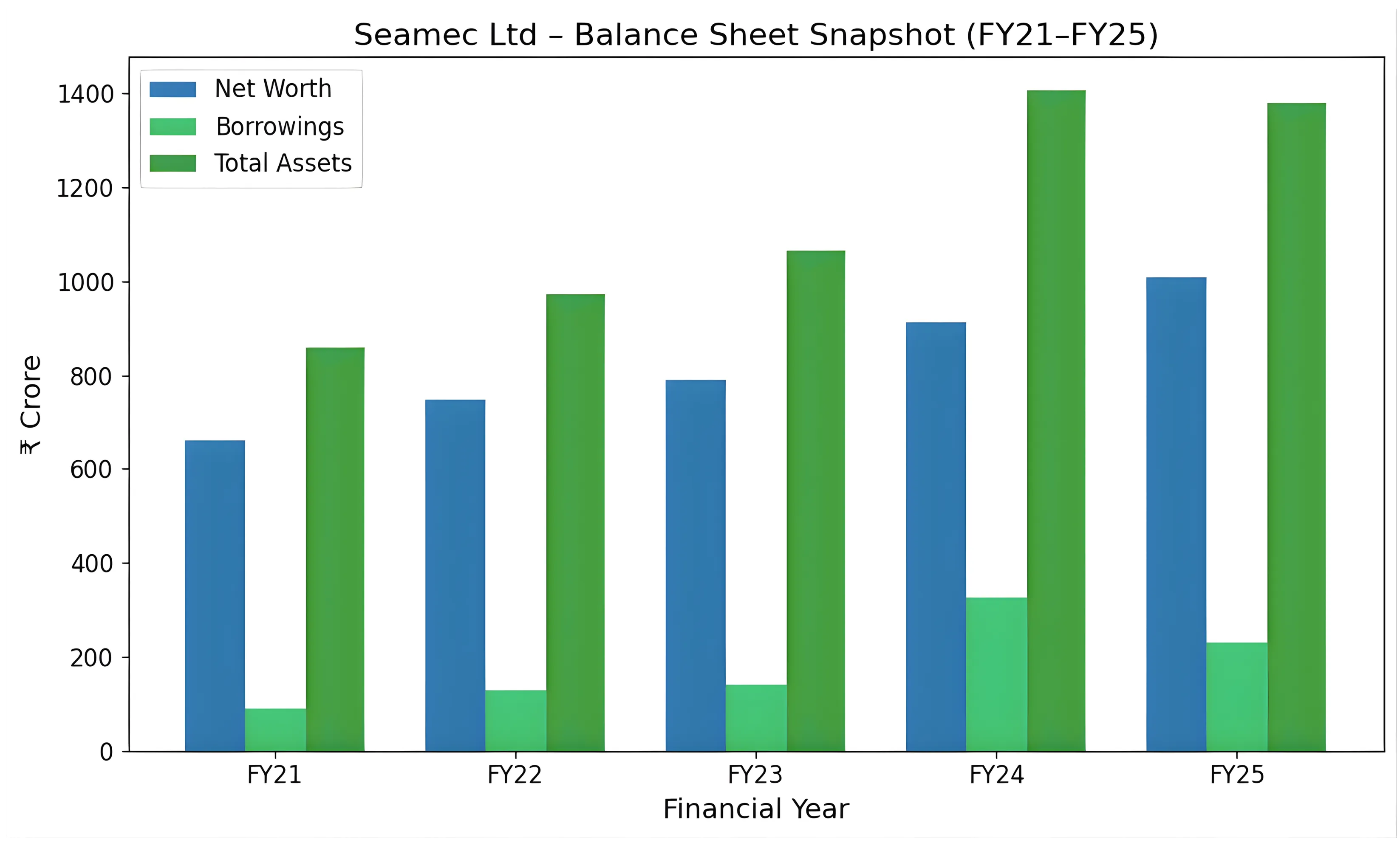

Table: Balance Sheet Snapshot (₹ crore)

| FY | Net Worth | Borrowings | Total Assets |

|---|---|---|---|

| FY21 | 662 | 89 | 859 |

| FY22 | 748 | 127 | 971 |

| FY23 | 790 | 139 | 1,064 |

| FY24 | 911 | 327 | 1,407 |

| FY25 | 1,007 | 231 | 1,379 |

From a valuation standpoint, book value and balance-sheet strength remain relevant reference points, given the asset-intensive nature of offshore marine services.

The balance sheet expansion over this period reflects deliberate capital allocation rather than balance-sheet stress. Borrowings rose sharply in FY24 as the company invested in fleet additions, a move that also explains the concurrent increase in fixed assets.

Importantly, the growth in assets has been accompanied by a steady increase in net worth, indicating that expansion has not been pursued at the cost of financial stability. While leverage rises during investment phases, it remains linked to identifiable, income-generating vessels rather than working-capital support.

This pattern is consistent with an asset-led offshore business, where returns are realised over multi-year operating cycles rather than immediately after capital deployment.

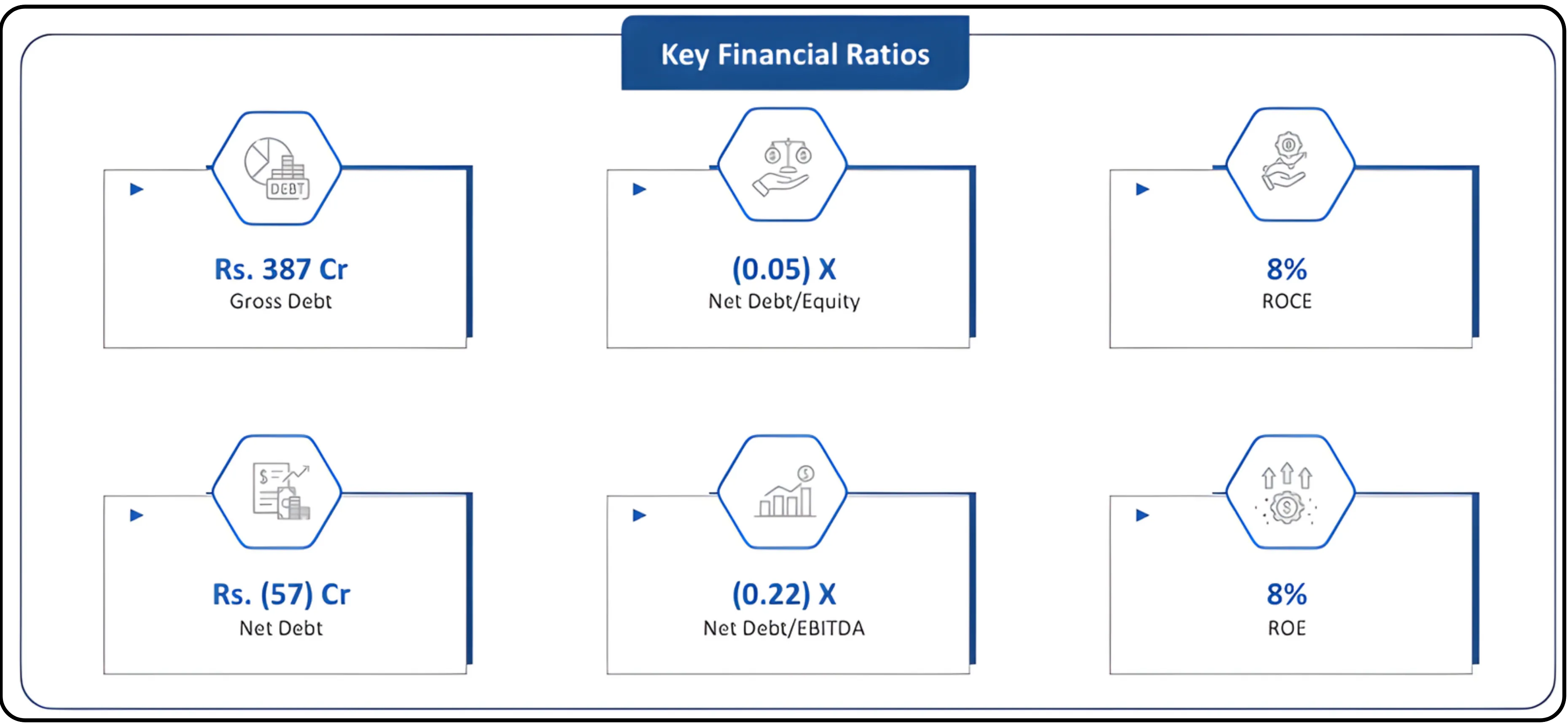

As of H1 FY26, Seamec’s balance sheet remains conservative despite recent fleet investments. Gross debt stood at ₹387 crore, while net debt turned marginally negative at ₹57 crore, reflecting strong operating cash flows and improved liquidity. Leverage metrics remain comfortable, with net debt to EBITDA at 0.22x and a net debt to equity position close to neutral. Return ratios continue to be modest, with ROCE and ROE at around 8%, underscoring the capital-intensive nature of the business even as operating conditions improve.

Related reading: India’s Maritime Economy — Complete Sector Analysis (Part 1/3) provides a broader view of shipping, offshore services, and port-linked activity across the Indian maritime ecosystem.

Cash Flow Profile

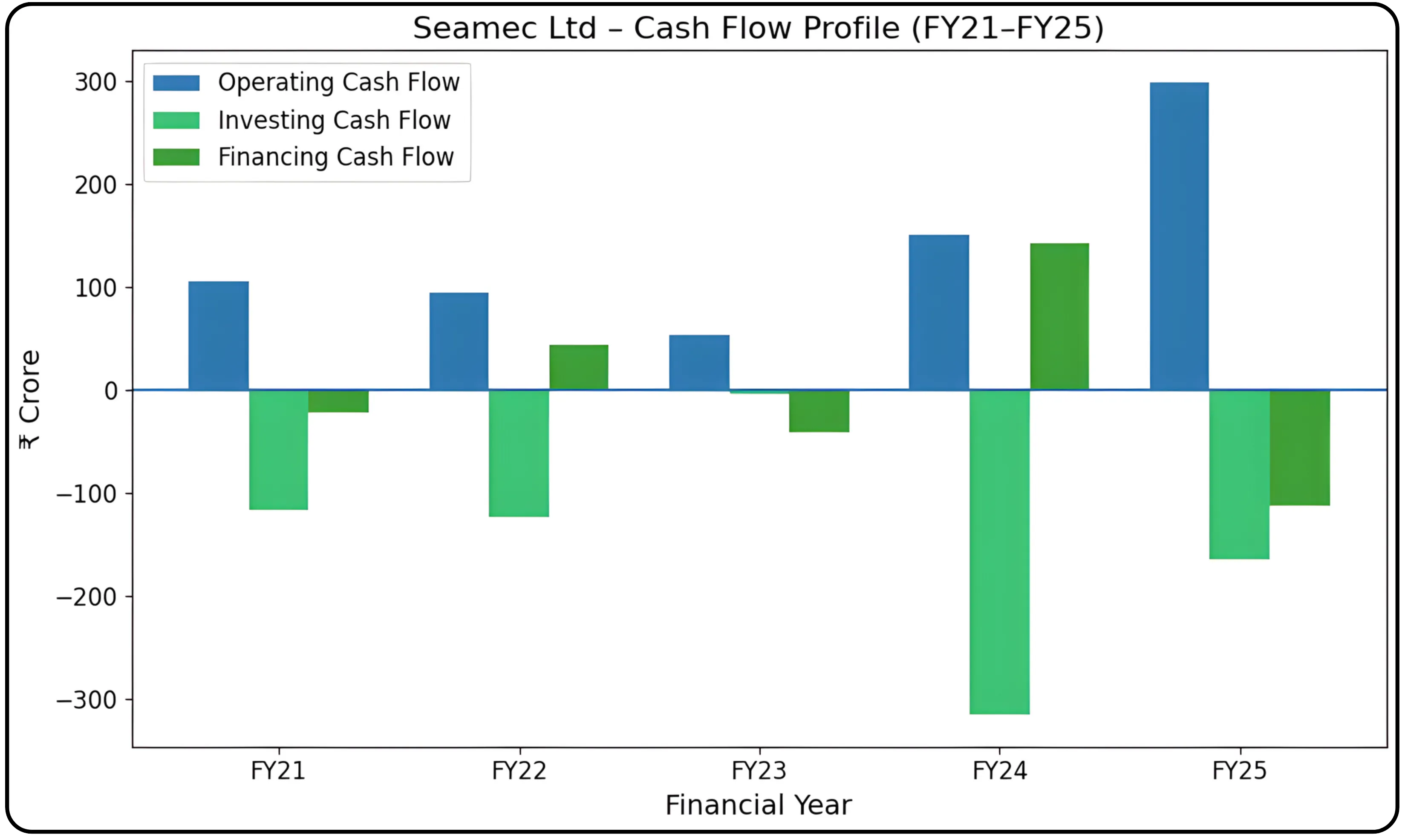

Table: Cash Flow Summary (₹ crore)

| FY | Operating Cash Flow | Investing Cash Flow | Financing Cash Flow |

|---|---|---|---|

| FY21 | 106 | -117 | -22 |

| FY22 | 94 | -124 | 43 |

| FY23 | 53 | -5 | -42 |

| FY24 | 150 | -316 | 142 |

| FY25 | 299 | -165 | -112 |

Operating cash flows broadly track deployment cycles, with stronger inflows visible in periods of stable vessel utilisation. The sharp improvement in FY25 reflects improved operating performance and working capital normalisation.

Investing cash flows show pronounced volatility, which is expected in a business where capital expenditure is concentrated around vessel acquisitions and upgrades. The significant outflow in FY24 corresponds with fleet expansion, while FY25 reflects a tapering of capex intensity.

Financing cash flows mirror this pattern. Debt was raised to fund expansion and subsequently moderated as cash flows improved. There is little evidence of sustained reliance on external funding to support operations, suggesting that the business remains internally cash-generative over a full cycle.

Working Capital and Capital Efficiency Context

Receivable days and cash conversion cycles have historically been elongated, reflecting the nature of offshore contracts and public-sector counterparties. Over the past few years, these metrics have shown improvement, particularly during periods of higher utilisation, indicating better cash discipline rather than a fundamental change in contract structure.

Return on capital employed has improved from earlier lows but remains moderate, constrained by the capital-intensive nature of the business and periodic underutilisation. This is not unusual for offshore marine services and underscores why valuation must be approached through cycle-aware metrics rather than peak-year returns.

Industry Context and Operating Environment

Seamec operates within a narrow but strategically important segment of India’s energy infrastructure. Offshore marine services sit downstream of exploration and drilling and upstream of production continuity. Once an offshore field is commissioned, the requirement for subsea support vessels becomes structural rather than optional.

India’s Offshore Landscape

India’s offshore oil and gas activity is concentrated largely in mature producing basins, most notably Mumbai High and the western offshore region. Unlike frontier exploration zones, these fields demand ongoing intervention: pipelines must be inspected, risers repaired, moorings maintained, and safety systems periodically upgraded. This creates steady demand for specialised offshore vessels even when upstream capital expenditure moderates.

Public-sector operators, particularly ONGC, remain central to this ecosystem. Their contracting approach favours compliance, technical capability, and proven operating history over short-term pricing. For operators like Seamec, this results in fewer but longer and more structured contracts, with relatively high entry barriers for new participants.

Cyclicality, but of a Different Kind

Offshore marine services are cyclical, but the cycle differs from conventional shipping or drilling services.

- Demand is less sensitive to short-term oil price fluctuations

- Activity is influenced more by field maturity, maintenance schedules, and regulatory compliance

- Seasonal factors such as monsoon-related downtime affect timing, not long-term necessity

This distinction explains why offshore support businesses often exhibit uneven quarterly results while maintaining reasonable earnings visibility over multi-year periods.

Capacity Constraints and Barriers to Entry

The supply side of the industry is constrained by long asset lead times. Building or acquiring a specialised diving support vessel is capital-intensive and time-consuming. New vessels can take several years to deliver, and second-hand assets are limited in availability.

Operational barriers further restrict entry:

- Stringent safety and certification requirements

- Experienced crew availability

- Track record with large operators

These factors reduce the risk of rapid oversupply, particularly in the niche segments where Seamec operates.

Competitive Positioning

Within India, the number of operators capable of undertaking complex subsea and inspection work is limited. While international players exist, domestic operators with compliant fleets and local execution capabilities are better positioned for long-duration contracts with Indian clients.

Seamec’s positioning reflects this reality. Its relevance does not come from fleet size alone, but from the combination of vessel capability, operating history, and the ability to remain deployed across extended periods.

Structural Tailwinds and Constraints

Long-term energy transition narratives often obscure an important reality: offshore infrastructure, once built, must be maintained regardless of future exploration plans. Even as energy mixes evolve, existing offshore assets continue to require inspection and repair over their productive lives.

At the same time, the industry remains capital-intensive and operationally unforgiving. Returns are shaped as much by execution discipline as by market demand. This places a premium on balance-sheet management and fleet reliability.

Also read: A Fundamental Perspective of the Indian Alcohol Industry offers a sector-level view of demand drivers, regulation, and profitability across India’s alcoholic beverages market.

Valuation Metrics Snapshot (Including P/E Ratio & Book Value)

Table: Valuation and Operating Metrics

| Metric | Value |

|---|---|

| Market Capitalisation | ₹2,755 crore |

| Enterprise Value | ₹3,000 crore |

| EV / EBITDA (TTM) | 11.6x |

| Median EV / EBITDA (10-year) | 9.7x |

| P/E (TTM) | 31.3x |

| Median P/E (10-year) | 29x |

| Price to Book Value | 2.56x |

| Median P/B (10-year) | 2.2x |

| ROCE (FY25) | 9% |

| Operating Margin (TTM) | 35% |

The current P/E ratio and P/B ratio should therefore be read in the context of capital intensity, depreciation cycles, and historical return profiles rather than as standalone indicators.

Interpreting the Numbers

The current EV/EBITDA multiple sits modestly above the company’s long-term median. Historically, Seamec has traded at higher multiples only when vessel utilisation was elevated, contract visibility extended beyond twelve months, and balance-sheet leverage was either stable or declining. The present multiple suggests that the market is recognising the improvement in operating margins and fleet quality, but is not extrapolating these conditions indefinitely.

The P/E multiple, while optically high, reflects the accounting reality of heavy depreciation and timing differences in profit recognition. When assessed alongside operating margins and cash flows, the valuation appears less stretched than headline earnings metrics suggest.

Price-to-book provides an important cross-check. The premium to historical averages aligns with the replacement cost of modern offshore vessels and the gradual shift toward higher-value subsea services. However, the multiple does not yet imply peak-cycle optimism.

Management Commentary as a Valuation Anchor

The management repeatedly emphasises two themes: capital discipline and deployment visibility. The company has stated that vessel acquisitions are pursued only when medium-term employment visibility exists and that return thresholds are evaluated over full operating cycles rather than single-year earnings.

This stance matters for valuation. It reduces the risk of capital being deployed at cycle peaks and supports the case for more stable cash flows over time. At the same time, management has acknowledged the inherently uneven nature of offshore operations, cautioning against interpreting strong quarters as new baselines.

By aligning valuation interpretation with these statements, the analysis avoids assuming growth trajectories that management itself does not endorse.

What the Current Valuation Appears to Discount

Taken together, the valuation metrics imply that the market is pricing in sustained deployment of the existing fleet and a continuation of current margin levels, without assuming a further step-change in returns on capital. There is limited tolerance for execution slippage, extended downtime, or materially higher leverage.

In other words, the valuation reflects progress, but not exuberance.

Risks, Constraints, and What to Watch

Seamec’s business carries risks that are structural rather than incidental. They arise not from competitive aggression or pricing pressure, but from the nature of offshore operations themselves.

The most immediate constraint is utilisation risk. Revenue and margins depend heavily on keeping vessels deployed. Even short periods of idling, whether due to delayed contracts, weather disruptions, or technical issues, can have a disproportionate impact on quarterly performance. While demand for inspection and maintenance work is structurally recurring, its timing is uneven.

A second constraint lies in capital intensity. Vessel acquisitions require large upfront investment, while returns are realised gradually over long operating lives. This creates a lag between capital deployment and earnings visibility. If deployment assumptions prove optimistic, returns on capital can remain subdued for extended periods, even when assets are technically sound.

Execution and reliability also matter more here than in most service businesses. Offshore contracts, particularly with public-sector clients, impose strict availability and safety requirements. Mechanical failures or certification delays can lead not only to revenue loss but also to penalties and reputational impact, which in turn affect future contract awards.

From a financial standpoint, leverage risk must be viewed in context. Debt rises during expansion phases and moderates when cash flows stabilise. While current leverage appears manageable, sustained underutilisation or cost overruns during fleet induction could pressure cash flows and limit balance-sheet flexibility.

Finally, policy and client concentration remain relevant. Offshore activity in India is still heavily influenced by a small number of large operators. Changes in project timelines, procurement processes, or regulatory standards can affect deployment schedules, even when long-term demand remains intact.

These risks do not invalidate the business model, but they explain why returns are cyclical and why valuation multiples tend to remain range-bound over long periods.

Closing Perspective

Seamec is best understood as a specialised offshore operator that has emerged from a difficult cycle with a stronger fleet and a more favourable service mix. The last five years show a clear improvement in operating margins, asset quality, and cash generation, albeit accompanied by the expected volatility of a capital-intensive business.

The company’s progress has been deliberate rather than dramatic. Growth has come through asset renewal and improved deployment rather than aggressive expansion. Management commentary reinforces this posture, emphasising capital discipline and contract visibility over headline growth.

From a valuation standpoint, the market appears to acknowledge this improvement while remaining cautious on durability. Current multiples recognise better operating quality but do not assume a prolonged peak cycle or exceptional returns on capital. This balance reflects the realities of offshore marine services, where long-term value creation depends less on momentum and more on execution across cycles.

In that sense, Seamec today stands as a business in transition, not from weakness to strength overnight, but from fragility to resilience over time. Its future outcomes will be shaped not by how fast it grows, but by how consistently it deploys capital, maintains its fleet, and converts offshore demand into durable cash flows.

Turn research into action, trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.