The packaging industry in India plays a functional rather than discretionary role in the economy. Unlike consumer-facing industries, packaging demand is largely derived from end-use sectors such as FMCG, food and beverages, pharmaceuticals, industrial goods, and infrastructure, making it both structurally relevant and closely tied to broader economic activity.

The packaging industry in India has evolved into one of the largest and fastest-growing sectors within India’s economy. The Indian packaging market was valued at approximately USD 86 billion in 2024 and is projected to reach USD 143 billion by 2029, implying a compound annual growth rate of around 11% over the period. Some industry estimates project even higher expansion driven by retail penetration, e-commerce, and export growth. India has already surpassed Japan to become the third-largest packaging market globally, underscoring the scale and strategic importance of the Indian packaging sector

Understanding the Indian Packaging Industry

The packaging industry in India is not a single unified market but a collection of material-based segments including paper packaging, plastic packaging, glass packaging, metal cans, and specialty films. Think of it this way: glass packaging behaves very differently from flexible plastics, and paperboard follows different cycles compared to polymer films. Each format has its own capital requirements, margins, and cost dynamics. Over the last decade, the sector evolved from a basic commodity business into something more specialized. What drove this? Rising consumption, urbanization, e-commerce growth, and stricter quality standards across end markets.

Demand Drivers – Where the Growth Comes From

| Segment | Nature | Demand Characteristics |

|---|---|---|

| FMCG & Food Packaging | Defensive / Stable | Most stable demand base. Benefits from repeat purchases and shift to branded products and organized retail channels. |

| Pharmaceutical Packaging | Defensive | Driven by safety standards and traceability requirements. High entry barriers create stable competitive dynamics. Tracks pharma industry growth. |

| E-commerce Packaging | Growth-oriented | Requires packaging for transit protection and logistics optimization. Sensitive to fulfillment models and return rates. |

| Industrial Packaging | Cyclical | Serves chemicals, automotive, construction sectors. Volumes fluctuate with industrial activity rather than consumer demand. |

The food industry held nearly 52% share of the plastic India packaging market in FY2023-24, driven by increased demand for processed foods, dairy products, and branded staples.

The Indian pharmaceutical industry accounts for nearly 18% of the plastic packaging market, reflecting India’s positioning as a global pharmaceutical hub and exporter of generic medicines.

India’s e-commerce packaging market is projected to reach USD 4.22 billion by 2026, expanding at a CAGR of 12.48%, as dimensional weight pricing and returns-ready constructions reshape retail packaging formats.

Cost Structure and Profitability

Here's the tricky part – most packaging relies heavily on raw materials like polymers, paper, aluminum, and energy. This makes margins sensitive to input price swings. The key question is: how quickly can you pass through cost changes to customers?

Value-added and specialized packaging generally offers better pricing power than commodity formats. Think pharmaceutical packaging versus basic plastic bags.

Environmental norms are reshaping the industry. Extended producer responsibility, recycled content mandates, and plastic restrictions are changing material choices and capital allocation. While these create compliance costs, they also favor larger players with scale and technology.

Material-wise Industry Structure

The Indian packaging industry is best analysed by separating it into material-based segments, as each category operates under distinct cost structures, regulatory pressures, and demand characteristics.

Paper-based packaging forms a large and growing segment, driven by demand from FMCG, food delivery, e-commerce, and consumer goods. Corrugated boxes, paperboard cartons, and folding cartons benefit from relatively high recyclability and favourable regulatory perception. However, margins in this segment are closely linked to paper and pulp prices, which can be volatile and often influenced by global supply conditions. Pricing power is typically moderate, with pass-through dependent on customer relationships and contract structures. Nearly three-fourths of India’s paper production already comes from recovered paper and recycled fibre, strengthening the sustainability profile of paper packaging formats.

Flexible plastic packaging is one of the most widely used formats due to its lightweight nature, cost efficiency, and versatility. It is extensively used in food, personal care, and pharmaceutical applications. This segment is highly sensitive to polymer prices and, in many cases, aluminium foil costs. While flexible packaging offers scale benefits and high-volume throughput, it also faces elevated regulatory scrutiny due to plastic waste concerns. Compliance requirements and recycled content mandates are therefore increasingly influencing product design and capital expenditure decisions. The packaging industry is increasingly transitioning toward mono-material structures, such as 100% recyclable rPET and PE-only flexible packs, to enhance recyclability and meet regulatory mandates. The April 2025 deadline mandating 30% post-consumer recycled content in rigid plastics is forcing producers to redesign packs and secure food-grade recycled PET supply chains.

Rigid plastic packaging caters to applications where durability, shape retention, and protection are critical, such as food containers, paints, lubricants, and household products. This segment tends to offer better customisation and customer stickiness compared to flexible packaging, particularly when packaging is closely integrated with the customer’s product design. However, raw material sensitivity remains high, and regulatory exposure to plastic usage norms continues to shape long-term strategy.

Glass packaging occupies a distinct position in the industry. It is primarily used in alcoholic beverages, food, and select pharmaceutical applications. Glass benefits from high recyclability and strong consumer perception, but it is energy-intensive and sensitive to fuel and power costs. Demand in this segment is relatively stable and often linked to beverage consumption patterns rather than broader consumer cycles. Capital intensity and operating leverage are higher compared to most plastic-based formats. Circular models, including returnable glass bottles and refill systems, are gaining traction as sustainability expectations tighten.

Specialty and high-performance films represent a more niche but value-added segment. These products are designed for specific applications requiring strength, clarity, durability, or functional coatings, often serving industrial, automotive, or infrastructure-linked end uses. While volumes are lower, margins tend to be more stable due to higher entry barriers, technical know-how, and lower substitutability.

Read A Year of Execution and Strategic Transformation at Laurus Labs Ltd for a sharp breakdown of growth, margins, and capital allocation in action.

Cost Structure and Pricing Dynamics

Cost structures in the packaging industry are dominated by raw materials and energy, making profitability highly sensitive to input price movements. Across most packaging formats, raw materials account for a substantial share of operating costs, while labour and overheads play a comparatively smaller role. As a result, margin behaviour is shaped less by volume growth and more by the ability to manage cost pass-through.

Polymer-based packaging segments, including flexible and rigid plastics, are directly exposed to fluctuations in crude-linked inputs such as polyethylene, polypropylene, and PET. Price volatility in these materials can be sharp and sudden, particularly during periods of global supply disruption or changes in energy prices. While many packaging companies operate with pass-through mechanisms, the timing of price revisions often lags input cost movements, leading to temporary margin compression or expansion depending on the direction of price changes.

Paper-based packaging faces a different cost dynamic. Input costs are influenced by paper and pulp prices, which are affected by global demand, recycling rates, and capacity utilisation across domestic and international markets. Unlike polymers, paper prices tend to move in cycles that can persist for longer periods. Pass-through in this segment is typically moderate, with pricing power influenced by customer concentration, contract tenures, and the degree of value addition in the packaging format.

Glass packaging is particularly sensitive to energy costs, as furnaces operate continuously and consume significant amounts of fuel and power. Changes in fuel prices therefore have a direct and immediate impact on [operating margins](https://www.tradejini.com/finance-kickstarter/operating-profit-margin). While glass manufacturers can pass on cost increases over time, the capital-intensive nature of operations and limited flexibility in production schedules can amplify operating leverage during periods of cost volatility.

Pricing power across the packaging industry varies by segment and customer profile. Commodity packaging formats with multiple suppliers tend to exhibit lower pricing power, especially when customers have the ability to switch vendors easily. In contrast, application-specific packaging, customised designs, and long-standing supply relationships improve pass-through capability and reduce margin volatility.

Customer mix also plays a role in determining pricing dynamics. Large FMCG and pharmaceutical customers often negotiate long-term contracts with defined pass-through clauses, which provide volume visibility but can limit short-term pricing flexibility. Smaller or specialised customers may allow greater pricing discretion, but volumes tend to be less predictable.

Overall, the packaging industry does not offer uniform margin stability. Periods of raw material inflation or deflation can distort reported profitability, making short-term margin movements an unreliable indicator of structural improvement. A more accurate assessment requires examining pass-through mechanisms, customer concentration, and the balance between commodity and value-added packaging within a company’s portfolio.

Regulation, Sustainability, and Compliance

Regulation and sustainability considerations are increasingly shaping the trajectory of the Indian packaging industry. Environmental concerns, waste management challenges, and regulatory intervention have moved packaging from being a purely operational input to a material area of policy focus. As a result, compliance requirements are now influencing material selection, product design, and long-term capital allocation across the sector.

Sustainability has become a measurable operational requirement due to stricter enforcement of Extended Producer Responsibility and bans on select single-use plastics. Government measures to curb plastic use and promote eco-friendly materials are accelerating structural change across the packaging industry.

Plastic packaging has been most directly affected by regulatory action. Extended Producer Responsibility obligations, restrictions on certain single-use plastic items, and mandates around recycled content have increased compliance costs and operational complexity for manufacturers. Companies are required not only to meet production standards but also to track, collect, and ensure responsible end-of-life treatment of packaging materials. This has shifted part of the regulatory burden upstream to packaging producers, particularly those operating in polymer-intensive segments.

Paper and paperboard packaging benefit from relatively favourable regulatory perception due to higher recyclability and established recovery systems. However, this does not insulate the segment entirely from scrutiny. Sustainability expectations around sourcing, forest management, and energy usage are becoming more prominent, especially for companies supplying large FMCG and export-oriented customers with environmental disclosure requirements.

Glass packaging occupies a different regulatory position. High recyclability and reuse rates support its acceptance from a sustainability standpoint, particularly in beverages. At the same time, the energy-intensive nature of glass manufacturing brings increased attention to emissions, fuel usage, and efficiency improvements. Compliance in this segment therefore centres more on energy optimisation and emissions management than on waste reduction.

Regulation is also influencing product innovation. Lightweighting, material substitution, increased use of recycled inputs, and redesign of packaging formats are becoming central to compliance strategies. While these initiatives often involve upfront investment, they can also create competitive advantages for players with scale, technical capability, and integrated operations.

From an industry structure perspective, regulatory complexity tends to favour organised players over smaller, unorganised manufacturers. Compliance costs, reporting requirements, and certification standards raise entry barriers and accelerate consolidation within certain packaging segments. Over time, this can lead to improved pricing discipline and greater share for compliant players, even as overall cost structures rise. The government has launched initiatives to promote sustainable practices and circularity in packaging solutions, reinforcing compliance requirements across domestic and international players.

Industry Structure and Competitive Landscape

Unlike sectors where scale alone determines competitiveness, packaging companies differentiate themselves through material expertise, customer relationships, cost pass-through capability, and compliance readiness.

The table below positions the key companies covered in this report based on their core packaging segment, material exposure, regulatory sensitivity, and business model, rather than size or valuation. This framework is more relevant for understanding how each company is likely to respond to changes in raw material prices, regulation, and end-use demand.

| Company | OPM | Primary Packaging Segment | Key Materials / Technology | End-Use Exposure | Pricing Power | Raw Material Sensitivity | Sustainability / Regulatory Exposure | Business Nature |

|---|---|---|---|---|---|---|---|---|

| AGI Greenpac | 23% | Glass packaging | Glass containers | Alcoholic beverages, food |

Medium | Medium (energy, soda ash) |

Medium | Integrated manufacturer |

| EPL Ltd | 20% | Flexible packaging (laminates) | Laminates, plastic tubes |

FMCG, personal care, pharma |

Medium | High (polymers, foil) |

High | Global converter |

| Jindal Poly Films | 4–8% | Packaging films | BOPET, BOPP, CPP films |

FMCG, labels, industrial |

Medium | High (polymers) | Medium–High | Integrated films manufacturer |

| Mold-Tek Packaging | 19% | Rigid plastic packaging | IML molded plastics | FMCG, food, paints, pharma |

Medium | High (polymers) | High | Pure-play rigid packaging |

| TCPL Packaging | 16% | Paperboard & flexible | Paperboard, laminates |

FMCG, food, liquor, pharma |

Medium | Medium | High | Diversified packaging |

| Garware Hi-Tech Films | 19% | Specialty films | High-performance BOPET | Automotive, industrial |

High | Medium | Medium | Value-added specialty player |

| Time Technoplast | 15% | Industrial & rigid packaging | Polymer drums, composites |

Chemicals, LPG, infrastructure |

Medium | Medium | Medium–High | Diversified industrial packaging |

The Indian packaging market remains highly fragmented, with over 22,000 units operating across formats. Approximately 85% of these are small and medium enterprises. However, ongoing consolidation is gradually shifting market share toward organised players, particularly in high-margin pharma and food packaging niches.

Read India’s Fertilizer Industry – Market Trends and Future Prospects for a clear view on demand drivers, policy impact, and long-term growth dynamics.

Structural Shifts and Emerging Trends

The Indian packaging industry is undergoing gradual structural change. One of the most visible shifts is the growing emphasis on sustainability-led packaging solutions. Regulatory requirements around waste management and extended producer responsibility, combined with customer pressure from large FMCG and pharmaceutical companies, are accelerating the move toward recyclable, lightweight, and lower-impact packaging formats. This has increased demand for paperboard-based solutions, recyclable mono-material plastics, and higher recycled content across packaging types. While these changes raise compliance and redesign costs in the short term, they also favour organised players with scale, technology, and established customer relationships.

Premiumisation is another important trend shaping the industry. Packaging is increasingly expected to perform functions beyond protection and transport, including shelf differentiation, convenience, traceability, and brand reinforcement. This is particularly evident in food, beverages, personal care, and pharmaceuticals, where packaging design and functionality influence consumer perception and regulatory compliance. As a result, value-added and application-specific packaging is gaining share relative to commoditised formats, improving pricing power and customer stickiness for specialised players.

Technology adoption is playing a growing role in operational efficiency and product innovation. Automation, in-mould labelling, advanced printing techniques, and material science innovations are improving consistency, reducing waste, and enabling more complex packaging designs.

Supply chain resilience has also emerged as a strategic focus. Volatility in raw material availability and prices has encouraged companies to diversify sourcing, invest in backward integration where feasible, and redesign packaging to reduce material usage. Lightweighting and downgauging initiatives are not only sustainability-driven but also cost-driven, helping mitigate exposure to raw material inflation.

Technological innovation is rapidly reshaping the Indian packaging industry. Smart packaging technologies including QR codes, NFC tags, RFID tracking, and augmented reality interfaces are being deployed to improve traceability and enhance consumer engagement. Advanced analytics and AI integration are being adopted for predictive maintenance, quality optimisation, and waste reduction, improving operational efficiency across large packaging suppliers. Digital watermarks and smart sorting technologies are being introduced to enhance material recovery facilities and circular recycling models.

Taken together, these structural shifts suggest that future growth in the packaging industry will be driven less by headline volume expansion and more by changes in mix, functionality, and compliance readiness. Companies that adapt to these trends are likely to see relatively more stable margins and stronger customer retention, even as overall industry growth remains closely linked to end-use demand conditions.

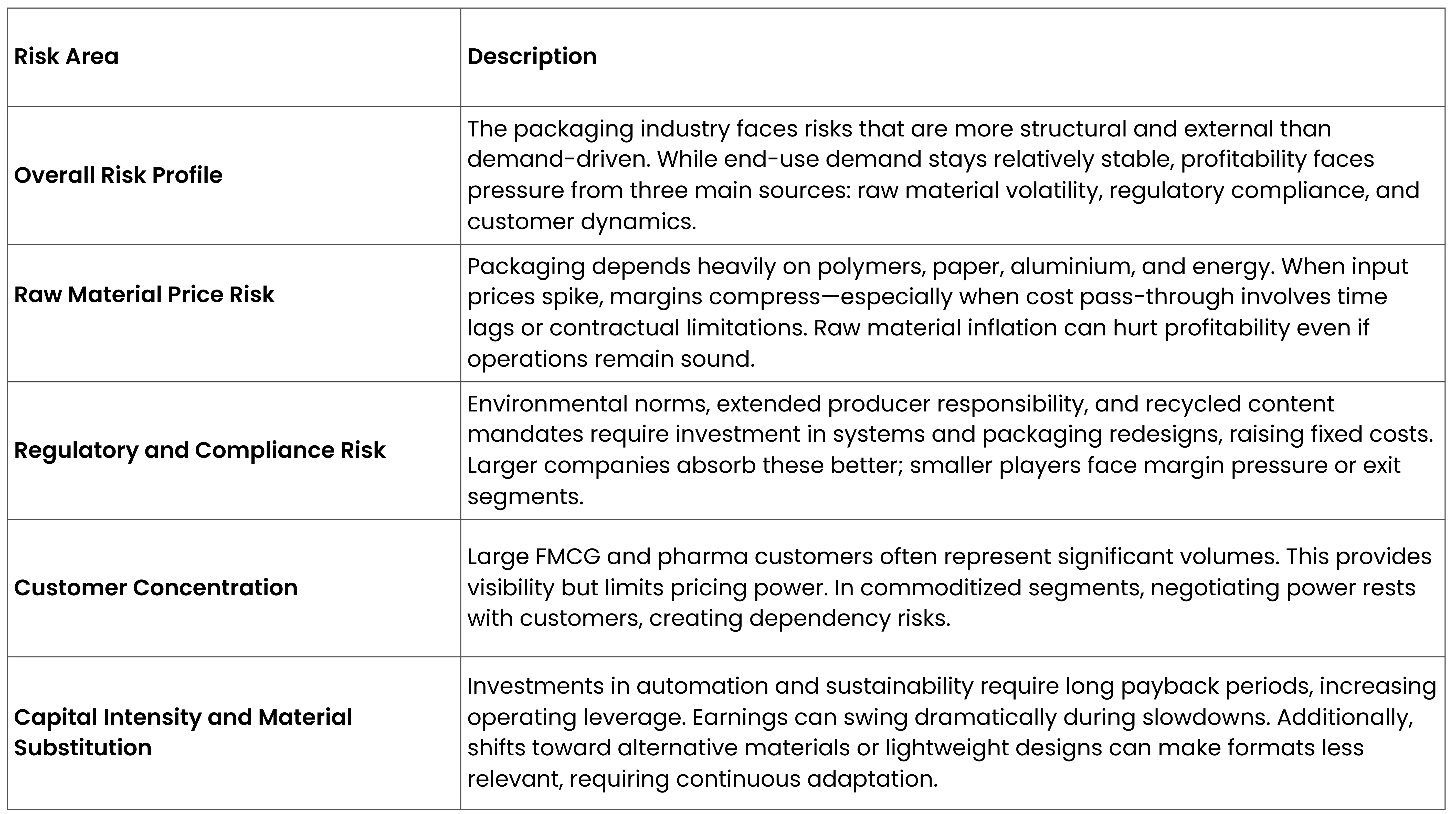

Risks and Challenges – Packaging Industry

Long-Term Outlook and How Investors Should Read the Sector

The long-term outlook for the Indian packaging industry is shaped by steady end-use demand rather than episodic growth spurts. Packaging will remain an essential input across consumption, healthcare, logistics, and industrial activity, ensuring structural relevance even as growth rates vary by segment.

Future growth is unlikely to be uniform across packaging formats. Expansion will be driven more by shifts in material mix, application specificity, and compliance readiness than by pure volume growth. Paperboard, specialty films, and value-added plastic packaging are positioned to gain share as sustainability norms tighten and customers demand higher functionality. In contrast, commoditised formats with limited differentiation are likely to face persistent margin pressure, especially during periods of raw material volatility.

Cost dynamics will remain a defining feature of the sector. Input prices for polymers, paper, glass, and energy are expected to remain cyclical, making pricing discipline and pass-through mechanisms critical determinants of profitability. Companies with diversified material exposure, strong customer relationships, and application-specific offerings are better placed to manage these cycles than single-format, commodity-focused players.

Regulation and sustainability will increasingly influence competitive positioning rather than simply adding compliance costs. Environmental norms, extended producer responsibility requirements, and recycled content mandates are likely to accelerate consolidation and favour organised manufacturers with scale, technology, and balance sheet strength. Over time, this could improve industry discipline, even as capital intensity rises.

There is a growing export market for Indian packaging materials, particularly plastic films, laminates, paperboard cartons, and specialty packaging solutions. India’s cost competitiveness allows manufacturers to achieve up to 40% cost savings compared to European counterparts, making the country an increasingly preferred hub for global sourcing.

For investors analysing the packaging sector, traditional growth metrics such as revenue expansion or capacity additions offer limited insight in isolation. A more effective framework is to focus on material exposure, pricing power, regulatory readiness, customer concentration, and capital allocation discipline. Short-term margin movements often reflect raw material cycles rather than structural change and should be interpreted accordingly.

In essence, the Indian packaging industry is best viewed as a structurally necessary, end-use–linked sector with uneven profitability across formats. It offers demand continuity but requires careful differentiation between business models to assess resilience and long-term value creation.

Turn research into action — trade smarter on CubePlus.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.