TVS Supply Chain Solutions helps businesses move, store, and deliver products across four continents. The company generated revenue of ₹11,003 crore in FY26, but profitability has remained a challenge, with profits reported in only two of the last eight years. FY26 was the stronger of those two years. This article examines whether the recent improvement is sustainable and what the business could be worth.

What the company does

The company is an asset-light, technology-led logistics provider. Asset-light means it owns very little of the infrastructure it runs, operating leased warehouses and outsourced transport rather than tying up capital in buildings and trucks. Its work splits into two segments that behave very differently.

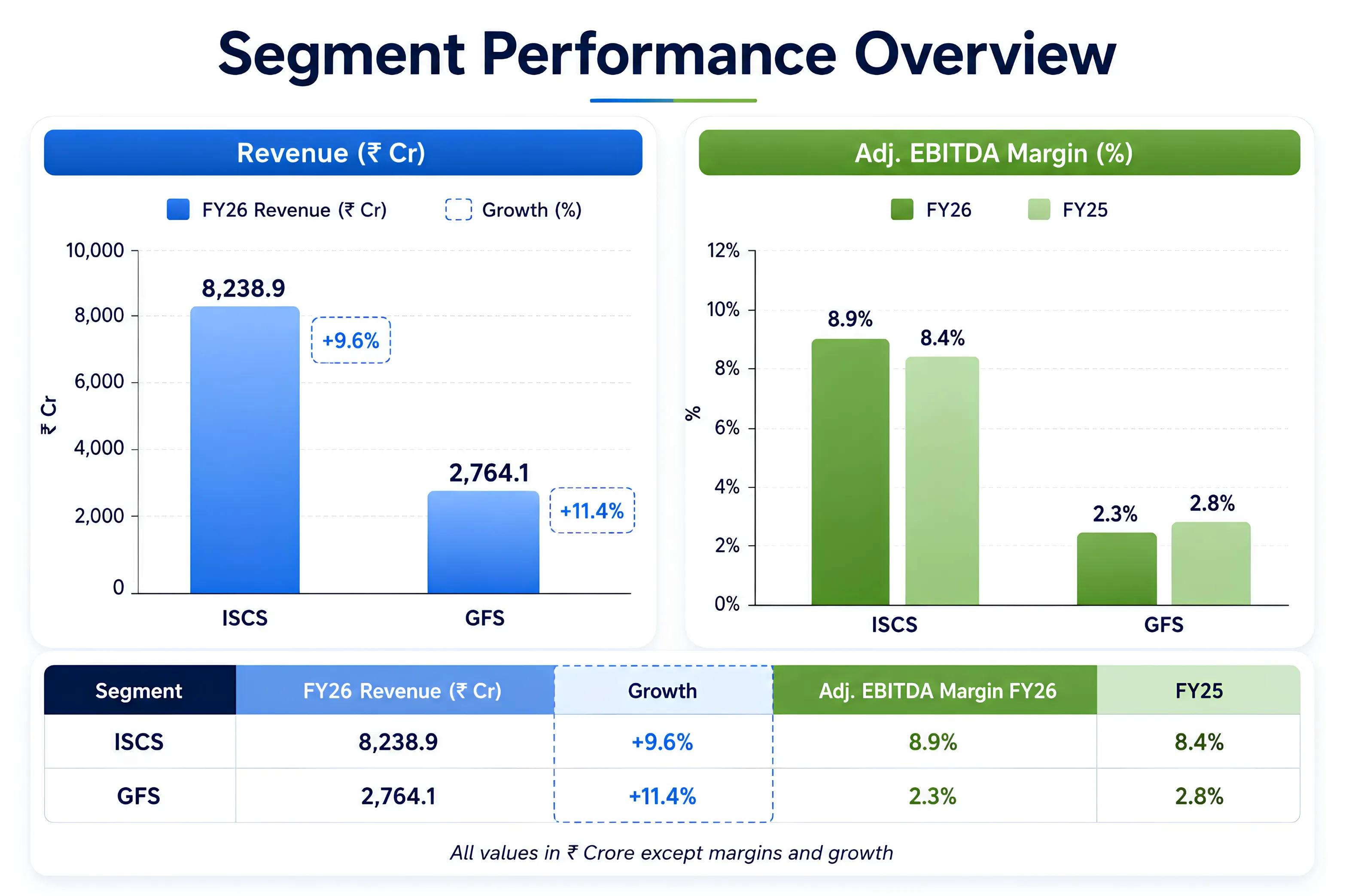

ISCS, or Integrated Supply Chain Solutions, is about three-quarters of revenue. This is the embedded, long-term work: managing a customer's sourcing, running logistics inside its factories, storing and moving goods, and handling spare parts after the sale. The contracts run for years, so the income is steady and the margins are the higher of the two.

GFS, or Global Forwarding Solutions, is the remaining quarter. Forwarding is the business of booking cargo space on ships and aircraft and handling the customs and paperwork. The forwarder does not own the vessels. It arranges the journey. Its revenue and margins move with global freight rates, which makes it far more volatile than ISCS.

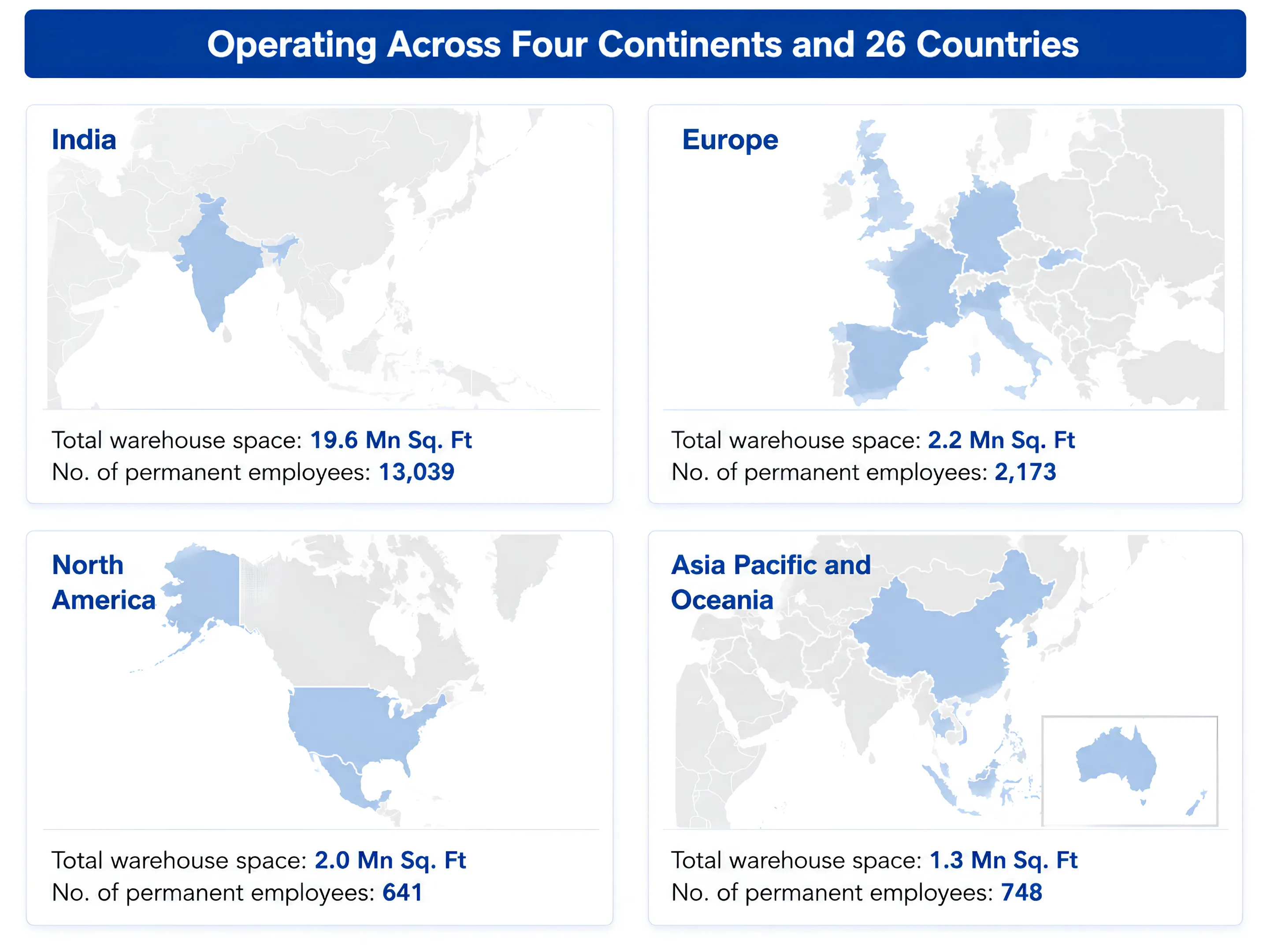

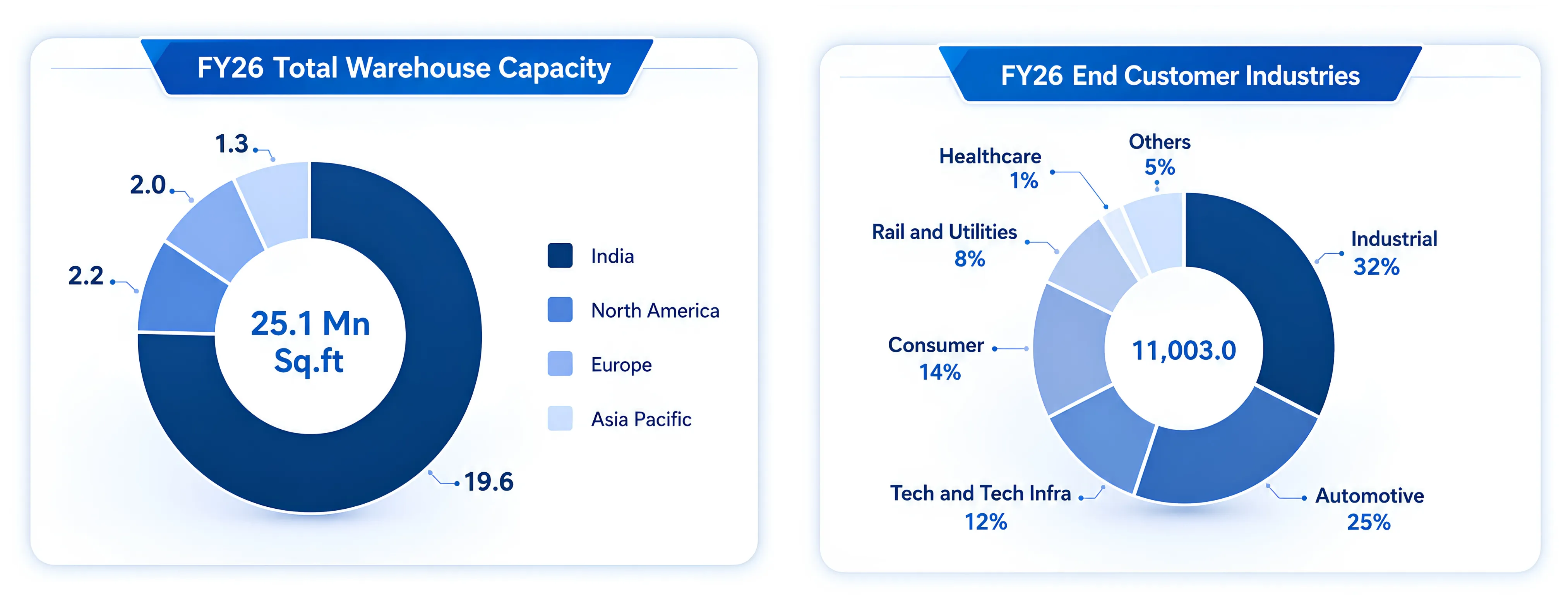

Across the two, the company manages 25.1 million square feet of warehouse space, employs over 16,500 people, and counts 100 of the Fortune Global 500 among its customers, spread across industrial, automotive, consumer, and technology sectors.

The turnaround in the numbers

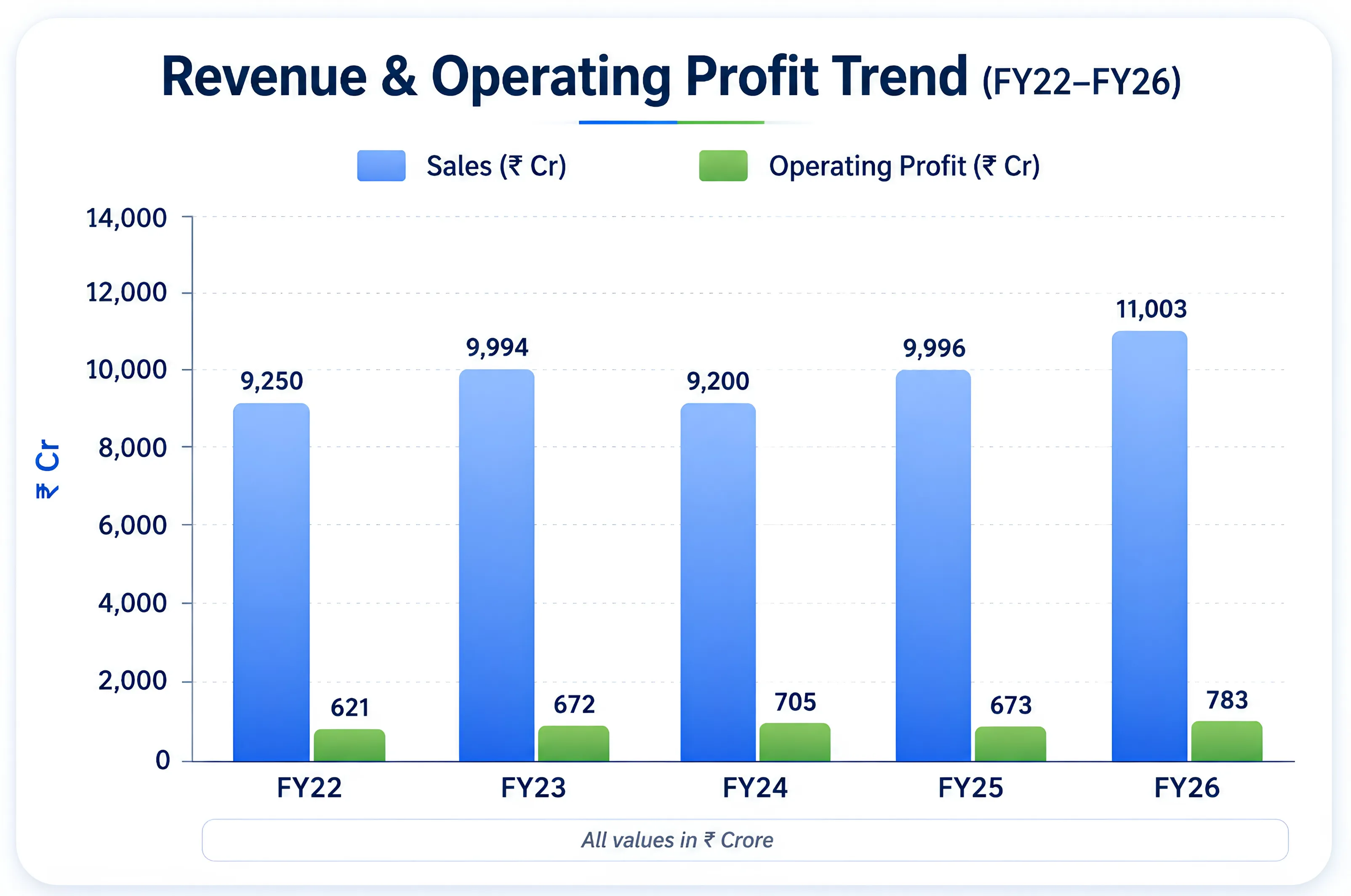

Set against its own history, FY26 stands out. The company has run a large operation at a thin margin for years and has rarely turned that into a profit.

| Year | Sales (₹ Cr) | Operating profit (₹ Cr) | OPM | Net profit / (loss) (₹ Cr) |

|---|---|---|---|---|

| FY22 | 9,250 | 621 | 7% | (46) |

| FY23 | 9,994 | 672 | 7% | 42 |

| FY24 | 9,200 | 705 | 8% | (90) |

| FY25 | 9,996 | 673 | 7% | (10) |

| FY26 | 11,003 | 783 | 7% | 117 |

FY26 net profit includes a one-time gain, discussed below.

Two things stand out. The operating margin (OPM), the operating profit as a share of sales, has sat at 7 to 8 percent throughout, so the core operation has neither weakened nor sharply improved. And the bottom line has swung around zero, dipping into a loss in FY24 when global freight rates collapsed and pulled the forwarding business down, before turning to a ₹117 crore profit in FY26. Revenue crossed ₹11,000 crore for the first time, and the fourth quarter alone crossed ₹3,000 crore, also a first.

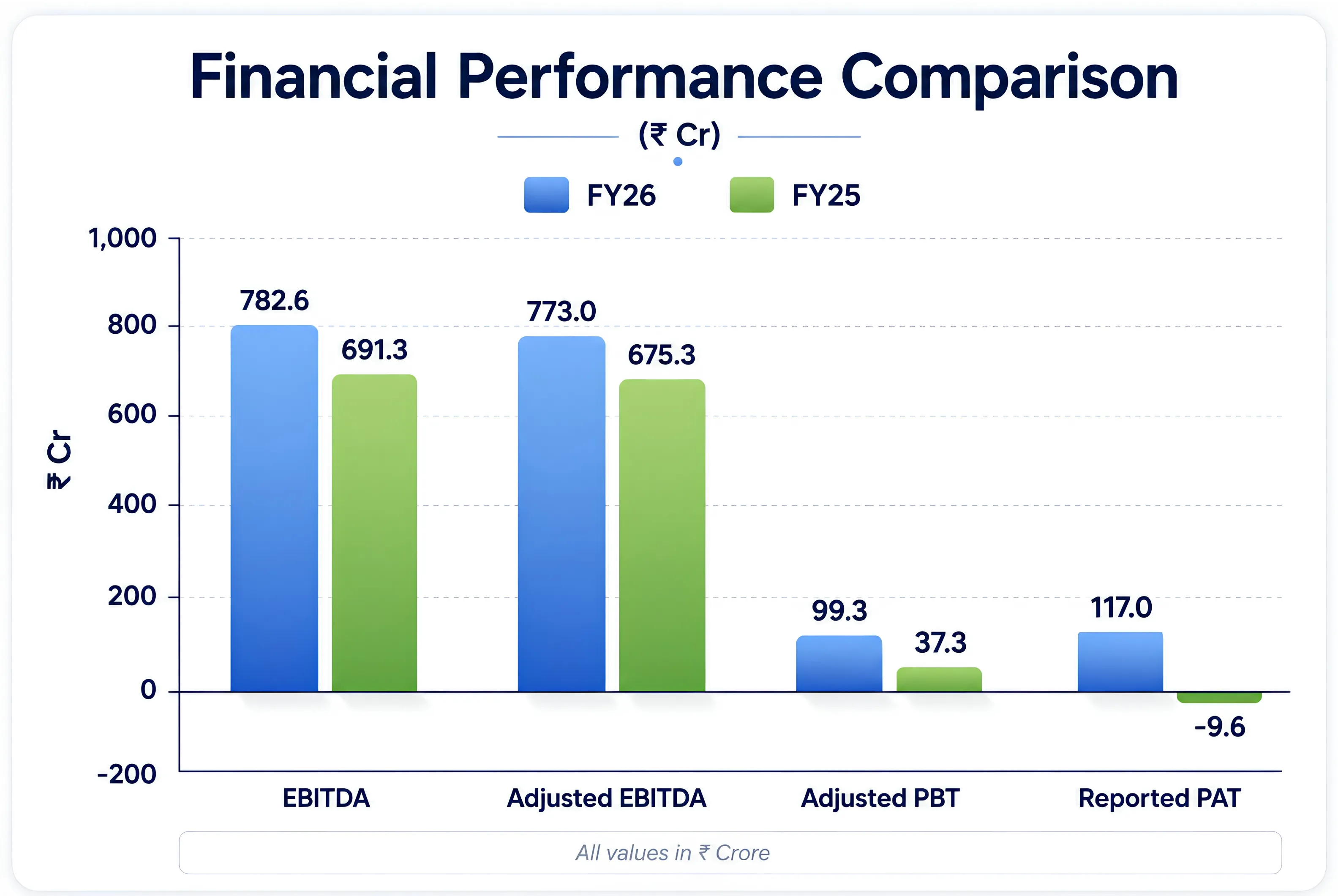

But the headline profit of ₹117 crore needs reading with care.

| Measure (₹ Cr) | FY26 | FY25 |

|---|---|---|

| EBITDA | 782.6 | 691.3 |

| Adjusted EBITDA | 773.0 | 675.3 |

| Adjusted PBT | 99.3 | 37.3 |

| Reported PAT | 117.0 | (9.6) |

EBITDA is the profit from operations before interest, tax, and accounting deductions. The reported profit of ₹117 crore includes a one-time gain of ₹177 crore booked in the first quarter, from transferring assets to an investment trust, and it absorbs ₹106 crore of one-time costs, mostly to restructure the European business. The two roughly cancel. Strip both out, and the clean measure of what the operations earned is the adjusted profit before tax of ₹99.3 crore, up from ₹37.3 crore. That near tripling, not the headline PAT, is the real signal that the business turned. After tax it is roughly ₹70 crore of underlying profit, which tells you the company is only just profitable on an operating basis.

Also Read: A Comprehensive Analysis of India's Logistics and Supply Chain Sector Part ½

What is driving it

The recovery was led by the steadier segment and by India.

ISCS did the more valuable thing: it grew while becoming more profitable, its margin widening as the European operation, long the weak spot, was made leaner through a cost programme the company calls Project One. GFS grew revenue on higher ocean freight volumes out of India, though its margin slipped as freight rates stayed weak. The volumes are strong; the pricing is not in the company's hands.

By geography, India now contributes 28 percent of revenue and grew 31 percent in the fourth quarter, the clear engine of the year. The rest comes from Europe, North America, and Asia Pacific. The company won new business worth ₹1,207 crore during the year, equal to about 12 percent of the prior year's revenue, and its Fortune 500 customer count rose from 91 to 100. The contracts are sticky, with the average customer relationship running about 4 years in India, 5 in North America, and over 7 in Europe.

The balance sheet and cash

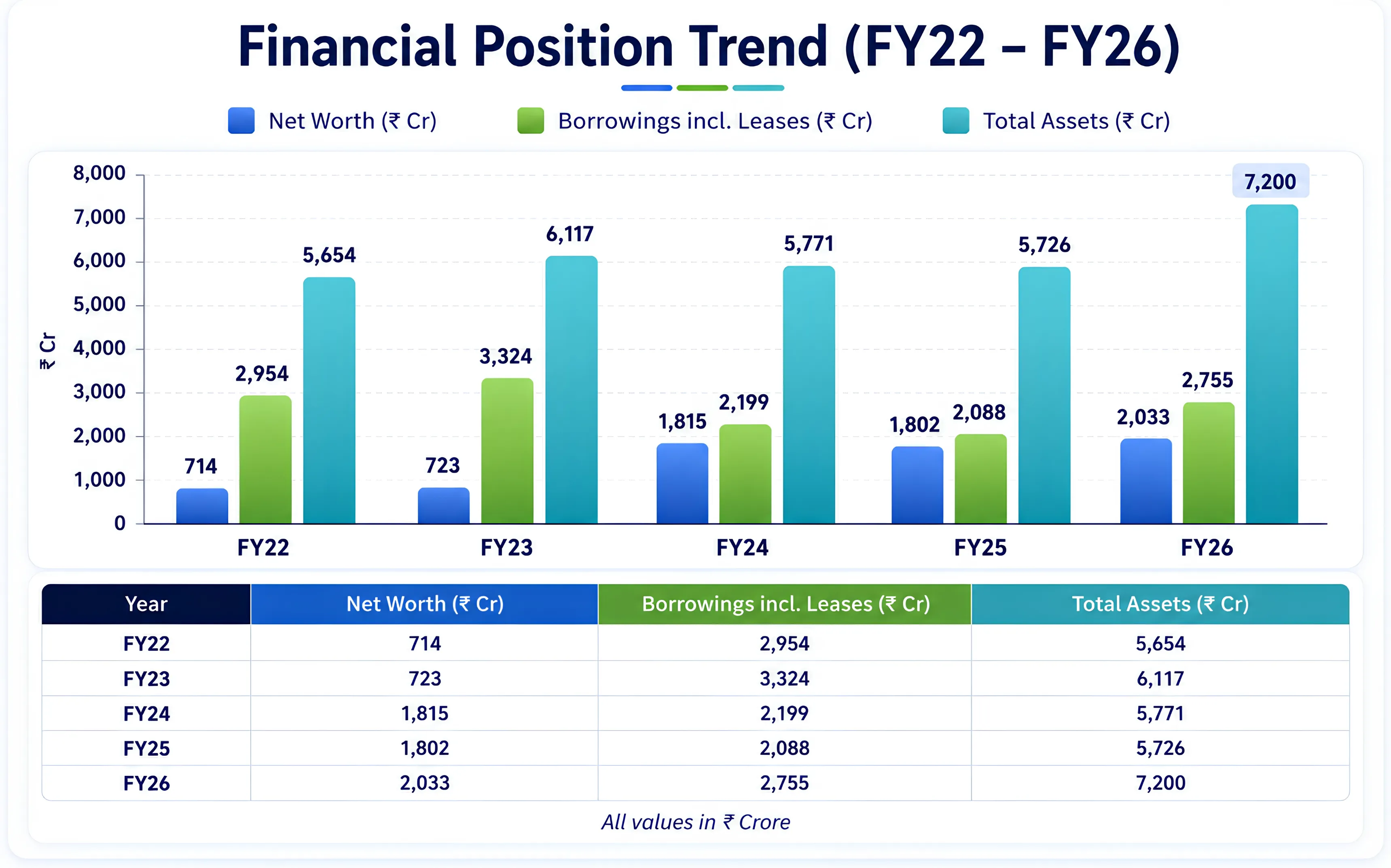

For a logistics company the balance sheet matters as much as the profit line, and here it is healthier than the gross figures suggest.

The 2023 listing recapitalised the company, roughly doubling its net worth and letting it cut bank debt the following year. The borrowings line looks large and rose again in FY26, but most of that figure is the accounting value of warehouse leases rather than money owed to banks, and the rise reflects new warehouse capacity taken on for new projects. Net of cash, the actual bank debt is only about ₹370 crore, of which just ₹120 crore is long-term and the rest short-term working capital. The company is rated India AA.

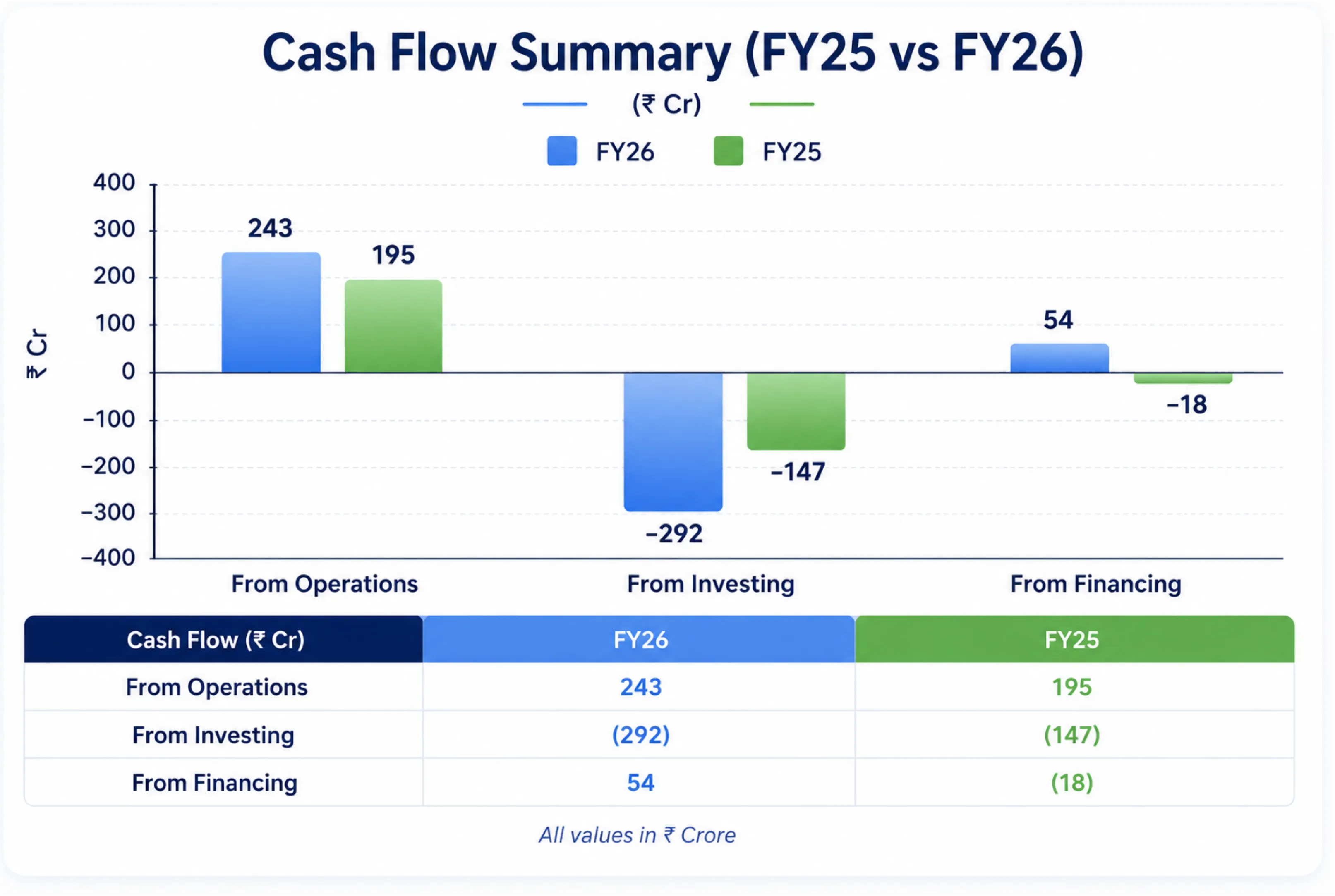

The business generated ₹243 crore of operating cash, up from ₹195 crore. Operating cash has been healthy in most years, the clear exception being FY24, when it fell sharply before recovering. This matters because cash, not reported profit, is what pays down debt over time.

What management expects next

Management frames FY26 as the foundation year. For FY27 it guides to double-digit revenue growth, possibly into the early teens, with ISCS as the main contributor. It expects ISCS margins to move from 9.3 percent toward a 9.5 to 10 percent band, and the overall operating margin to begin around 7.3 to 7.5 percent, with the final figure depending on the forwarding business, where it stays bullish on volumes but guarded on freight pricing.

Two moves support the outlook. The acquisition of Swamy and Sons 3PL, completed in May 2026, takes the company deeper into fast-moving consumer goods and is expected to lift India margins in FY27. An early-stage partnership aimed at defence and aerospace logistics, a field with high certification barriers, could open a new vertical over time. The company also continues to lean on technology, with AI and robotics in its operations and an accepted patent for a unified logistics platform. Its order pipeline stands at ₹6,100 crore, of which it historically converts about a fifth, a rate it wants to push higher.

The year also marks a leadership change, with the managing director who led the recovery handing over to the global chief executive. Management signalled continuity rather than a change of course.

What it is worth

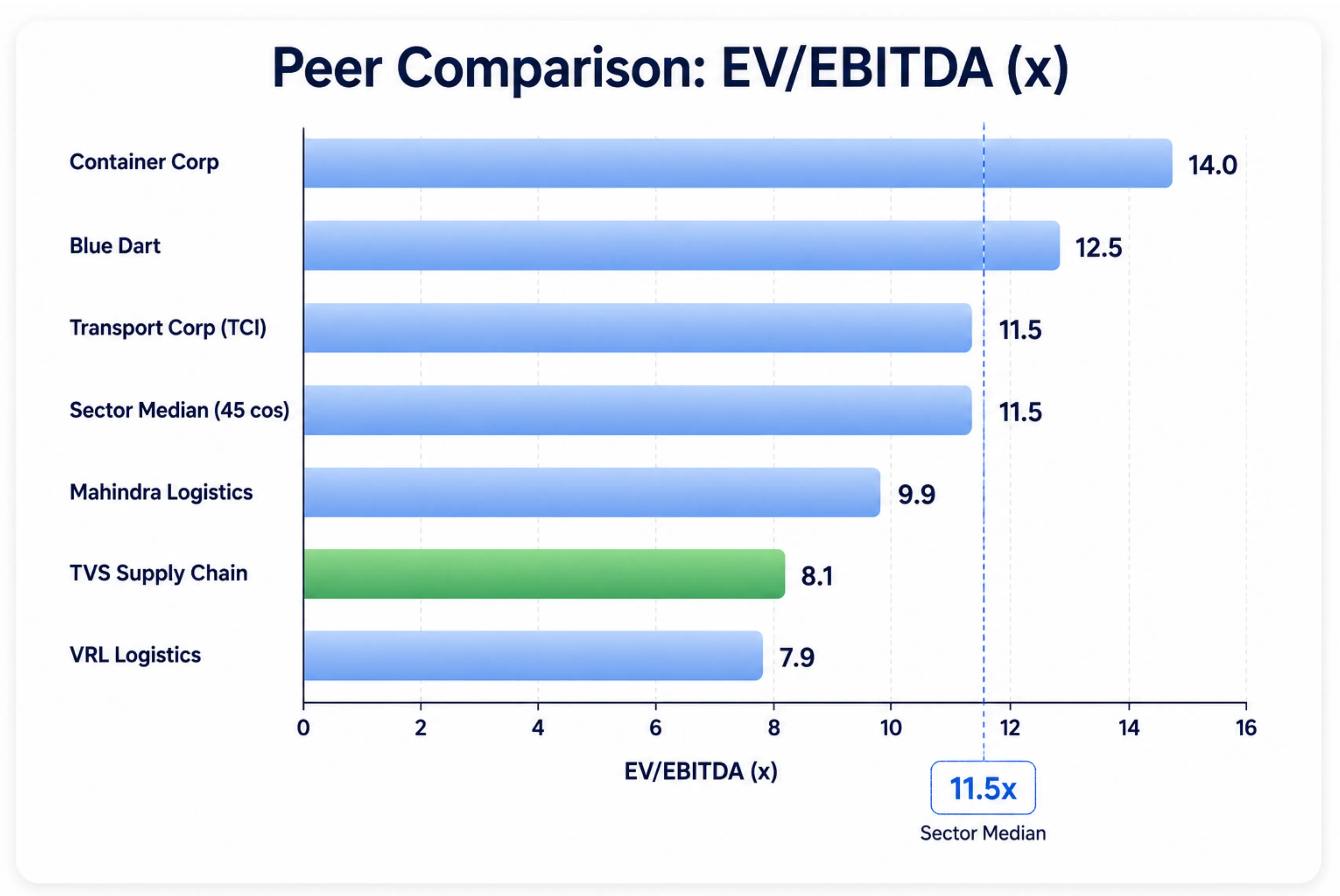

A logistics business like this is valued on EV/EBITDA. Enterprise value, or EV, is the company's market value plus its debt, which makes the measure neutral to how a business is financed, and EBITDA is a steadier base than a profit line that has only just turned positive. On this measure TVS Supply Chain trades at about 8 times EBITDA.

A multiple says nothing on its own, so it has to be placed against comparable listed logistics companies, all measured the same way.

| Company | EV/EBITDA | ROCE % | OPM % |

|---|---|---|---|

| Container Corp | 14.0 | 12.4 | 21.5 |

| Blue Dart | 12.5 | 16.6 | 15.5 |

| Transport Corp (TCI) | 11.5 | 19.5 | 10.5 |

| Mahindra Logistics | 9.9 | 7.3 | 5.4 |

| TVS Supply Chain | 8.1 | 9.9 | 7.1 |

| VRL Logistics | 7.9 | 17.9 | 20.2 |

| Sector median (45 cos) | 11.5 | 12.4 | 10.5 |

TVS sits at the low end of the group, below the sector median near 11 times. The asset-owning, higher-return names trade richer, and consistently so: Transport Corporation of India, Blue Dart, and Container Corp all earn returns on capital well above TVS's and carry multiples of 11 to 14 times. The most directly comparable name is Mahindra Logistics, the other listed Indian third-party logistics company on the same model. It trades close to 10 times despite returns and margins lower than TVS's, which makes TVS the cheaper of the two nearest peers. VRL Logistics is cheaper still, an outlier that pairs strong returns with stalled growth.

Read together, TVS is priced at the bottom of the logistics pack. Against the high-return names, that gap is consistent with its lower returns. Against its closest peer, it is the cheaper of the two despite better current numbers. The multiple moves up only if its margins and returns climb toward the better operators, which is the same improvement management has guided to and what the coming years will test. You are paying about 8 times today's operating earnings for a business whose case rests on those earnings rising.

The risks

The turnaround is real, but the room for error is small.

The forwarding business is the first risk. Its revenue and margins track global freight rates, shaped by fuel costs and conflict on trade routes, which the company cannot control. The second is the thinness of profit. A business turning over ₹11,000 crore that nets a little over 1 percent operates on a margin where a small move in cost or pricing swings the bottom line sharply. The third is the gap between the headline and the underlying, since the reported profit leans on a one-time gain and the operating profit beneath it is far smaller. The fourth is conversion, because the pipeline is a list of possibilities, not booked revenue.

The verdict

On the numbers, FY26 is a turnaround, but an early one. The operating evidence is clear. Revenue is growing, the larger ISCS business is widening its margins, the European operation has been fixed, and the company is generating real cash.

What keeps it early is that the operating margin has not yet structurally moved, the profit beneath the one-off is still slim, and the freight-rate pressure on forwarding has not gone away. The business is priced at about 8 times its operating earnings while those earnings work up from a low base. The direction is set. Whether the margins reach where management is guiding is the question the next few years will answer.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.