Mutual funds have emerged as one of the most preferred investment choices in India, with Systematic Investment Plans (SIPs) consistently touching new record inflows month after month. The industry’s growth reflects this trend clearly. In 2015, India’s mutual fund industry managed assets worth ₹12,55,000 crore, and as of August 31, 2025, the total AUM has surged to ₹75,18,702 crore. While this rise indicates growing trust and improving financial awareness, investor behaviour still shows patterns driven more by emotions and market noise than by research or data. This is where behavioral finance becomes relevant. It helps decode how biases and psychological triggers influence decision-making. For mutual fund investors, understanding these behavioral traps is crucial to avoid costly mistakes and stay focused on long-term financial goals.

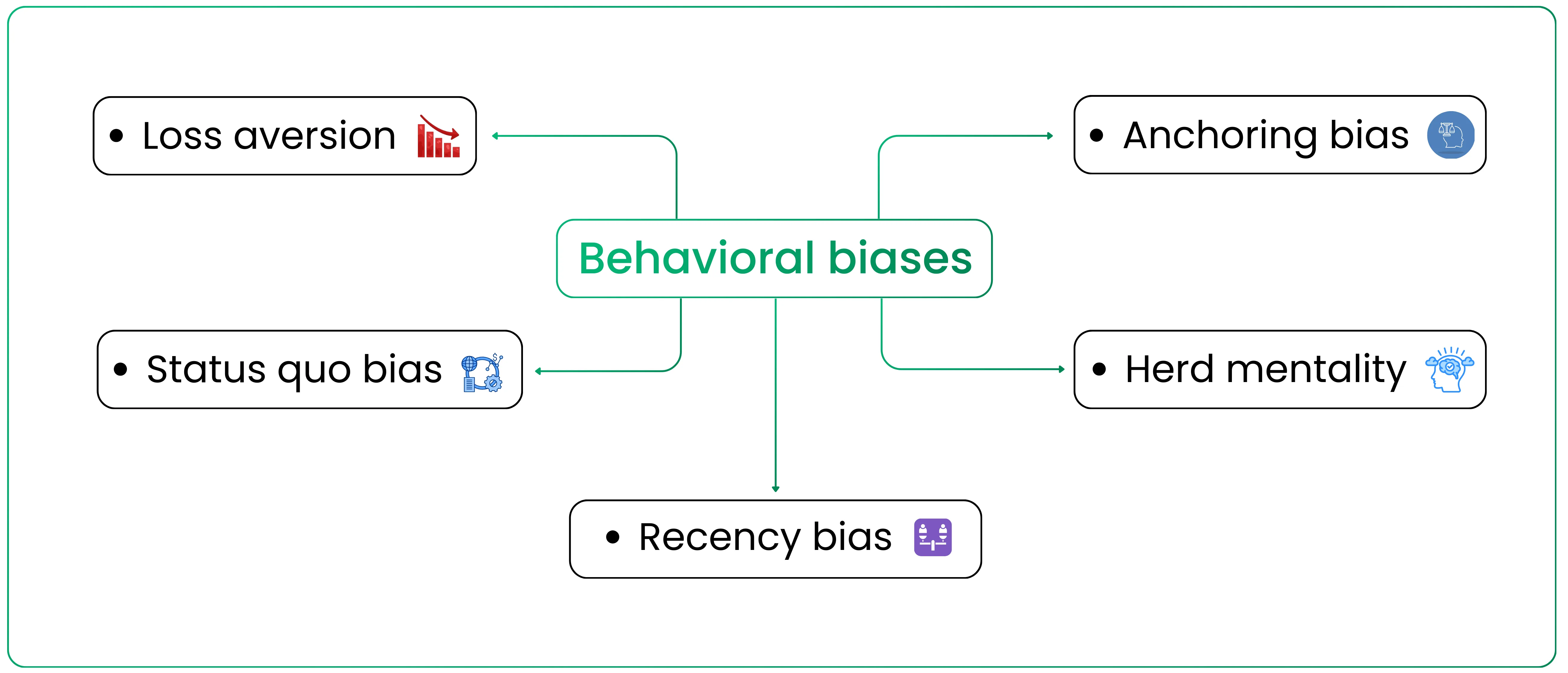

Loss aversion

Investors dislike losses more than they like equivalent gains. A 10% fall in mutual fund portfolio value creates far more anxiety than the satisfaction of a 10% rise. This results in hesitation to invest during corrections, even though historical data shows that investing at lower market levels improves long-term returns. The fear of losing prevents rational buying when valuations are more attractive. It is natural to feel anxious when the portfolio shows a decline or notional loss. Very few investors are able to look beyond this fear and confidently invest more during market dips or even continue their SIPs without interruption in a downtrend. However, this discipline is essential for building long-term wealth.

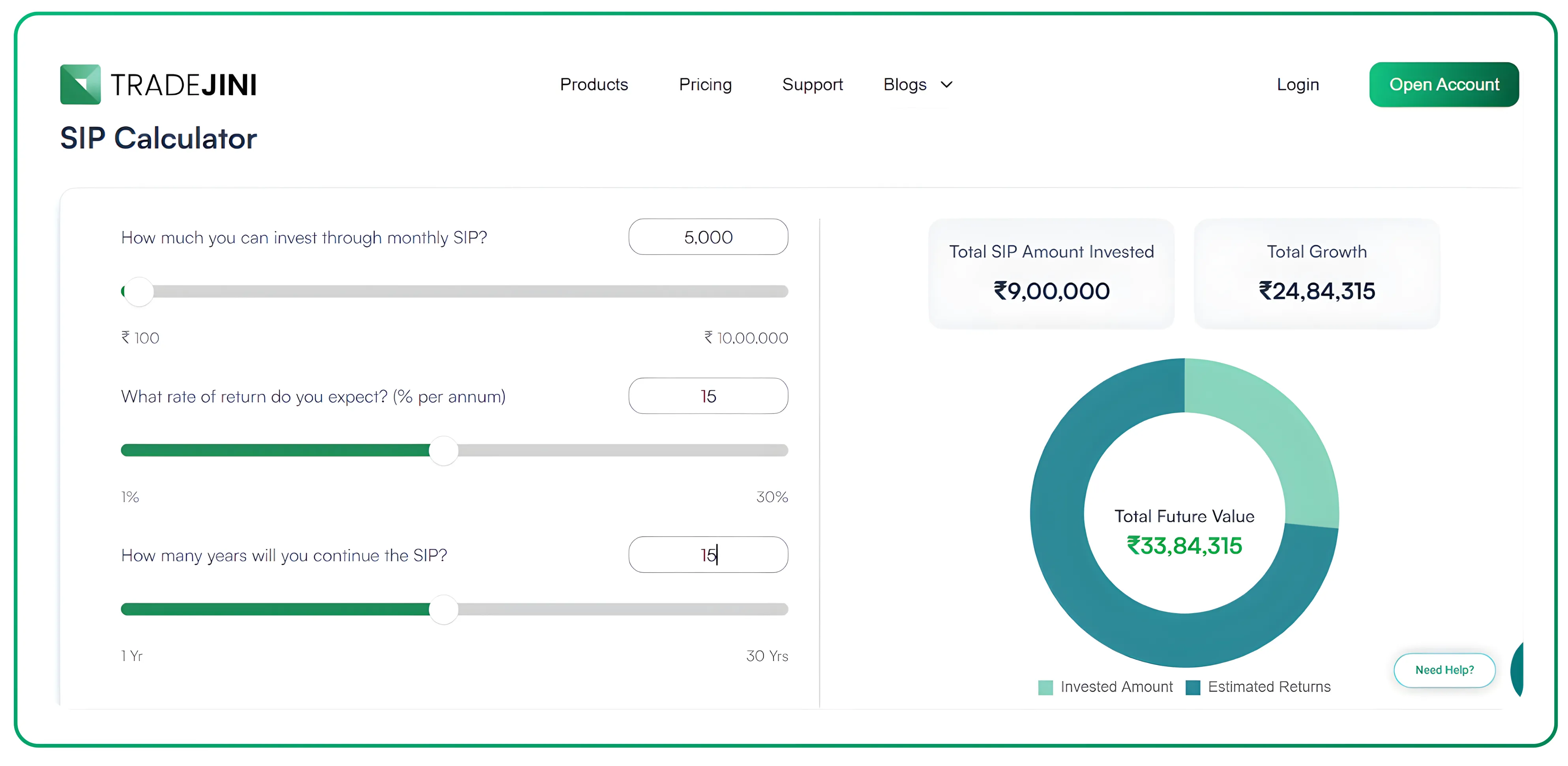

Using the Tradejini Calculator, a simple SIP of ₹5,000 per month at an assumed 15% return over 15 years shows a potential corpus of around ₹34 lakhs. Sounds impressive, right?

But here’s the real question, will this projection actually play out if you interrupt your SIP midway out of fear? Mutual funds work on the power of consistency and compounding, and any break in contributions directly impacts long-term returns.

So the thought to reflect on is: are short-term emotions worth sacrificing the long-term wealth that disciplined SIP investing can build?

Anchoring bias

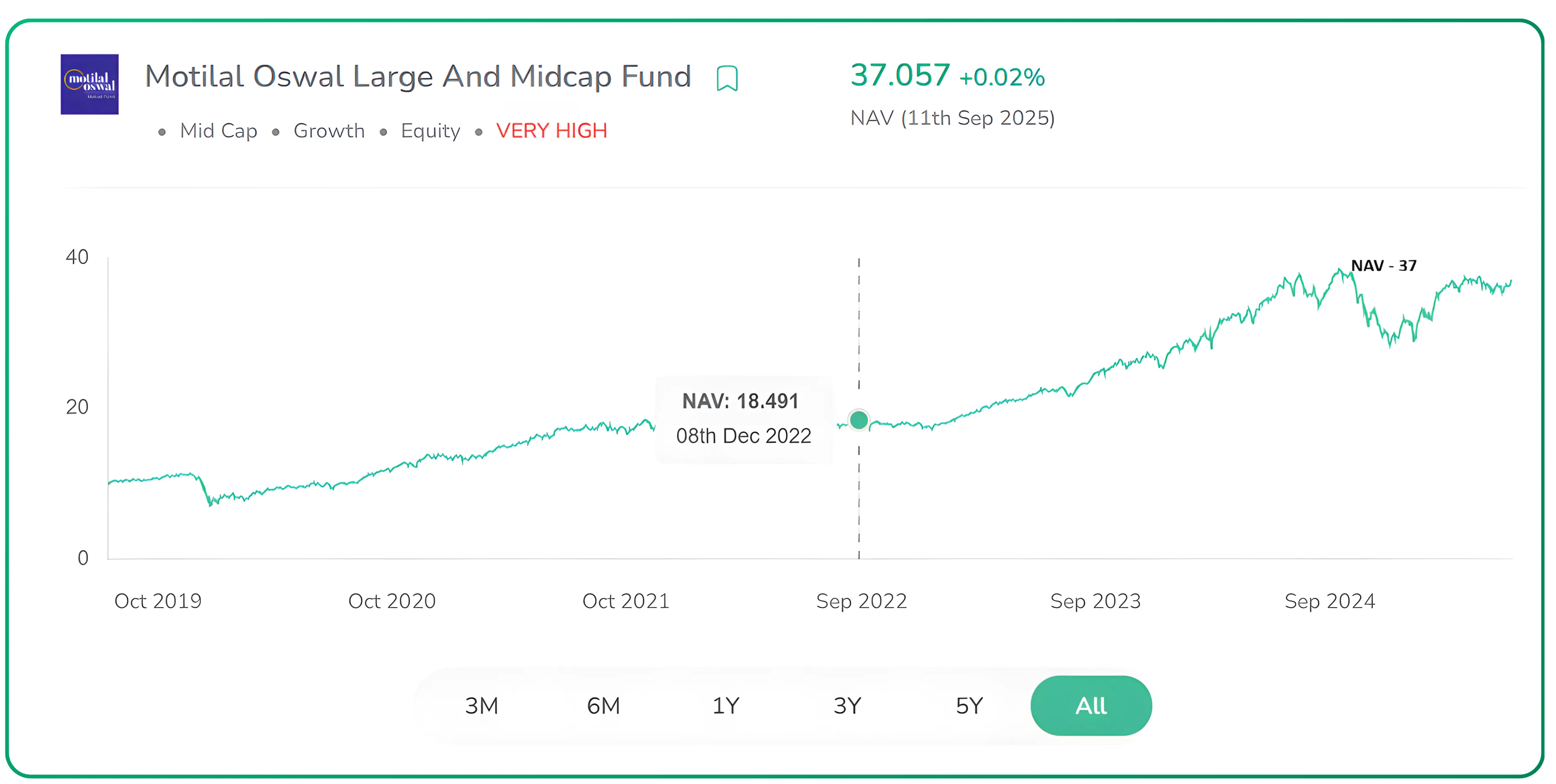

Anchoring makes investors wait for certain market levels that may never come. For example, in December 2022, the Nifty fell from 18,600 to about 17,000 by March 2023 and then started moving up again. Many investors kept waiting for the 16,000 level to buy, but the market never reached that level. Instead, it went on to rally through 2024 and 2025.

Now here’s the question: what did this hesitation cost them? Let's check on CubePlus; you will see the NAV of a fund was around ₹18 in December 2022, and by 2024–25 it had nearly doubled to ₹37. Isn’t it striking that simply waiting for a ‘better entry point’ meant missing out on years of compounding?

So the real question is, should we let such fixed numbers stop us from investing, or should we focus on staying invested and allow compounding to work in our favour?

Status quo bias

Despite mutual funds proving over time that they can beat inflation, many investors still keep their money in savings accounts or fixed deposits. This is often not about lack of awareness but about comfort with what feels safe. The real issue here is opportunity cost. By avoiding equity or hybrid funds, investors give up on the chance to earn a much higher CAGR. For many years, people believed the stock market was unsafe. But after COVID, more investors began to realise that equities can build wealth over the long term. Still, those who prefer complete safety often overlook an important point: it is inflation that quietly reduces the value of money. And when you compare returns over time, you notice that stock markets have consistently performed much better than fixed deposits.

For instance, Mrs. Sharma invested in FD lumpsum for 10 years And she invested in mutual funds through SIPs every month 5000, due to month on month investment compounding works more effectively with market cycles. As seen in the below table. So should investors still hold on to the comfort of fixed deposits, or should they rethink and ask if SIPs in mutual funds offer a better way to reach long-term goals?

| Mrs Sharma | FD 7% Return | Mutual Fund 15% |

|---|---|---|

| Invested Amount (10 years) | 600,000 | 600,000 |

| Amount After 10 Years | 9,83,000 | 13,15,000 |

Herd mentality

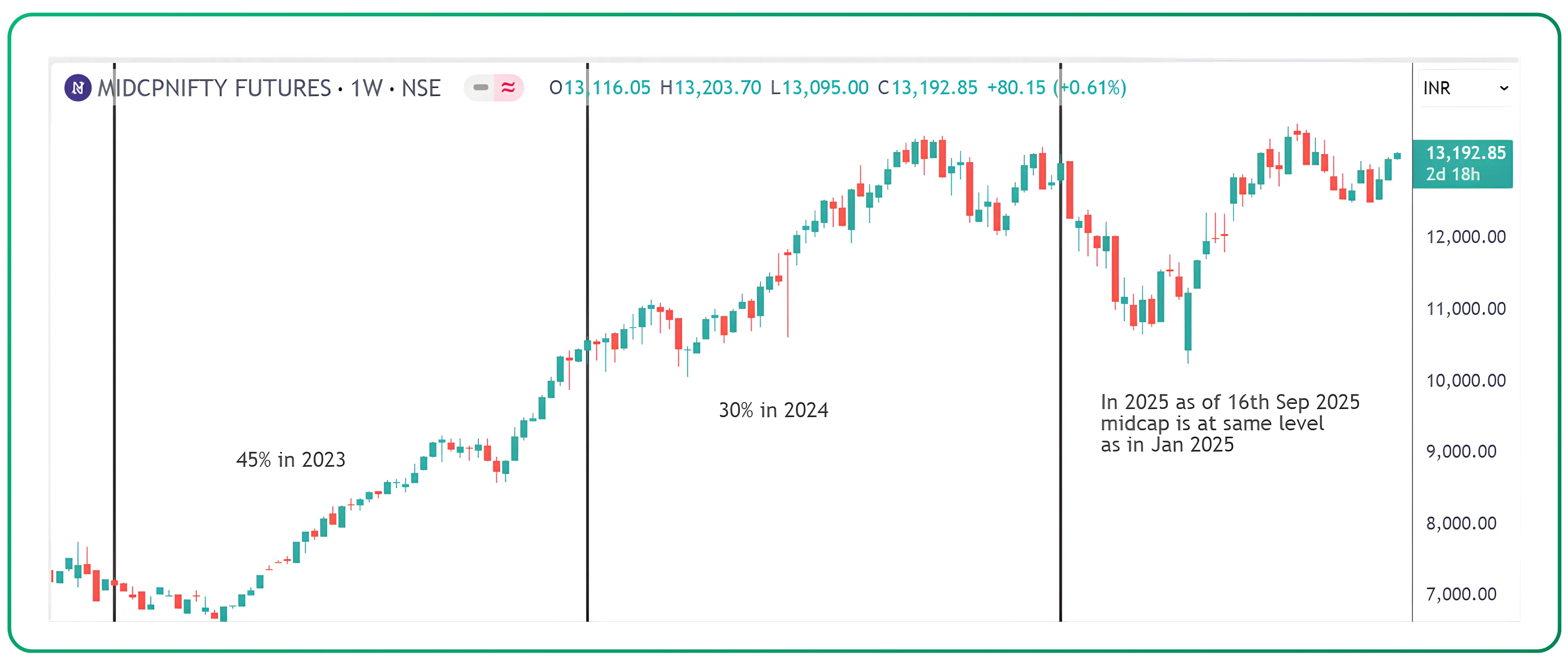

Investor inflows often peak during rallies, reflecting herd behavior. The rally of 2024–25 saw record mutual fund subscriptions, not because valuations were cheap but because of herd mentality. Conversely, inflows slow during corrections when funds are better priced. This herd mentality creates a buy-high, sell-low cycle, weakening long-term returns.

Similarly, Futures and Options (F&O) trading has become very popular among people chasing quick profits. But SEBI data shows that almost 91% of traders end up losing money in F&O. Many realise too late that the same money lost in these trades could have grown steadily if it had been invested through SIPs in mutual funds.

Instead of depending on luck and fast decisions, SIPs use discipline and compounding to build wealth slowly but surely.

This shows how herd mentality makes people follow risky trends, while truly long-term wealth is created through patient, consistent investing.

Also Read: https://www.tradejini.com/blogs/how-to-choose-best-mutual-funds-2025-wisely

Recency bias

Investors often extrapolate recent performance. If midcap funds delivered high returns last year, many assume the same will continue, leading to concentration in one category. Conversely, after a correction, investors shy away from equities, assuming prolonged weakness. Recency bias makes investors reactive rather than strategic, ignoring longer-term performance data that shows the benefits of consistent investing across cycles. Emotional decision-making based on short-term or recent performance increases risks.

Overcoming biases

Systematic investing: SIPs reduce timing risk and bring discipline.

Goal-based allocation: Linking investments to specific financial goals ensures focus beyond market swings.

Diversification: Spreading investments across equity, debt, gold, and other avenues reduces the risk of being overly exposed to any single asset or market condition.

Periodic review: Annual or semi-annual reviews prevent knee-jerk reactions to short-term moves.

Advisory support: Professional guidance can counter emotional decision-making with data-driven advice.

Behavior matters as much as markets

Market cycles are beyond investor control, but behavior is not. Data shows that mutual funds reward discipline and patience, yet biases often push investors toward suboptimal timing and allocation. Recognizing loss aversion, anchoring, herd mentality, and other biases is the first step. Building systems like SIPs, diversification, and goal-based investing is next.

Liked this post? Explore how to pick funds that align with your goals on CubePlus and take the next step in your wealth journey.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.