India's ceramic tiles and bathroom fittings sector stands at a turning point. The industry showed strong profit margins in Q2FY26 despite flat sales growth. Kajaria Ceramics posted its highest operating margins in three years at 18%. The sector faces short-term challenges from weak property market sales and price competition from unorganized Morbi manufacturers. However, long-term growth drivers from city expansion, government housing plans, and sector organization remain strong. India's tiles market is projected to grow from ₹531 billion in FY25 to ₹769 billion by FY29 at 9.7% CAGR. The bathroom fittings market will expand from ₹331 billion to ₹483 billion with 10% yearly growth. For stock investors, the opportunity lies in margin expansion stories and market share gains by organized players rather than top-line revenue growth.

Also Read: Inside India’s Ambitious Semiconductor Manufacturing Mission

Ceramic Industry in India: Market Size and Position

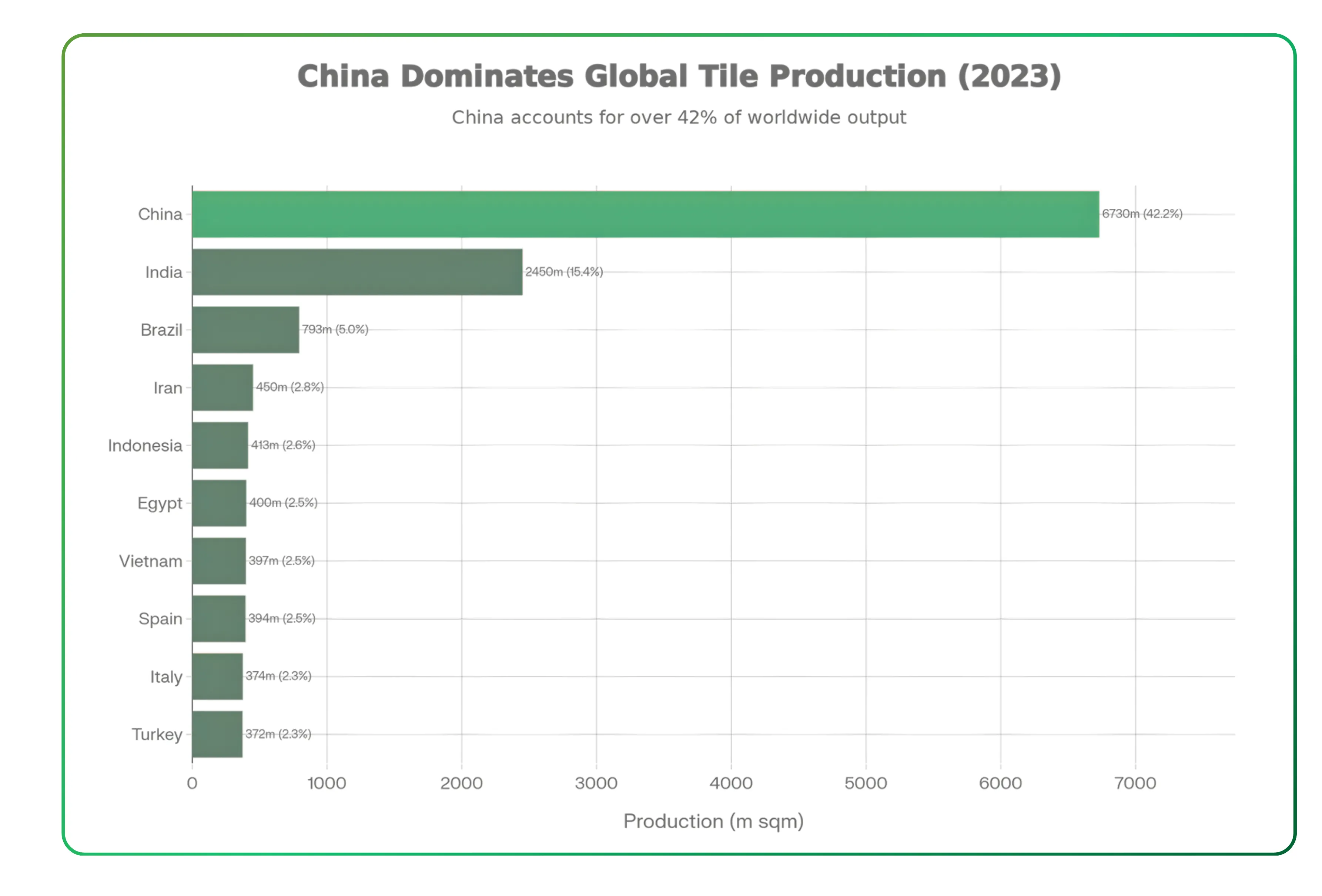

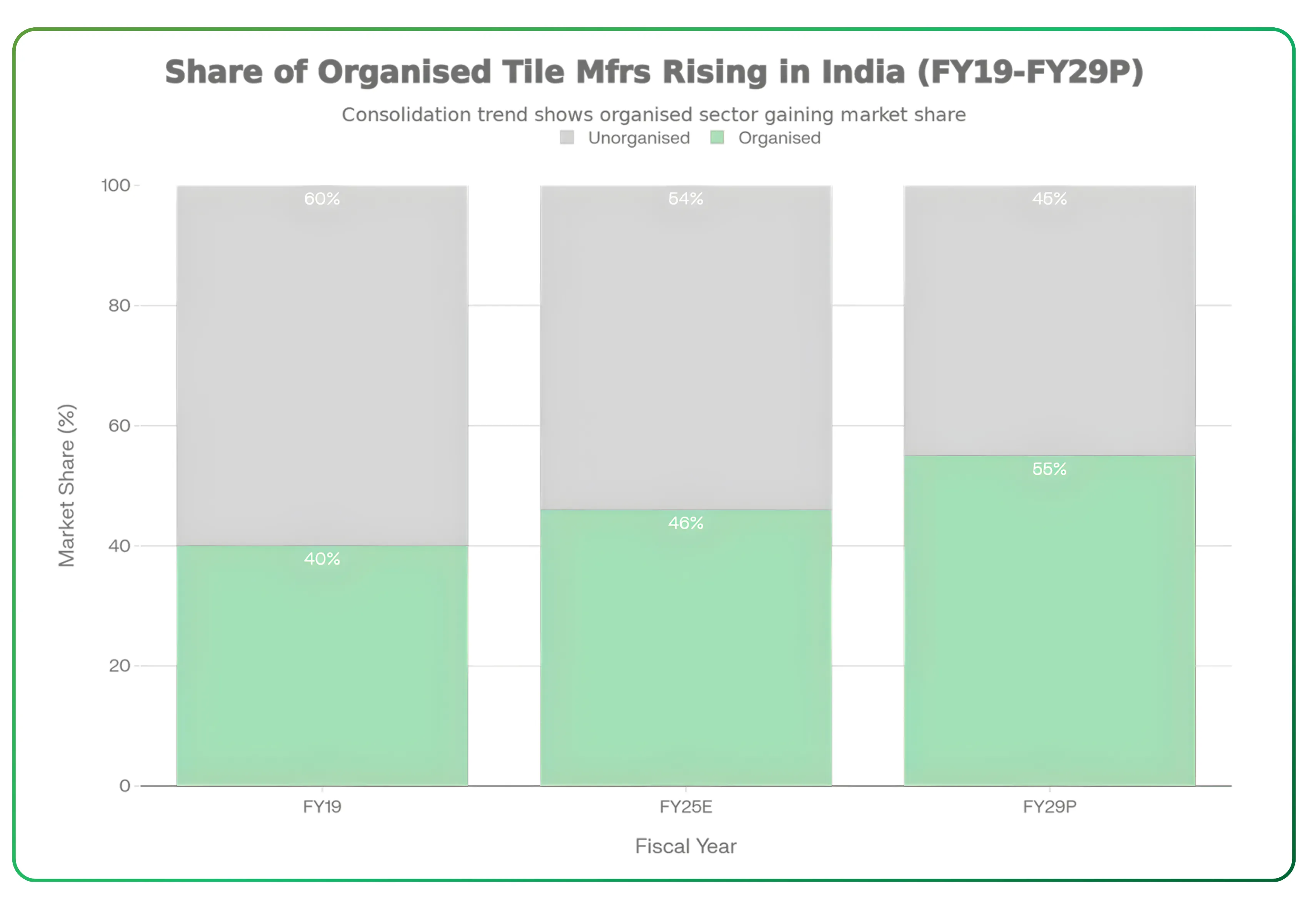

India ranks as the world's second-largest producer, consumer, and exporter of ceramic tiles globally after China. The country commands 11-15% of world production and 10.9% of global consumption. The Indian ceramic industry holds approximately 14% market share in global ceramic tile production. The domestic tiles market reached ₹531 billion in FY25, growing from ₹360 billion in FY19 at 6.7% yearly growth. However, growth in FY24 and FY25 slowed to approximately 3%. Organized players gained market share through volume growth while overall industry volumes remained flat.

The Indian ceramic tiles market size was USD 10.45 billion in 2025 and is forecast to reach USD 15.84 billion by 2030. The Indian ceramic tile industry is expected to grow at 8.2% yearly growth rate between 2023-2028. India is projected to produce more than 2 billion square metres of ceramic tiles in 2025. The market structure reveals that approximately 70% of ceramic manufacturers operate in the unorganized sector, making this a highly fragmented industry in India.

The market structure shows clear division. Organized players account for 46% of the tiles market in FY25, projected to reach 55% by FY29 as the sector becomes more organized. Kajaria Ceramics leads with 17% organized market share, followed by Somany Ceramics and Prism Johnson at 9% each. Asian Granito holds 6%, Varmora 5%, and Orient Bell 3%. The remaining 50% comprises unorganized manufacturers, primarily concentrated in Morbi, Gujarat.

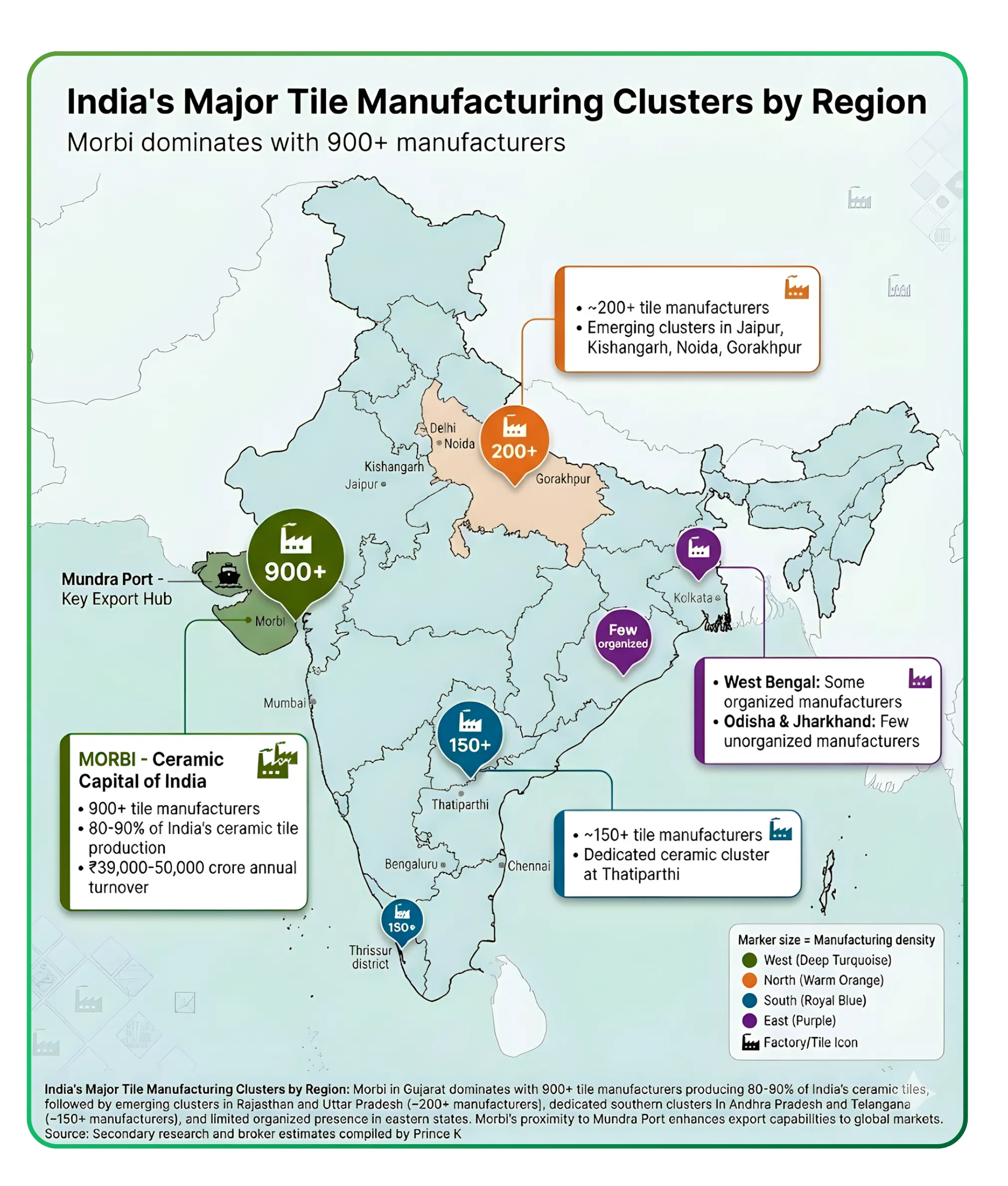

Morbi: The Ceramic Capital of India

Morbi in Gujarat serves as the heart of the ceramic industry in India. This cluster dominates the nation's ceramic tiles production with remarkable scale. Morbi accounts for approximately 80-90% of ceramic tile production in India, making it the undisputed leader. The cluster hosts approximately 900+ ceramic manufacturing units, creating a massive industrial ecosystem.

Morbi's economic contribution is substantial. The annual turnover is estimated at ₹39,000-50,000 crores, far exceeding earlier estimates. Exports from Morbi reach approximately ₹15,000-17,500 crore annually in 2024-25. Morbi contributes approximately 13% to global ceramic manufacturing, showcasing its international significance. The cluster benefits from abundant local raw materials, favorable location near Mundra Port enhancing export capabilities, and government support through subsidies and incentives. Looking ahead, Morbi aims to double its ceramic output by 2027 and reach a turnover of ₹80,000 crore.

Manufacturing capacity beyond Morbi has expanded to new regions. New manufacturing centers have emerged in Rajasthan in the North and Andhra Pradesh and Telangana in the South. This geographic expansion helps ceramic manufacturers reduce dependence on a single production cluster. Kajaria expanded its southern presence with facilities in Andhra Pradesh and a 59% stake in a Telangana subsidiary. Somany established manufacturing in Tirupati, Andhra Pradesh, strengthening its footprint across India.

Product Evolution and Market Segments

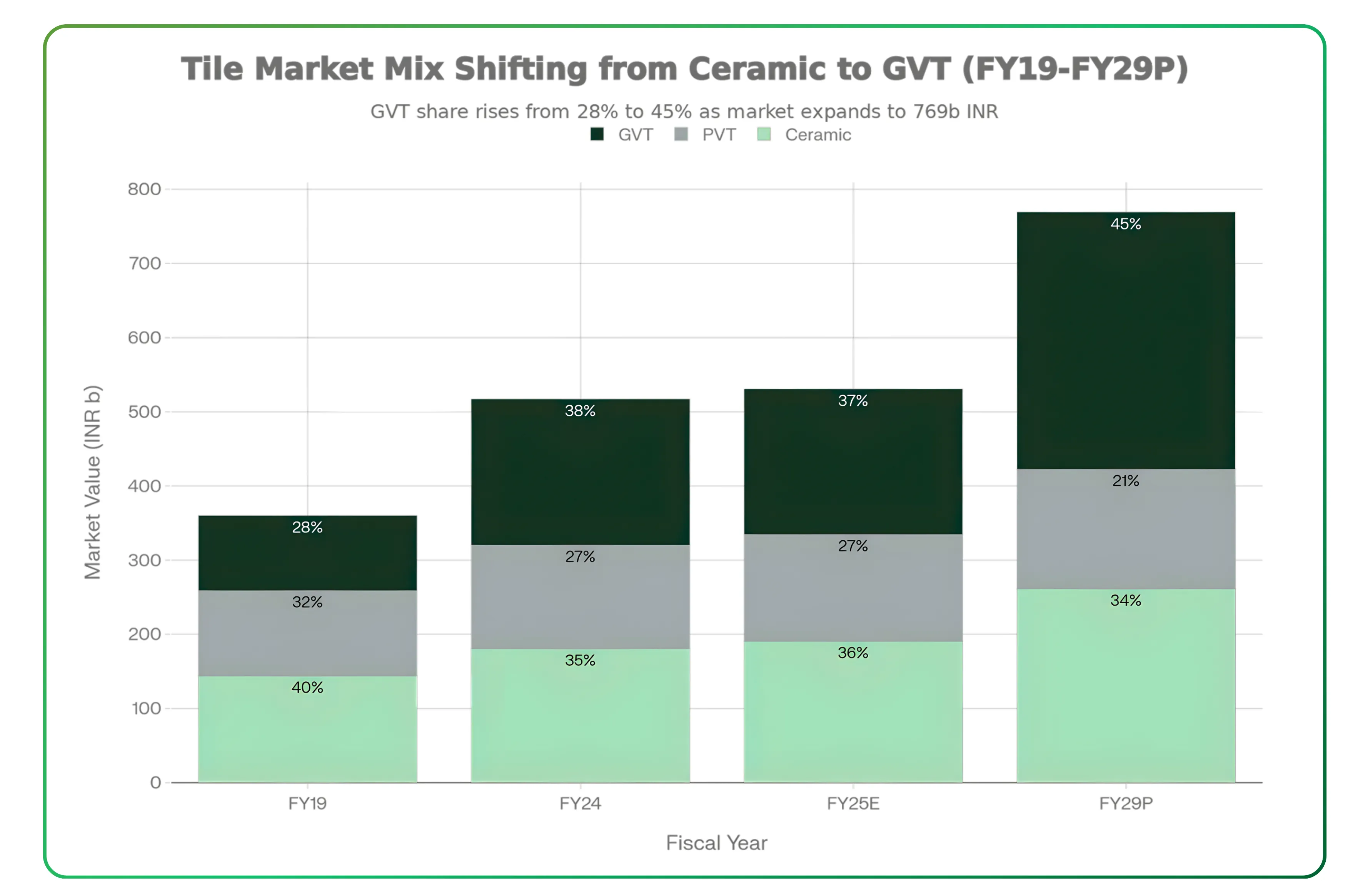

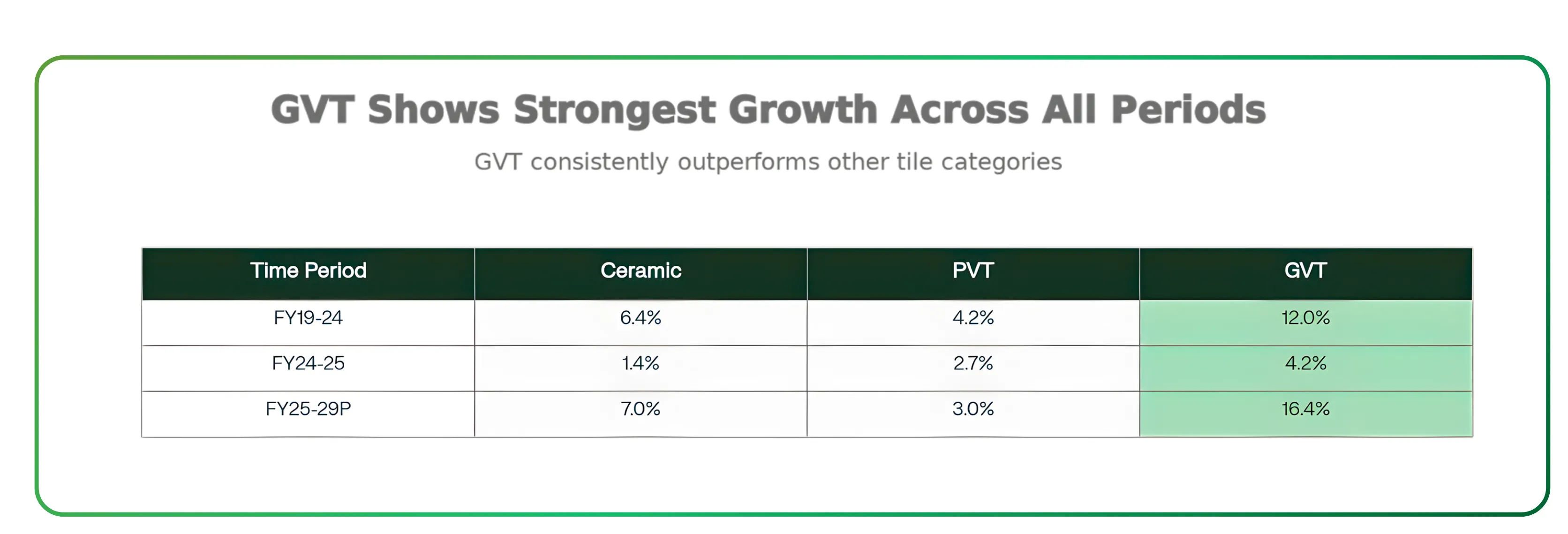

Product mix evolution shows glazed vitrified tiles gaining market share rapidly across the ceramic industry in India. In FY19, when the total market stood at ₹360 billion, ceramic tiles comprised 40% of market value, polished vitrified tiles 32%, and glazed vitrified tiles 28%. By FY29, this is projected to shift dramatically as the market expands to ₹769 billion, with ceramic tiles at 34%, polished vitrified tiles 21%, and glazed vitrified tiles commanding 45% share. Glazed vitrified tiles demonstrate the strongest growth trajectory across all time periods, growing at 12.0% yearly (FY19-24), 4.2% (FY24-25), and projected 16.4% (FY25-29P). In comparison, ceramic tiles grew at 6.4%, 1.4%, and 7.0% respectively, while polished vitrified tiles showed 4.2%, 2.7%, and 3.0% growth across the same periods. This sustained outperformance reflects consumer preference for premium, large format tiles with better aesthetics and durability in both residential and commercial projects.

The bathroom fittings market reached ₹331 billion in FY25, growing 10.3% year over year from ₹300 billion in FY24. The segment is projected to reach ₹483 billion by FY29 with 10% yearly growth rate. The market divides into toilet fittings accounting for 39% and bath fittings comprising 61%. The toilet fittings segment is highly organized at approximately 75% and concentrated among few players, with top three players Roca, Hindware, and Cera commanding 60% to 70% combined market share. This segment, being more widespread, is projected to grow at 7% yearly. Bath fittings will expand at 11.7% yearly, driven by low usage rates and increasing home renovation frequency across India. The tap and faucet market is approximately 60% organized but highly scattered, presenting consolidation opportunities. Jaquar leads with 15% to 20% market share, followed by Cera and Hindware at 4% to 5% each.

Also Read: 9 Smart Money Moves for 2026

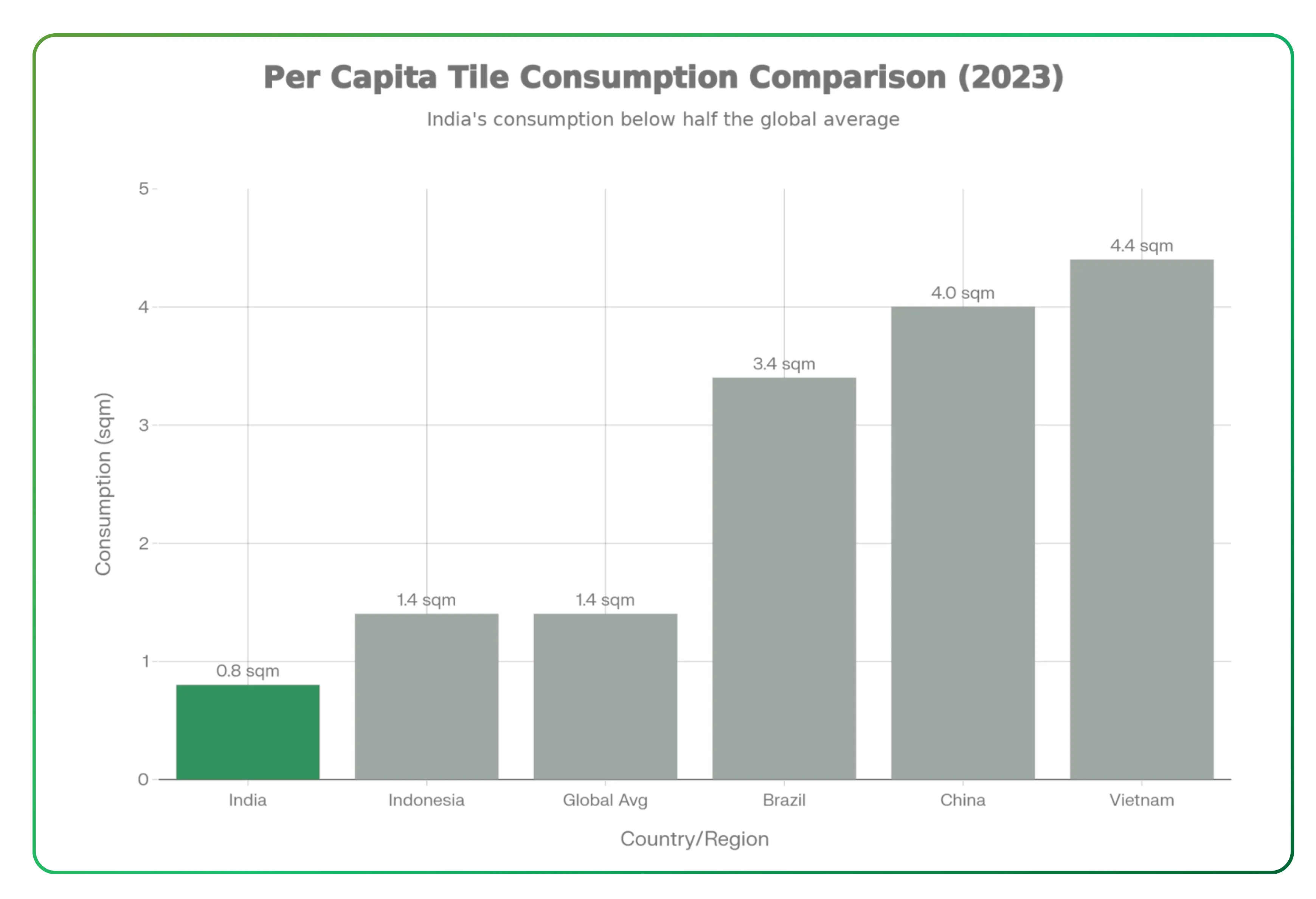

India's per person tile consumption stands at just 0.8 square meters, significantly below the global average of 1.4 square meters and far behind major markets like Brazil at 3.4 square meters, China at 4.0 square meters, and Vietnam at 4.4 square meters. This consumption gap represents substantial growth potential for the ceramic industry in India. By FY29, India's per person consumption is expected to reach 1 square meter, marking a 25% increase. This growth will come from multiple drivers including increasing property development across residential and commercial sectors, growing market share of ceramic tiles over traditional alternatives like marble and natural stone, and expanding use cases across floors, walls, bathrooms, kitchens, and commercial spaces including offices, hotels, and retail establishments.

Raw Materials and Cost Advantages

India's cost advantage creates favorable manufacturing economics compared to developed markets in Europe and North America, with labor costs running 40% to 60% lower than established hubs. Natural gas, the primary variable input cost, comprises approximately 18% to 20% of total production costs for tiles manufacturers. The availability of raw materials like clay, quartz, and other minerals in Gujarat and nearby regions supports cost-effective production. The domestic consumption base of ₹531 billion provides assured demand for ceramic manufacturers, helping reduce dependence on volatile export markets. While exports reached ₹160 billion in FY25, domestic sales account for approximately 70% of total revenue for major listed players, shielding companies from trade policy uncertainties and allowing focus on higher margin retail channels.

Also Read: ABS Marine Anchoring Growth with Long-term Offshore Contracts

Distribution network represents a key structural advantage for organized players in the industry in India. Kajaria operates 430 exclusive brand outlets and 1,850 dealers nationwide, while Somany maintains 474 exclusive outlets and 2,675 dealers across the country. This extensive distribution network built over decades creates substantial barriers to entry and provides organized players with reach into smaller cities where unorganized competition faces limitations. Brand value and product innovation capabilities further differentiate organized ceramic manufacturers, with companies investing heavily in design development and maintaining international partnerships for technology access.

Government Support and Policy Framework

Government housing programs provide structural demand support for the ceramic industry. The Pradhan Mantri Awas Yojana urban housing scheme targets construction of affordable housing units across India, creating baseline demand for ceramic tiles and bathroom fittings in residential houses. The Gujarat government has provided substantial assistance of over ₹115 crore to more than 2,200 beneficiaries in recent years, supporting the ceramic industry growth in Morbi. State level incentives for manufacturing expansion, particularly in Andhra Pradesh and Telangana, include subsidized land allocation, power tariff concessions, and capital subsidy support. The goods and services tax implementation speeds up the organization of the construction and building materials sectors, with organized ceramic manufacturers benefiting from compliance capabilities and ability to serve developers requiring GST compliant billing. This regulatory shift gradually reduces the cost advantage of unorganized Morbi manufacturers operating with limited compliance.

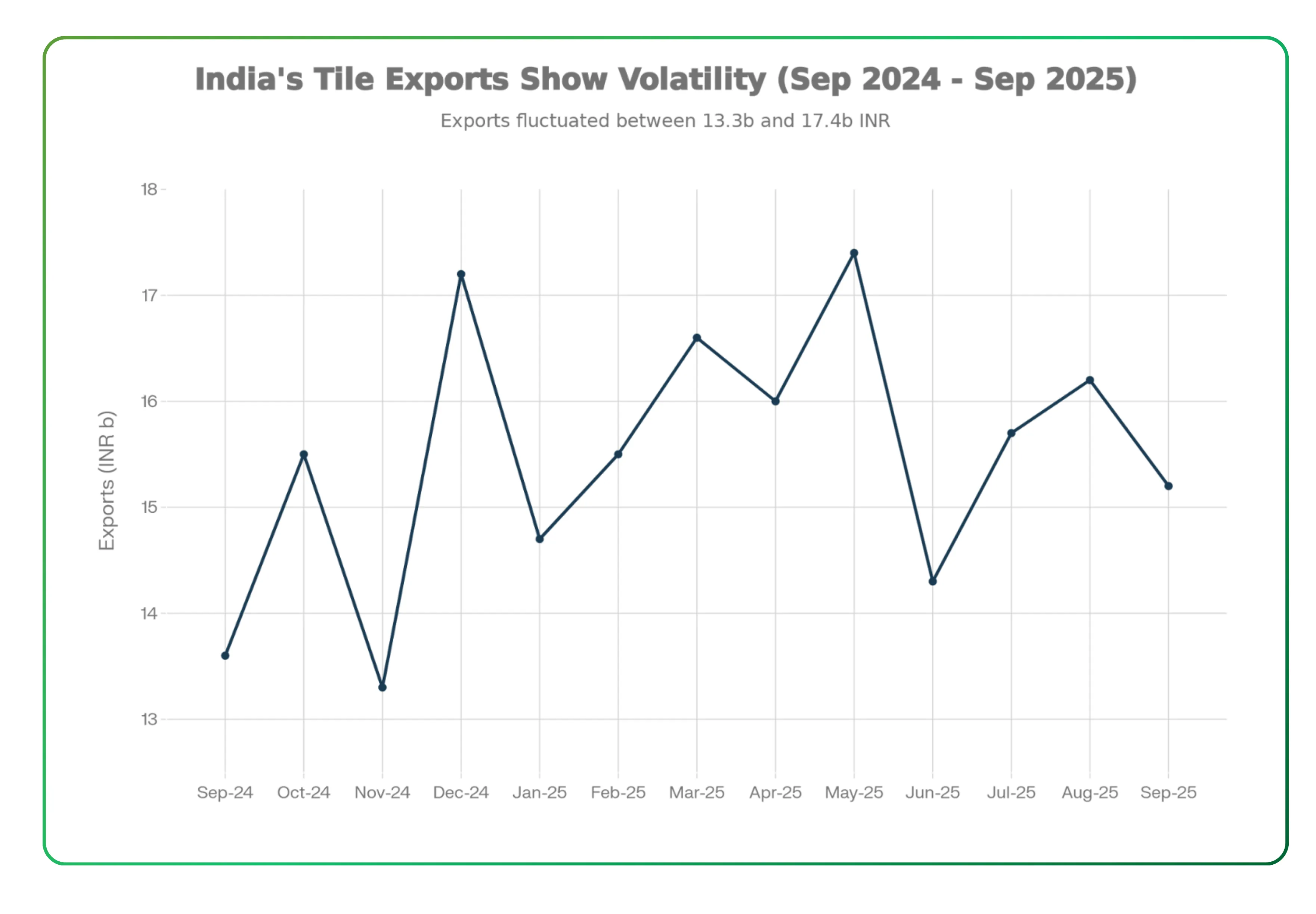

Anti dumping duties developments present mixed results for Indian ceramic tile exporters. The US Commerce Department's April 2025 decision found no evidence of dumping by Indian ceramic tile exporters to the USA, with countervailing duty rates set at 3.06% to 3.45%, relatively low levels. This preserved access to the largest export market while eliminating potential protection from Chinese imports. Mexico started anti dumping investigations in August 2025, potentially restricting future export opportunities and redirecting capacity to domestic markets. These developments affect India's position as major exporters to Latin America and other countries.

Largest Ceramic Manufacturer and Major Companies

Kajaria Ceramics Limited

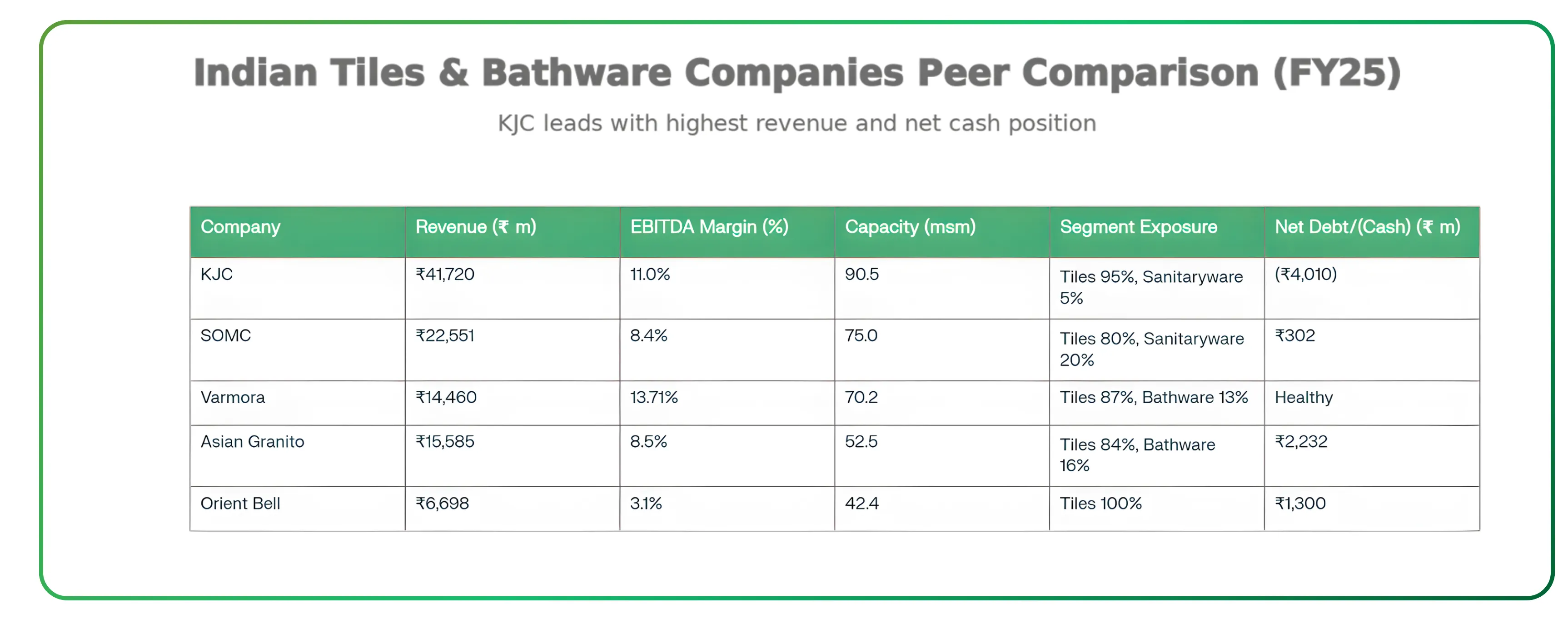

Kajaria Ceramics leads the Indian ceramic industry with 17% organized market share and operates total tile capacity of 87.80 million square meters across 9 plants. Major facilities include Gailpur Rajasthan (35.95 msm), Morbi Gujarat (17.90 msm), Sikandrabad UP (8.80 msm), Srikalahasti Andhra Pradesh (8.80 msm), and operations in Telangana and Nepal. The company also operates bathroom fittings capacity of 12 lakh toilet pieces and 1.60 million taps annually. Key strengths include largest production capacity among organized players, geographic diversification across India, strong distribution network with 430 exclusive outlets and 1,850 dealers, and negative net debt of ₹593 crore providing financial flexibility.

Somany Ceramics Limited

Somany operates 75 million square meters tile capacity across 6 facilities with 75% capacity utilization. Major plants include Bahadurgarh Haryana (23.32 msm), Tirupati Andhra Pradesh (8.40 msm), Ahmedabad Gujarat (11.15 msm), and Morbi Gujarat (12.04 msm). The company also operates 0.48 million pieces toilet fittings capacity at 74% utilization and 1.30 million taps annually at optimal utilization. Key strengths include 474 exclusive outlets and 2,675 dealers nationwide, 4.5 million square meter Max plant commissioned in January 2024 for premium large format glazed vitrified tiles, and diversified sales mix with own manufacturing (27%), joint ventures (32%), and outsourced tiles (41%). The company focuses on maximizing existing capacity utilization to 95-100% with zero major capacity additions planned for next 18 months.

Cera Sanitaryware Limited

Cera operates toilet fittings manufacturing capacity at 85% utilization and tap manufacturing capacity at 97% utilization, approaching full capacity constraint. The company maintains strong cash position of ₹778 crore and posted revenue of ₹488 crore in Q2 FY26 with operating profit of ₹67 crore. Revenue mix shows toilet fittings (47%), taps (40%), tiles (11%), and wellness (2%). Key strengths include Senator luxury brand with 28 stores targeting 45-50 stores by FY26 end, Polipluz brand for smaller cities with 38 distributors and 650 dealers targeting 100 distributors and 2,000 dealers by March 2026, comprehensive Dealer Management System covering 200+ dealers providing real-time sales visibility, diversified product positioning across premium (42%), mid (36%), and entry segments (22%), and efficient cost management with gas costs at 3.6% of revenue. High capacity utilization levels indicate strong demand, with tap segment nearing capacity limits. Both new brands combined target ₹40-45 crore revenue in H2 FY26, scaling to ₹150 crore by FY27.

Orient Bell Limited

Orient Bell operates 42.4 million square meters tile capacity across 5 plants with consolidated capacity utilization at 68% in Q2 FY26, improved from Q1 levels and year-over-year comparison. The mother plant at Sikandrabad performed particularly well, while southern plants at Dora and Hoskote operated at lower utilization reflecting regional demand variations. Key strengths include strong cost management with manufacturing costs reduced 3.7% on like-for-like basis, successful operational turnaround with gross margins expanding to 39%, profit before tax reaching ₹3.9 crore versus ₹0.8 crore in Q2 FY25, and H1 FY26 profit of ₹3.3 crore marking strong recovery from loss of ₹1.2 crore in H1 FY25. The company demonstrates operational efficiency improvements despite moderate capacity utilization, with geographic sales distribution showing tier 3 cities leading at 41%, tier 1 at 36%, and tier 2 at 23%.

Also Read: Exploring the Financial Dashboard on CubePlus

Investment Perspective and Market Valuation

Sector valuations reflect market recognition of margin recovery potential balanced against execution risk on demand timing. Kajaria's premium valuation is justified by consistent execution, market leadership as the largest ceramic manufacturer in India, and superior margin profile. Somany represents attractive value entry assuming management delivers on debt reduction and margin expansion guidance. Cera's valuation reflects strategic investment phase with near term margin pressure but long-term brand building in luxury and entry segments.

The margin expansion story drives investment thesis more than revenue growth in the current scenario. Kajaria's margin expansion of nearly 4.5 percentage points in Q2 FY26 demonstrates operational leverage potential. This happens when companies focus on cost optimization, product mix improvement toward premium porcelain tiles and glazed vitrified tiles, and working capital efficiency rather than chasing volume growth in weak demand environment. The ability to expand margins despite flat revenues shows management quality and operational excellence.

Cash generation capability supports dividend payments and balance sheet strength across organized players. Kajaria maintains negative net debt meaning cash surplus, enabling consistent dividend payouts and financial flexibility for growth. Cera's ₹778 crore cash position provides strategic flexibility for expansion, new brand launches, and maintaining interest in growth opportunities. Somany prioritizes debt reduction over dividends near term but should resume shareholder distributions after balance sheet improvement, making it attractive for long-term investors.

Challenges Facing the Sector

Industry Challenges, Impact, and Expected Resolution

| Challenge Area | Impact on Industry | Expected Resolution |

|---|---|---|

| Natural Gas Prices | Natural gas comprises 18–20% of production costs. Indian natural gas prices declined to ₹316.50 per mmbtu as of January 2026 from elevated mid-2025 levels. However, global energy market changes create ongoing uncertainty. A 10% gas price increase translates to roughly 2 percentage point margin impact without pricing power. | Near-term benefit from price reduction provides 0.5–1 percentage point margin improvement. Long-term volatility remains based on global energy dynamics and demand from Middle East and other regions. |

| Export Markets | India exported ₹160 billion tiles in FY25, down 20% year-over-year due to Cyclone Biparjoy disrupting Morbi operations. USA remains largest export market followed by UAE, Iraq, Mexico, and Kuwait. Mexico's August 2025 anti-dumping investigations create potential for restricted access. | Exporters may redirect volumes to domestic markets or other countries, intensifying domestic competitive pressure. USA market access preserved with low 3.06–3.45% countervailing duties. Focus may shift from Latin America to other growth markets. |

| Environmental Compliance | Environmental compliance and waste management regulations increase operational costs. New norms for emissions, water usage, and waste disposal require capital investments and ongoing compliance expenses. Hydrogen-ready kilns and eco-friendly technologies being adopted. | Organized players better positioned to manage compliance costs through scale and technology adoption. Unorganized sector faces pressure, accelerating market share shift. Government subsidies may ease transition costs. |

| Skilled Labor Shortage | Shortage of trained technicians and masons affects installation quality and customer satisfaction. Limits rapid expansion in tier 2 and tier 3 cities where demand is growing. | Industry associations and companies investing in training programs. Technology-led installation improvements and partnerships with vocational institutes emerging as solutions. |

| Property Sector Cycles | 70–80% of demand from new construction and 20–30% from renovation, tying growth to property cycles. Shift toward premium housing raises realization but limits unit volume growth. | Increased focus on renovation demand. Shorter replacement cycles. Commercial real estate (offices, hotels, retail) providing incremental demand beyond residential sector. |

Future Outlook and Growth Trajectory

| Time Period | Key Projections | Growth Drivers |

|---|---|---|

| Near Term (H2 FY26 to FY27) | • Tiles market: ₹531 billion to ₹769 billion by FY29 • Bathroom fittings: ₹331 billion to ₹483 billion by FY29 • Demand recovery expected in H2 FY26 • Gas price reduction providing 0.5–1 percentage point margin benefit • Organized market share from 46% to 55% by FY29 |

• Pickup in property construction activity • Government infrastructure and housing schemes • Renovation demand from existing homes • Market share gains by organized players • Tightening compliance favoring organized sector |

| Medium Term (FY27 to FY29) | • Industry growth: 9–10% CAGR • Organized players growth: 12–15% CAGR • Per capita consumption: 0.8 → 1.0 sq. meters • Glazed vitrified tiles share: 29% → 45% • Global rank maintained at #2 after China |

• Urbanization and city expansion • Rising incomes driving higher per capita consumption • Formalization boosting organized share • Product premiumization (porcelain, wall, floor, mosaic tiles) • Brand equity and distribution scale advantages |

| Structural Themes | • Market consolidation among organized players • Technology adoption (fiber optics, automation) • Sustainability focus with hydrogen-ready kilns • Geographic expansion beyond traditional clusters • Export growth to Europe, USA, Middle East despite selective duties |

• Capital availability favoring organized players • Consumer shift toward branded products • Focus on quality and durability • Government support for manufacturing • Improving ease of doing business • Rising institutional investor interest |

The Indian ceramic tiles and bathroom fittings sector is moving from cyclical demand driven story to structural margin and market share consolidation story. Organized player margin growth through cost management, product mix improvement toward premium categories, and distribution optimization is outpacing revenue slowdown. This implies positive earnings revisions for well-managed companies like Kajaria Ceramics, the largest ceramic manufacturer in India.

Also Read: Thinking Like a Turtle | How Traders & Investors See Market Differently

The sector benefits from multiple tailwinds including rising urbanization, growing housing demand, increasing preference for tiles over marble and granite, and expanding use of ceramic products in commercial spaces. The formalization of the unorganized sector through stricter compliance norms and government support for organized manufacturing creates additional opportunities. Companies investing in brand building, distribution expansion, and technology upgrades are positioned to capture disproportionate market share gains. The ceramic industry in India stands at an inflection point where operational excellence and strategic positioning matter more than ever for generating shareholder value.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.