India's semiconductor story is moving from policy announcements to actual execution. With 10 approved projects representing ₹1.60 lakh crore (approximately $19.5 billion) in investment, the question for investors is no longer "if" but "when" and "who benefits." The India Semiconductor Mission has committed ₹65,000 crore of its ₹76,000 crore budget, and the first chips from Indian facilities are expected in 2026. For equity investors, the opportunity lies not in fabrication facilities with multi-year timelines, but in packaging operations and semiconductor-adjacent electronics manufacturing that will see revenue traction within 12 to 24 months.

Industry Overview and Market Size

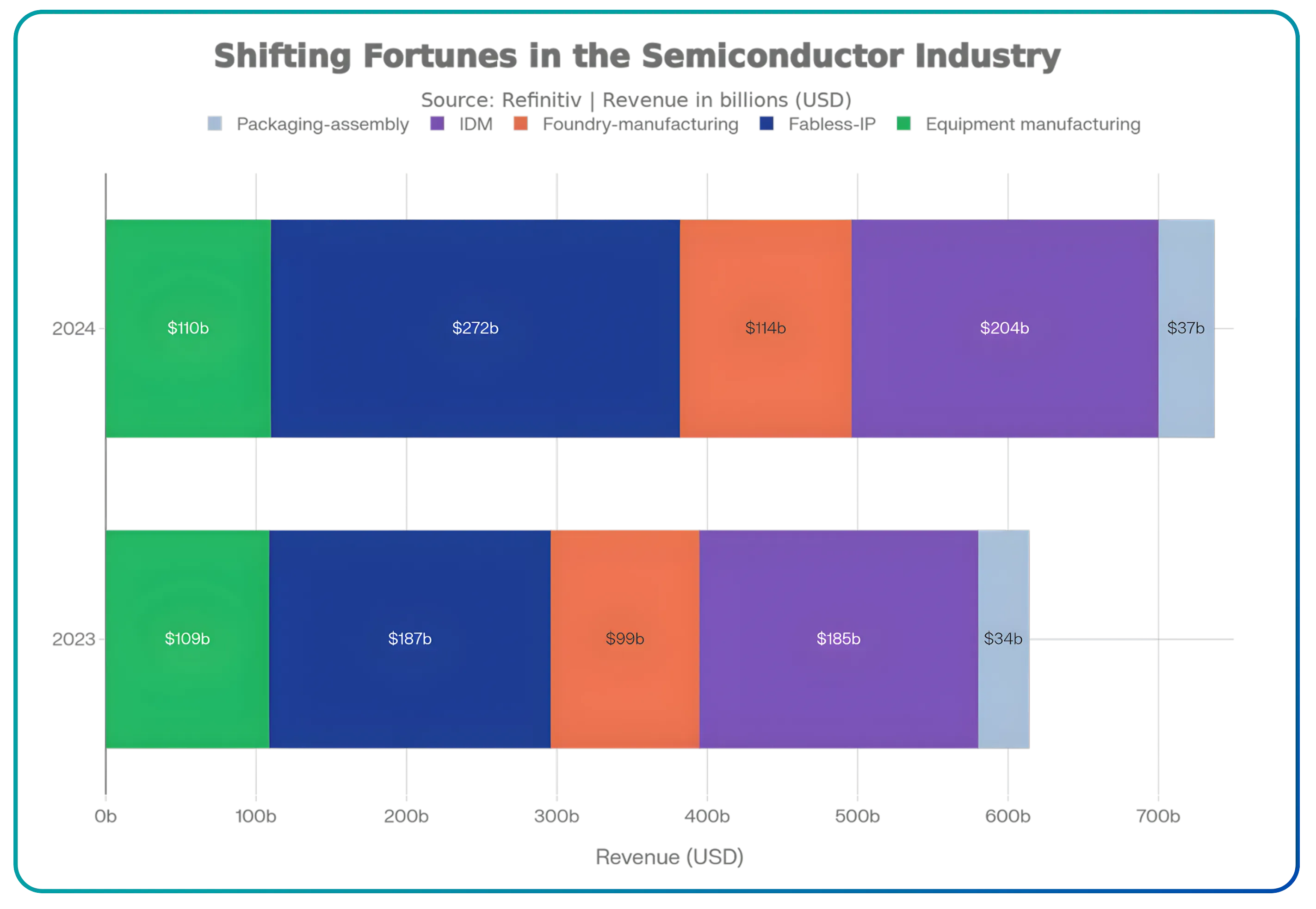

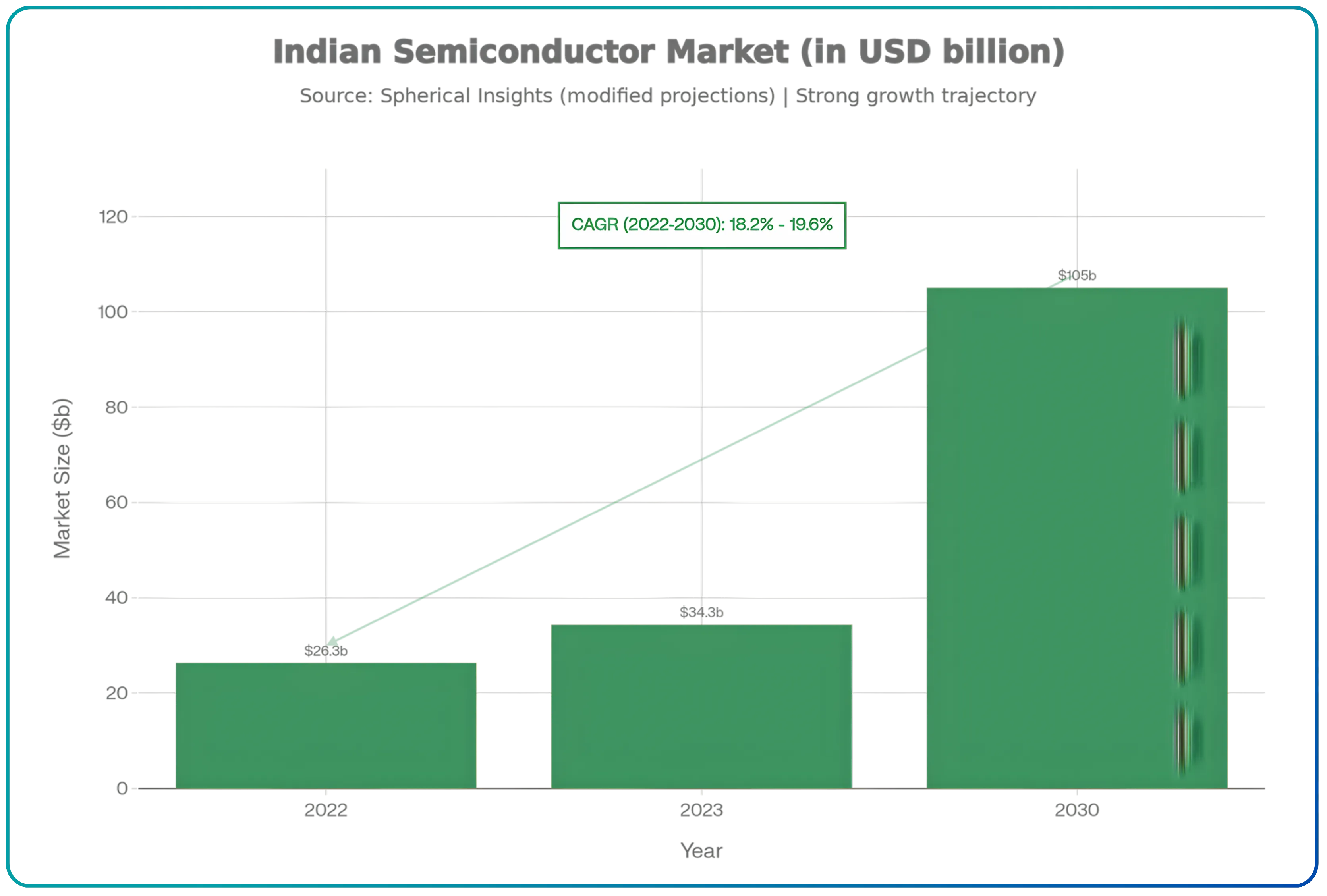

The global semiconductor industry posted 19% sales growth in 2024, reaching $697 billion, driven primarily by artificial intelligence and data center demand. India's semiconductor market tells a different story. Valued at $45 to $50 billion in FY2025, the market is projected to reach $100 to $110 billion by 2030. This growth comes almost entirely from consumption, not manufacturing. India imports nearly all its semiconductor requirements today.

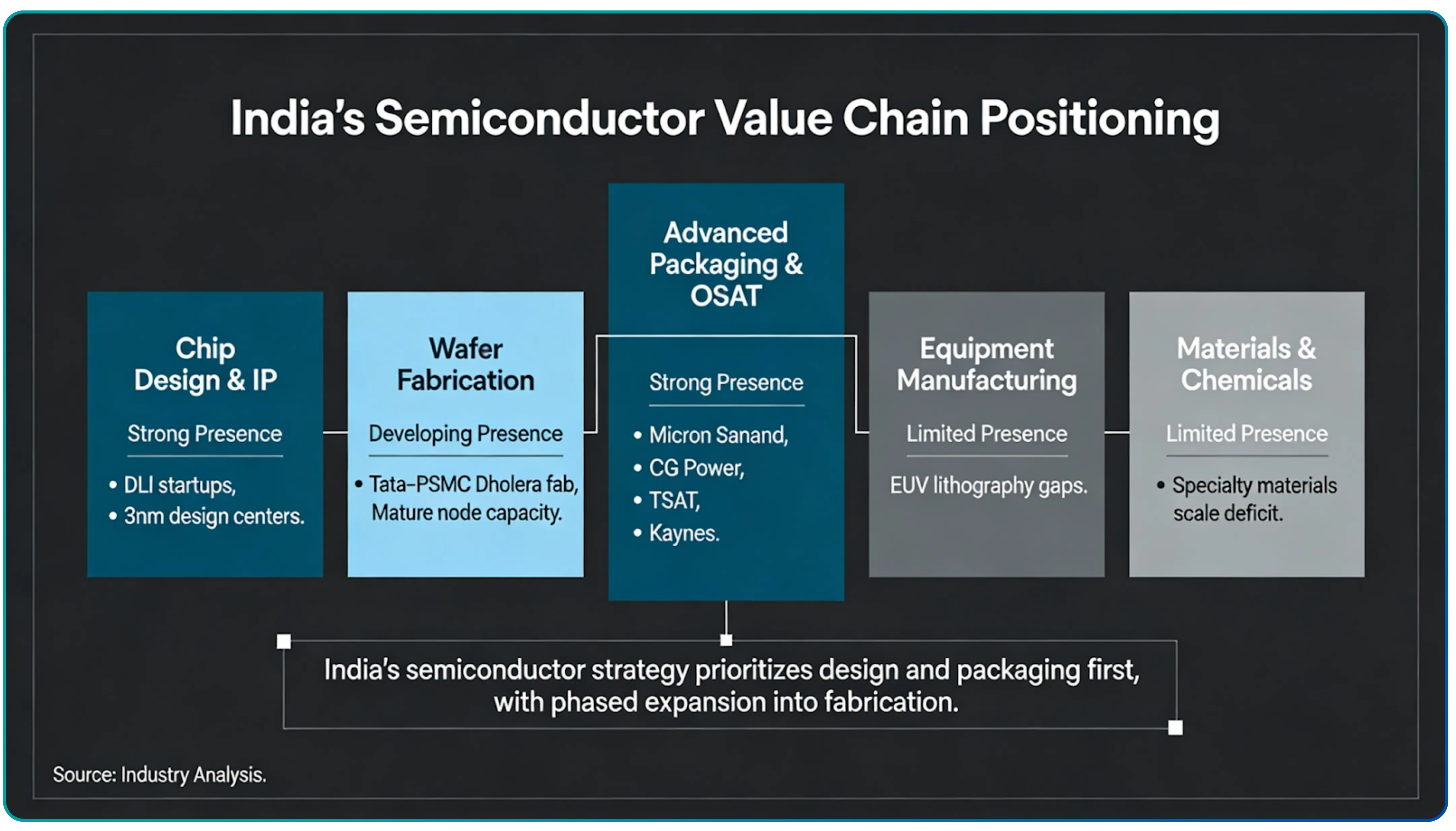

The domestic manufacturing build-out is happening across three segments. First, outsourced semiconductor assembly and test facilities where chips are packaged and tested. These require lower capital investment (₹3,000 to ₹27,000 crore per project) and can generate revenue within 18 to 24 months of commissioning. Second, logic fabrication facilities where silicon wafers are actually manufactured. These need massive capital (₹91,000 crore for Tata Electronics Dholera) and take four to five years from groundbreaking to first revenue. Third, compound semiconductors like silicon carbide for electric vehicle power electronics, still in early approval stages.

For investors, the timeline difference matters. Assembly and test operations will contribute to listed company financials starting 2026 to 2027. Fabrication revenue appears only post 2028, if execution goes according to plan.

India's Structural Advantages

India brings three structural advantages to semiconductor manufacturing. First, a large and growing engineering talent pool with over 1.5 million engineering graduates annually. The challenge is specialized semiconductor training, which the government is addressing through dedicated programs targeting 85,000 semiconductor professionals over 10 years. Second, lower operational costs compared to established hubs like Taiwan and South Korea. Labor costs run 40% to 60% lower, though this advantage narrows for capital-intensive fabrication where equipment costs dominate. Third, a massive domestic end market consuming $45 to $50 billion of chips annually, providing assured demand for automotive, industrial, and consumer electronics applications.

The demographic advantage is real but constrained. The semiconductor industry needs to grow from 345,000 professionals today to 460,000 by 2030. However, approximately 67,000 technical positions may remain unfilled due to limited pipeline of specialized graduates. This talent bottleneck will constrain how fast new facilities can ramp production, creating wage inflation in the process.

Also Read: The Datacenter Boom Fueling the AI Revolution

Regulatory Tailwinds and Policy Support

The India Semiconductor Mission provides up to 50% fiscal support for approved projects, making the economics work for global companies. Micron Technology's ₹22,516 crore assembly facility in Gujarat receives substantial government backing. Tata Electronics' ₹91,000 crore fabrication facility benefits from a similar support structure, though the company has not disclosed exact subsidy amounts.

Beyond capital subsidies, the Design Linked Incentive scheme supports chip design startups with funding and access to expensive Electronic Design Automation tools. Twenty-three design projects have been sanctioned, with 278 academic institutions and 72 startups receiving tool access. This creates a pipeline of intellectual property and design talent, though commercial revenue from design services remains small scale today.

State governments are competing aggressively. Gujarat has secured multiple projects including Micron, Tata Electronics, and CG Power facilities through land allocation, power infrastructure, and additional fiscal incentives. This state-level competition accelerates project timelines and reduces execution risk.

Approved Projects: The Investment Pipeline

| Company | Location | Project Type | Investment (₹ Cr) | Status | Expected Commissioning |

|---|---|---|---|---|---|

| Micron Technology | Sanand, Gujarat | OSAT | 22,516 | Under construction | 2025–2026 |

| Tata Electronics–PSMC | Dholera, Gujarat | Logic Fab (50k wafers/month) | 91,000 | Site preparation | 2027–2029 |

| CG Power–Renesas–Stars | Sanand, Gujarat | OSAT (15M chips/day) | 7,600 | Pilot launched Aug 2025 | Commercial 2026 |

| Tata Semiconductor (TSAT) | Morigaon, Assam | OSAT (48M chips/day) | 27,000 | Under construction | Phase 1 Apr 2026 |

| Kaynes Semicon | Sanand, Gujarat | OSAT (6.33M chips/day) | 3,307 | Pilot operational | Ramping |

| HCL–Foxconn JV | Jewar, UP | OSAT (20k wafers/month) | 3,700 | Early stage | 2026–2027 |

| SicSem | Bhubaneswar, Odisha | Silicon Carbide Fab | 2,066 | Approved Aug 2025 | Post 2027 |

| 3D Glass Solutions | Bhubaneswar, Odisha | Advanced Packaging | 1,943 | Approved Aug 2025 | Post 2027 |

| Continental Device (CDIL) | Mohali, Punjab | OSAT | 117 | Approved Aug 2025 | 2026–2027 |

| ASIP Technologies | Andhra Pradesh | Advanced Packaging | 468 | Approved Aug 2025 | 2026–2027 |

The pattern is clear: multiple assembly and test facilities will commission in 2025 to 2026, creating near-term revenue opportunities. The large fabrication facility at Dholera carries a 2027 to 2029 timeline, making it a multi-year execution story with limited near-term financial impact.

Market Structure and Competitive Landscape: Implications for Listed Companies

1. Tata Electronics Limited (Unlisted, but ecosystem anchor)

Tata Electronics is building India's first major logic fabrication facility in partnership with Taiwan's Powerchip Semiconductor Manufacturing Corporation. The ₹91,000 crore investment targets 50,000 wafers per month at 28 to 65 nanometer nodes, serving automotive, industrial, and defense applications.

Risk factors: Multi-year construction delays are common in greenfield semiconductor facilities. Yield ramp challenges can extend breakeven by years. Competition from established foundries with depreciated assets makes mature node economics challenging.

2. MosChip Technologies Limited (NSE: MOSCHIP)

MosChip is one of India's few listed pure-play semiconductor design services companies. FY25 consolidated revenue stood at ₹466.84 crore, driven by application-specific integrated circuit design and silicon engineering services.

Recent traction: The company announced a partnership with C-DAC and Socionext to design a high-performance computing system-on-chip on TSMC's 5 nanometer process. This represents a material design engagement demonstrating capability at advanced nodes. Earlier disclosures show approximately ₹18 crore revenue from a successful tape-out, indicating project scale and monetization pathway.

Risk factors: Heavy dependence on global client relationships creates revenue concentration risk. Talent retention costs are rising as semiconductor hiring intensifies. MosChip does not publish a formal order book, limiting forward revenue visibility. Competition from larger global design services providers constrains margin expansion.

3. Kaynes Technology India Limited (NSE: KAYNES)

Kaynes operates at the intersection of electronics manufacturing services and semiconductor assembly through its Kaynes Semicon division. Q2 FY26 revenue reached ₹9,062 million with a strong order book of ₹80,994 million as of September 2025. The company has commissioned a pilot outsourced semiconductor assembly and test line in Sanand with investment of ₹3,307 crore, targeting a capacity of 6.33 million chips per day.

Recent traction: Kaynes positions itself across automotive, industrial including electric vehicles, aerospace, and strategic electronics, the verticals most semiconductor-adjacent. While the company does not break out a specific "semiconductor revenue" line, vertical exposure indicates substantial linkage. The order book provides 12 to 18 months revenue visibility.

Risk factors: Electronics manufacturing services faces intense competition and margin pressure. High working capital intensity limits return on capital employed. The company does not publish capacity utilization rates, making it difficult to assess operational efficiency. Dependence on automotive and defense procurement cycles creates revenue lumpiness.

4. Syrma SGS Technology Limited (NSE: SYRMA)

Syrma operates in precision electronics manufacturing with exposure to automotive, industrial, and high-reliability assemblies. Q2 FY26 revenue was ₹11,546 million with an order book of approximately ₹58 billion. The company has entered international partnerships including a joint venture with Italy's Elemaster for high-reliability electronics and is expanding printed circuit board and assembly capacity.

Recent traction: Syrma's revenue mix is weighted toward industrial and automotive segments, providing indirect semiconductor exposure through component assembly and system integration. The company does not operate a dedicated outsourced semiconductor assembly and test facility like CG Power or Kaynes, but serves as a downstream beneficiary of chip consumption growth.

Risk factors: Competitive electronics manufacturing services landscape limits pricing power. Technology complexity requires continuous capability investment. End-market cyclicality in automotive and industrial sectors creates demand volatility. Execution risk as company scales operations.

5. CG Power and Industrial Solutions (NSE: CGPOWER)

CG Power's semiconductor play comes through CG Semi, a joint venture with Renesas and Stars Microelectronics. The company launched an outsourced semiconductor assembly and test pilot facility in Sanand in August 2025, with planned investment of ₹7,600 crore and target capacity of 15 million chips per day. The facility serves automotive, defense, infrastructure, and internet of things end markets.

Recent traction: The pilot facility is operational and conducting customer qualification runs. Commercial production is targeted for calendar 2026. This makes CG Semi one of the earliest commercial outsourced semiconductor assembly and test players in India alongside Kaynes.

Risk factors: Early-stage operations face a learning curve and yield challenges. Indian outsourced semiconductor assembly and test facilities will initially run lower margins than established global peers like Amkor and Assembly Test Electronics due to ramp costs and scale limitations. Global outsourced semiconductor assembly and test companies report gross margins around 16% to 17% and operating margins in high single digits. Expect CG Semi to run 200 to 600 basis points lower initially, narrowing as volume scales.

Investment Landscape and Valuation Framework

The semiconductor value chain offers different risk-reward profiles at each stage. Design services companies like MosChip trade at high multiples reflecting growth potential but face execution risk and limited near-term scale. Electronics manufacturing services players like Kaynes and Syrma offer nearer-term revenue visibility through existing order books but operate in competitive, margin-pressured businesses.

Assembly and test operations represent a middle path with 18 to 24 month revenue timelines and better margin structure than generic electronics manufacturing services. However, early-stage Indian facilities will run below global peer margins initially. Investors should model 200 to 600 basis point margin discounts versus established players, narrowing over three to five years as scale and yield improve.

Fabrication facilities carry the longest gestation (four to five years) and highest capital intensity. Tata Electronics Dholera requires ₹91,000 crore investment with revenue unlikely before 2027 to 2029. Breakeven extends beyond 2030 under base case assumptions. This makes fabrication a structural, long-duration theme unsuitable for investors seeking near-term returns.

Valuation multiples: Listed semiconductor-adjacent companies trade at premium multiples reflecting growth expectations. Kaynes and Syrma command price-to-earnings ratios in the mid-30s to 40s range, pricing in order book conversion and capacity expansion. MosChip, with smaller scale and higher risk profile, sees more valuation volatility. Re-rating catalysts include execution milestones, customer additions, and margin stability.

Also Read: The AI Revolution and India’s Datacenter Opportunity

Challenges and Risk Factors

Execution risk dominates the near-term outlook. Semiconductor manufacturing requires precise integration of facility construction, clean room environments, equipment installation, process development, and yield optimization. Delays at any stage extend time to revenue. Tata Electronics faces a multi-year execution timeline with limited precedent for greenfield fabrication in India.

Talent constraints create bottlenecks. The industry needs 115,000 additional professionals by 2030 but faces unfilled positions of approximately 67,000 due to limited specialized training pipeline. This creates wage inflation and constrains how fast new facilities can ramp production. Companies are competing aggressively for experienced process engineers and equipment technicians.

Capital intensity limits near-term profitability. Fabrication facilities require ₹90,000 crore plus investment with extended payback periods. High fixed cost structure creates operating leverage eventually but limits profitability for years. Assembly operations require lower capital but face cyclical demand and competitive pricing pressure.

Technology obsolescence risk. India's fabrication strategy focuses on 28 to 65 nanometer mature nodes for automotive and industrial applications. These nodes face competition from established foundries with fully depreciated assets. Continuous technology upgrades require sustained capital investment to remain competitive.

Global cyclicality affects demand. The semiconductor industry experiences boom-bust cycles driven by inventory dynamics, end-market demand shifts, and capacity additions. India's facilities will face the same cyclical pressures as global peers, with limited ability to pass through cost increases during downturns.

Also Read: A Deep Dive into India’s Energy Markets

Future Outlook

India's semiconductor journey is progressing from policy intent to physical infrastructure. Multiple assembly and test facilities will be commissioned in 2025 to 2026, creating first tangible revenue opportunities for listed companies. The design services ecosystem is scaling with government support, though commercial revenue remains modest.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.