India’s datacenter industry stands at an important crossover point, transforming from a nascent market into a global powerhouse. With capacity tripling from 350 megawatts in 2019 to over 1,030 megawatts in 2024, and projected to reach 3,000-3,500 megawatts by 2030, India represents one of the world’s fastest-growing datacenter markets. This explosive growth which is driven by digital transformation, artificial intelligence adoption, regulatory mandates, and India’s emergence adoption, regulatory mandates, and India’s emergence as a global data hub positioning the country as a critical infrastructure player in the digital economy.

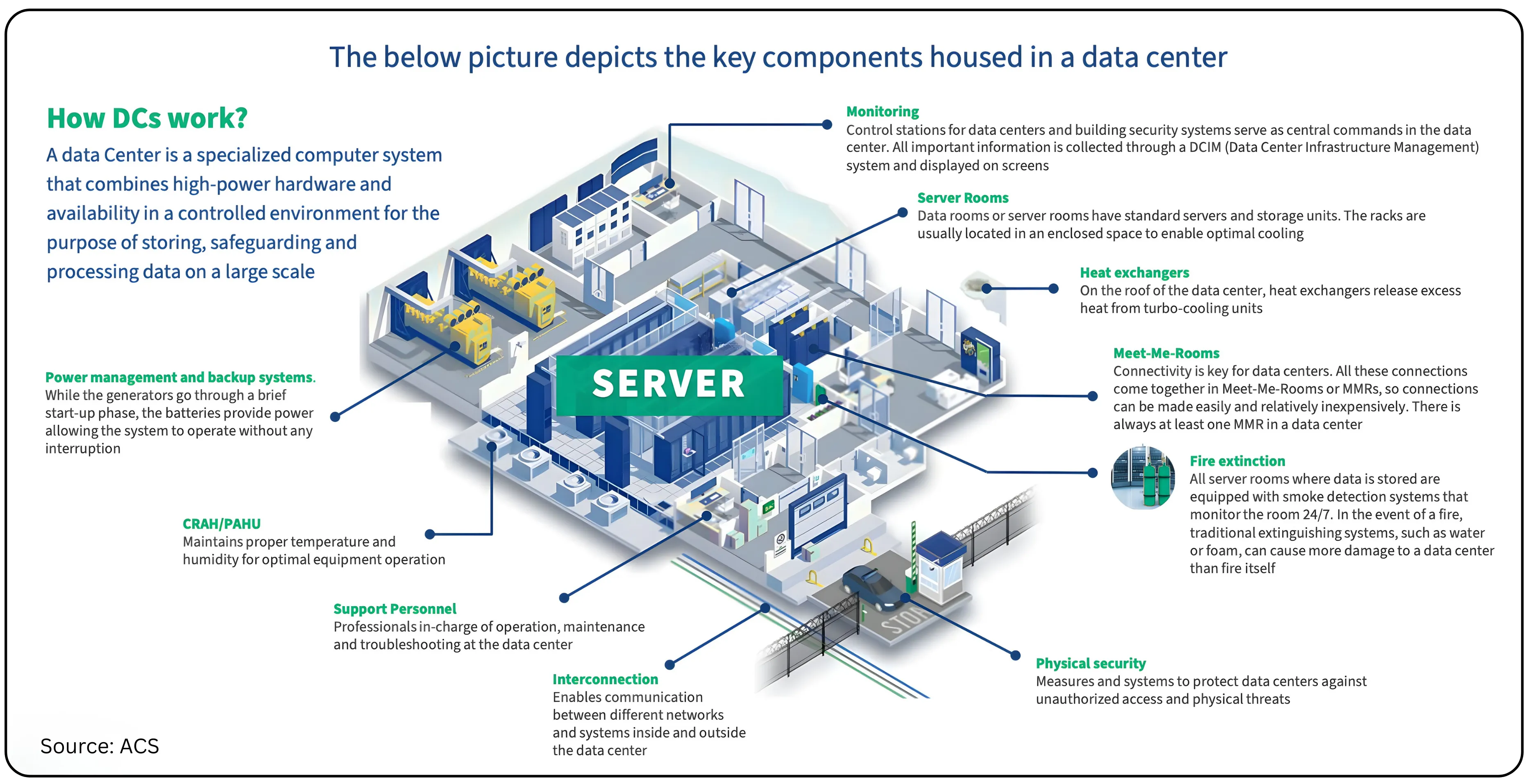

The picture below depicts the key components housed in a data center

Market Overview and Global Context

The global datacenter industry has evolved into a $347.6 billion market, projected to reach $652 billion by 2030 at an 11.2% compounded annual growth rate. Within this landscape, India currently holds just 3% of global operational datacenter capacity which is a stark contrast to its 20% share of worldwide data demand. This massive gap between data generation and local storage capacity represents both a challenge and an extraordinary opportunity.

While the United States leads with 15 gigawatts of capacity (48% of global share) and China follows with 9 gigawatts (23%), India's 1.03 gigawatts represents significant untapped potential. This disparity is particularly striking given India’s 836 million interest users and 550 million smartphone users; the numbers are expected to reach 982 million and 693 million respectively by 2030.

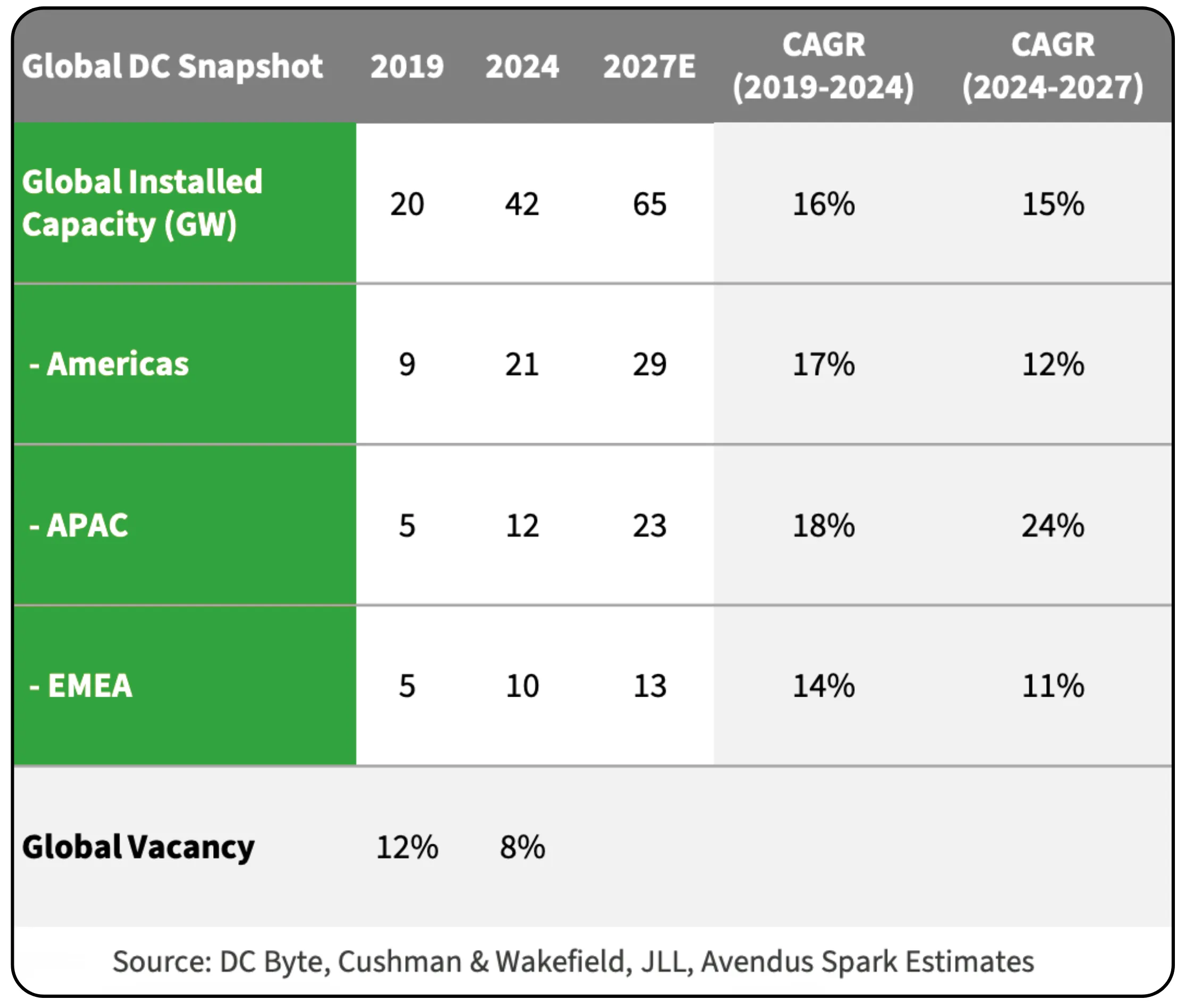

The global datacenter capacity across regions grew at 16% CAGR over the past five years, with Asia-Pacific (excluding India) growing fastest at 18%. India’s growth trajectory has been even more impressive at 24% CAGR since 2019, signaling the country’s rapid catch-up trajectory.

Also Read: The Business of Sustainability: Inside India’s Recycling Boom

###The AI revolution and Power Dynamics

Artificial Intelligence has fundamentally altered datacenter economics and infrastructure requirements. AI workloads consume 3-5 times more computing power than traditional applications, requiring 2-3 times more electrical capacity. Training GPT-3 consumed 1.29 gigawatt-hours of electricity: GPT-4 required over 50 gigawatt-hours, nearly 0.1% of New York City’s annual consumption.

Globally, datacenters consumed 415 terawatt-hours in 2024 (1.5% of global electricity demand), projected to exceed 945 terawatt-hours by 2030. Within this growth, AI datacenters will constitute 35% of capacity by 2030, up from 15% currently. In India specifically, AI datacenter capacity is expected to grow at 80% CAGR from from 2024 to 2027, reaching 619 megawatts from just 41 megawatts.

The power challenge has sparked a cooling revolution. Traditional air cooling reaches its limits as modern AI servers consume 40-100 kilowatts per rack versus 10-30 kilowatts for traditional servers. The liquid cooling market is exploding from $2.8 billion in 2024 to $13.1 billion by 2032, with companies like Microsoft achieving 15% energy efficiency improvements through two-phase immersion cooling.

Also Read : IEX, At the Heart of India’s Power Market Evolution

India’s structural advantages

India’s datacenter market growth is underpinned by several compelling structural advantages that position it uniquely among emerging markets.

Cost competitiveness

India offers among the world’s lowest datacenter construction costs at approximately $7 per watt, which is second only to China’s $6 per watt. This compares favorably to the United States ($13/watt), Japan ($21/watt), and the United Kingdom ($26/watt). Mumbai’s specific construction cost of $6.60 per watt makes it particularly attractive compared to Tokyo and Sydney.

Electricity costs further enhance India’s competitiveness at $0.13 per kilowatt-hour, approximately 20% lower than the United States ($0.16/kWh) and significantly below Japan ($0.21/kWh), Australia ($0.26/kWh), and the UK (0.45/kWh).

Massive Domestic Market

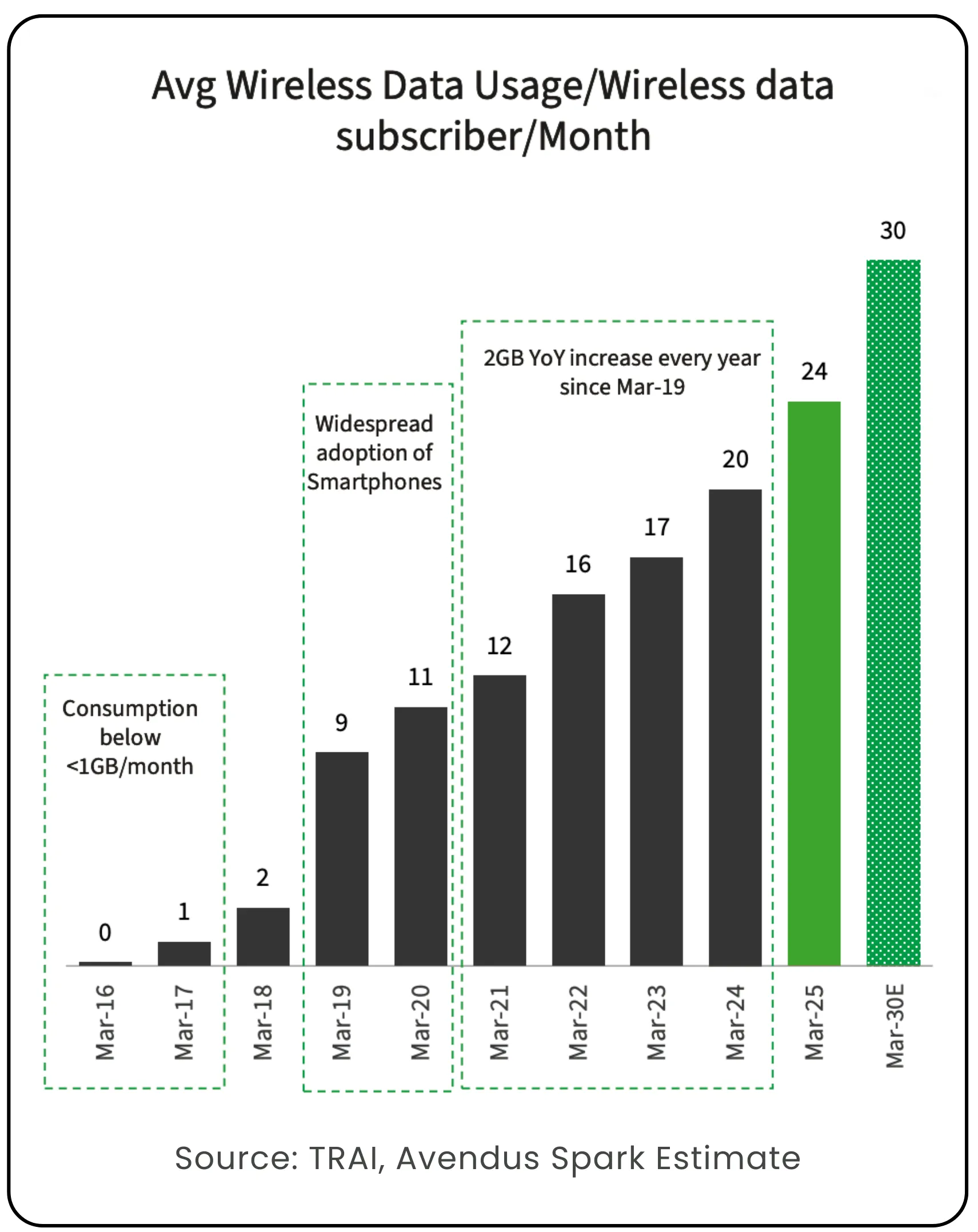

With 1.4 billion people and the world’s second-largest mobile user base, India generates enormous data processing requirements. Mobile data consumption has stabilized at 20-21% of global usage since 2020, with per-smartphone consumption expected to reach 30-35 gigabytes monthly by 2030 from current levels of 25-30 gigabytes.

India’s 5G penetration which is currently at 29%, is projected to reach 50% by 2030, driving data consumption growth at 9% CAGR. Video streaming, which accounts fro 74% of global mobile traffic, will continue expanding data requirements as content quality and consumption increase.

Cloud Adoption Acceleration

India’s public cloud industry is growing at 26% CAGR, from $2 billion in FY20 to a projected $22 billion by FY30. This significantly outpaces global cloud growth of 15% CAGR. Enterprise adoption of cloud services is shifting datacenter capacity from on-premise installations (60% in 2017) to hyperscale-leased colocation facilities (projected 40% by 2027).

Regulatory tailwinds and policy support

India’s regulatory framework has emerged as a powerful catalyst for domestic datacenter development, creating both mandate-driven demand and enabling infrastructure.

Data localisation mandates: The Digital Personal Data Protection Act (DPDPA) 2023, while not explicitly mandating localization, empowers the government to restrict cross-border data transfers to specific countries. This creates implicit incentives for domestic storage and processing.

More directly, the Reserve Bank of India’s 2018 directive required all payment data to be stored exclusively in India triggering immediate demand surges. Similarly, SEBI mandated that all regulated entities like stock exchanges, brokers, mutual funds, depositories, and KYC agencies, store and process data within India to ensure unrestricted regulatory access.

State-level incentives: Multiple states have implemented comprehensive datacenter policies offering substantial incentives:

Maharashtra (2021 Policy): 100% electricity duty exemption, dual power grid availability, 50% wheeling charge exemption, 100% stamp duty exemption, classified as essential services with special building norms, and residential property tax rates.

Tamil Nadu (2021 Policy): Lifetime electricity duty exemption, INR1/unit power subsidy for five years outside Zone I, open-access power, support for captive renewable energy, land at subsidized rates, and up to 50% building fee rebates.

Karnataka (2021 Policy): 25-50% land subsidy for first three datacenter parks, 100% stamp duty exemption on first land transaction (50% on second), 60% interest reimbursement, and 7% capital subsidy up to INR200 million.

Telangana (2016 Policy): Electricity at cost of generation, dual power grid, renewable energy under open access, subsidized fuel prices, and separate infrastructure category status.

Uttar Pradesh (2023 Policy): 100% electricity duty waiver, INR1/unit tariff subsidy in Zone II, lifetime electricity duty exemption, and relaxed Floor Space INdex regulations.

The Draft Data Center Policy 2020 and IndiaAI Mission (supported by INR219 billion MeitY budget targeting a $1 trillion AI economy by 2035) provide additional federal support.

Market structure and competitive landscape

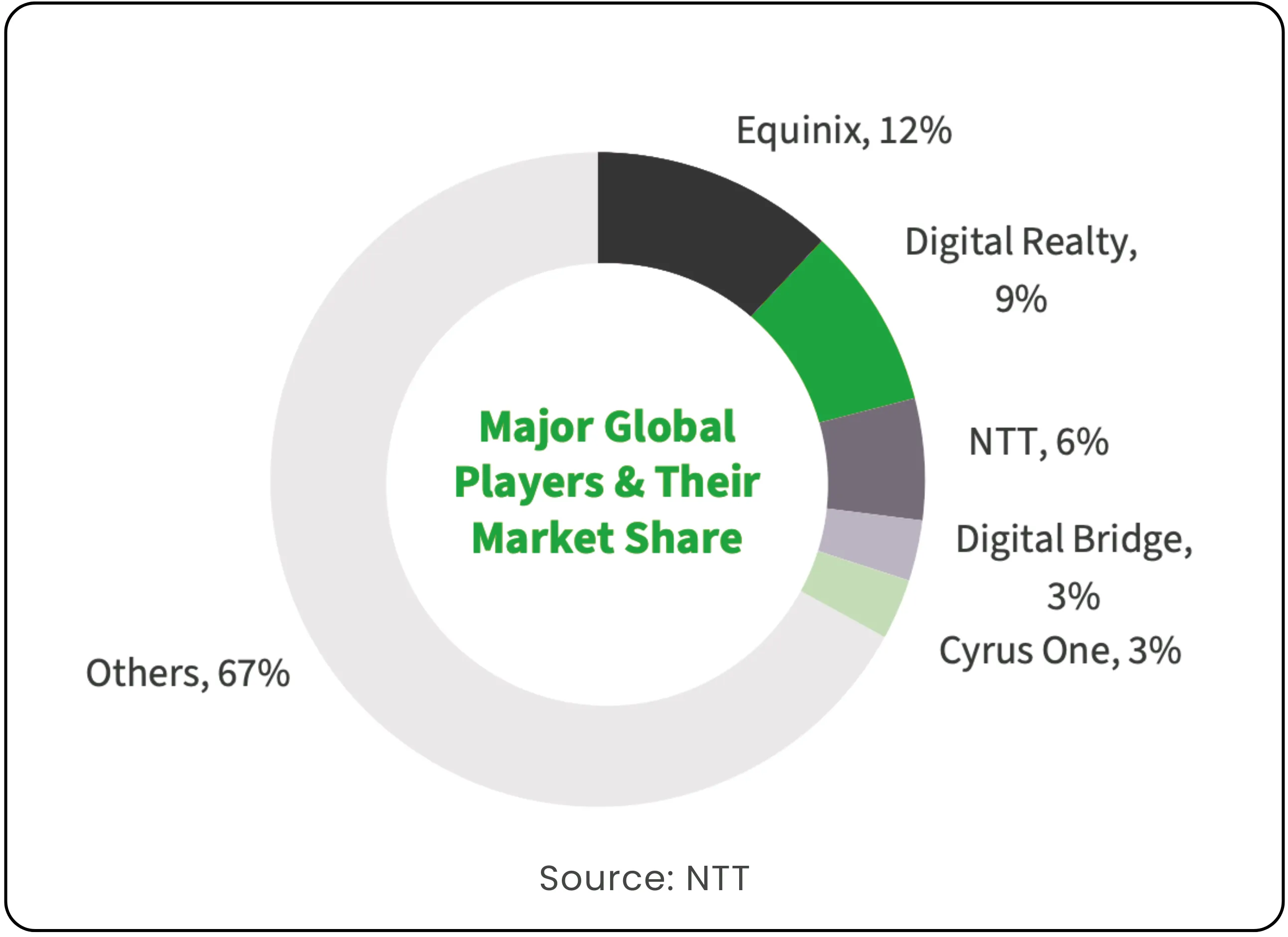

India’s datacenter market exhibits high concentration, with the top five players accounting for 75% of capacity. NTT and STT Global Data Centers together control approximately 50% of the market, followed by Sify Technologies (10%), CtrlS Data Centers (9%), and Nxtra Data Limited (9%).

NTT: Nippon Telegraph and Telephone Corporation

However, this concentration is expected to decline as new entrants establish capacity. By 2027, the top six players' combined share is projected to fall to 60% from 85% currently, as approximately 1,000-1,200 megawatts of new capacity comes online from new market participants.

Geographic distribution

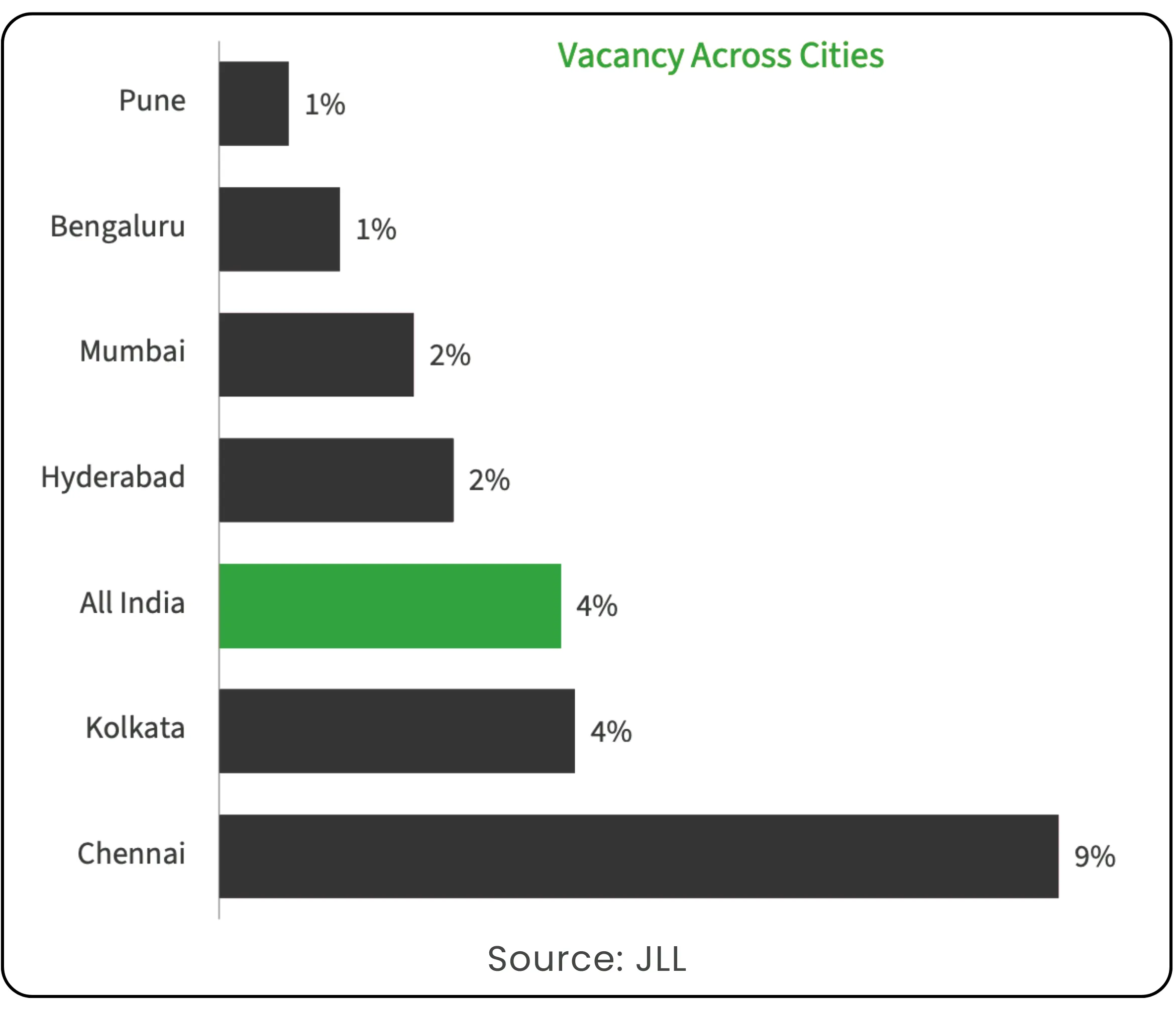

Mumbai and Chennai dominate India’s datacenter landscape, together accounting for 63% (563 MW and 113 MW respectively) of installed capacity. This concentration stems from submarine cable landing stations and reliable power availability. Delhi (114 MW, 11%), Pune (109 MW, 11%), Bengaluru (81 MW, 8%), and Hyderabad (55 MW, 5%) constitute secondary markets.

Notably, Chennai exhibits the highest vacancy rate at 9%, suggesting available capacity for immediate deployment. The market is experiencing geographic diversification with upcoming capacity additions shifting toward tier-2 cities, Mumbai and Chennai’s contribution to annual capacity additions is expected to decline from 65% in 2024 to 50% by 2027.

Large-scale datacenters (exceeding 20 megawatts) have grown from 42% of capacity in 2020 to 56% currently, reflecting economies of scale and hyperscaler preference for consolidated facilities.

Customer dynamics and business models

Hyperscalers including Amazon Web Services, Microsoft Azure, Google Cloud, and Meta account for 54% of India’s datacenter demand, up from 43% in 2021. This represents the most significant shift in customer composition. Banking, financial services, and insurance (BFSI) contribute 18%, technology companies 125, with the remaining 16% distributed across telecom (4%), entertainment and media (2%), healthcare (1%), and energy (1%).

The number of players in hyperscaler datacenter development has tripled from five in 2019 to fifteen in 2024. Hyperscaler colocation capacity has quadrupled over this period, with 54% of colocation capacity now leased to hyperscalers. For upcoming supply through 2027, approximately 50-60% (600-700MW of 1,000-1,200MW total) is already pre-committed or leased by hyperscalers, demonstrating strong demand visibility.

Revenue models and economics

India’s datacenter industry operates across four primary business models:

Colocation (wholesale and retail): Enterprises and hyperscalers rent rack space, power, and cooling. Wholesale contracts (>250KW-1MW) typically span 5-10 years, while retail arrangements (small to mid-size business) run 3-5 years at approximately INR7,500 per kilowatt monthly.

Cloud Infrastructure (IaaS): Providers offer virtualized computing resources where virtual machines, storage, and networking using flexible subscription or pay-as-you-go pricing. This capital-intensive model generates 5-6x colocation revenues but requires significantly higher investment.

Managed Services (PaaS): Outsourced IT operations and support layered on core infrastructure, offering monitoring, backup, security, and compliance services on subscription or annual maintenance contract basis.

Edge Datacenters: Small-scale facilities (100KW-2MW) located closer to end users in metro cities and tier-2/3 regions for latency-sensitive workloads like content delivery, gaming, and 5G applications

To understand these revenue models in more detail read: The Datacenter Boom Fueling the AI Revolution

Financial Metrics: Colocation operations exhibit 60-70% EBITDA margins (excluding electricity pass-through), generating stable yields of 10-12% on invested capital with 10-12 year payback periods. Required capex approximates INR500-600 million per megawatt.

Cloud infrastructure operations achieve 40-50% EBITDA margins but require INR800 million - 1 billion per megawatt investment. However, pre-tax yields reach 29%, versus 12% for colocation, with return on equity approaching 20% versus 3% for colocation at project maturity, offering payback periods of 4-5 years.

Investment landscape and valuation framework

The Indian datacenter investment landscape has entered an unprecedented expansion phase, characterized by massive capital commitments from both domestic conglomerates and global technology giants.

Major Strategic investments and partnerships: TCS’s $6.5 Billion AI Data Centre Initiative: In Q2 FY26, Tata Consultancy Services announced the largest single datacenter commitment by an Indian IT services firm pledging a $6.5 billion investment to build 1 gigawatt of AI and sovereign datacenter capacity. This transformative project includes 15 centers in India and 14 globally, targeting 10x growth over India’s current 1.2 gigawatt capacity within five years. TCS’s 40% of new hires are focused on AI and data science, positioning TCS as the world’s largest AI-led tech services firm.

Airtel-Google-Adani $15 Billion AI Hub: Bharti Airtel Adani Connex, and Google are jointly developing India’s largest AI hub in Visakhapatnam with $15 billion investment. The facility will feature a renewable energy-powered datacenter and undersea cable network, positioning India as a global AI infrastructure hub while enhancing Google’s Vertex AI services for Indian enterprises.

Tata Communications-AWS Strategic Network: Tata Communications’ stock surged 15% following announcement of its AI-driven synergy with AWS, launching one of India’s most advanced long-distance networks connecting AWS regions in Mumbai, Hyderabad, and Chennai. This network supports high-throughput, low-latency AI, 5G, and high-performance computing workloads, representing Tata’s largest national infrastructure project.

Also Read:Tata Communications ambitious digital transformation story

Jio-Anthropic AI Partnership: Reliance Jio is exploring a strategic partnership with

Anthropic to bring Claude AI models to India, addressing data residency requirements for Indian enterprises. Anthropic plans its first India office in Bengaluru, aiming to co-develop AI solutions across Jio’s telecom, retail, and energy verticals. While enterprises can currently access Claude via AWS Bedrock and Google Cloud, local residency would ensure regulatory compliance and lower latency.

These announcements collectively represent over $23 billion in new commitments, complementing the existing INR2.13 trillion ($25 billion) pipeline from traditional datacenter players including AdaniConneX, Yotta Infrastructure, and CapitaLand projected by 2030.

Valuation Framework Global datacenter companies trade at 20-22x EV/EBITDA on a one-year forward basis. Equinix, the world’s largest datacenter company, trades at 20x forward EV/EBITDA, while Digital Realty trades at 22x. Singapore-listed Keppel DC REIT trades at 22x, while Australia’s Next DC commands premium valuations of 52x due to regional scarcity and growth prospects.

Regional players show varying valuations: GDS Holdings (China, Hong Kong, Singapore, Southeast Asia presence) trades at 13-15x forward EV/EBITDA, below global peers despite historical alignment.

The recent surge in Indian datacenter-related stocks, Tata Communications’ 15% jump and sustained investor interest in TCS following its datacenter announcement- suggests the Indian market may command premium valuations due to high growth trajectory, regulatory tailwinds, and strategic positioning in the global AI infrastructure landscape.

Challenges and Risk Factors

The industry faces several structural challenges. High capital intensity with $430 billion projected global capex in 2025 creates significant upfront investment requirements against slower revenue realization. Rapid technological depreciation cycles (building:30 years, infrastructure: 10 years, GPUs: 3-5 years) generate approximately $40 billion annual depreciation against $15-20 billion revenue globally.

Technological obsolescence risk, power grid constraints in prime locations, regulatory uncertainty, and talent shortages for specialized operations present ongoing challenges. Some analysts warn of bubble-like behavior with overbuilding driven enthusiasm, drawing parallels to past telecommunications infrastructure booms.

Future Outlook

India’s datacenter industry stands at the threshold of transformative growth. The convergence of data localization mandates. AI adoption, cloud migration, and cost advantages creates a compelling multi-decade growth trajectory. As India’s share of global datacenter capacity expands from 3% toward more proportional representation relative to its data generations, the sector offers sustained investment opportunities across colocation, cloud infrastructure, managed services, and edge computing segments.

The companies and infrastructure providers that build the most efficient, sustainable, strategically located, and technologically advanced datacenter capacity will capture disproportionate value as India solidifies its position as a global digital infrastructure hub.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.