Sharvaya Metals Limited is an Ahmednagar-based aluminium manufacturer engaged in producing and supplying a wide variety of aluminium products. The company has built expertise in producing aluminium alloyed ingots, billets, slabs, sheets, and circles. With its manufacturing unit located at 59, Nagar Kalyan Road, Bhalawani, Tal Parner, Ahmednagar, Maharashtra, Sharvaya Metals is strategically placed to cater to both domestic and international customers.

The company supplies to consumer appliances manufacturers, cookware brands, and automotive players, while also expanding its reach to electric vehicle (EV) component suppliers by producing battery housings and aluminium casings for battery cells.

The IPO proceeds will enable Sharvaya Metals to increase capital expenditure, strengthen working capital, and expand its production capacity to serve domestic and global demand.

Core business and verticals

Sharvaya Metals operates across multiple verticals of the aluminium value chain, focusing on:

- Aluminium Alloy Ingots: Supplied to industries like automotive and heavy machinery.

- Aluminium Billets: Used in extrusion processes for architectural and industrial applications.

- Aluminium Slabs and Sheets: Key raw materials for cookware, consumer appliances, and industrial parts.

- Aluminium Circles: Supplied to cookware manufacturers and appliance companies.

- Specialized Aluminium Products for EVs: Battery housings, aluminium casings for battery cells, and lightweight structures for the EV ecosystem.

This extensive product range gives the company resilience against demand fluctuations in any single sector and positions it strongly in both traditional and emerging markets.

Also read : Amanta healthcare IPO OVERVIEW

IPO details

| Particulars | Details |

|---|---|

| IPO Type | SME IPO (BSE SME platform) |

| Face Value | ₹10 per equity share |

| Issue Price / Price Band | To be announced (expected premium over face value) |

| IPO Size | Equity shares aggregating up to 30,00,000 shares (aggregating up to ₹58.80 Cr) comprising Fresh Issue and Offer for Sale (OFS) |

| Fresh Issue | Net proceeds to be used for: • Capital expenditure (expansion & modernization) • Working capital requirements • General corporate purposes |

| Offer for Sale (OFS) | Promoter selling shareholders offloading a portion of holdings |

| Market Maker Reservation Portion | Reserved to ensure liquidity; smaller-than-average market maker reservation |

| Minimum Bid Lot | As prescribed for SME IPO investors |

| Net Offer Allocation | • Retail Investors • Non-Institutional Investors (NII) |

| Registrar | Bigshare Services Pvt Ltd |

| Demat Requirement | Mandatory for all IPO applicants |

Financial performance

| Particulars | FY22 | FY23 | FY24 |

|---|---|---|---|

| Revenue from Operations | ₹40.80 | ₹70.15 | ₹71.45 |

| Total Income | ₹40.95 | ₹70.53 | ₹71.58 |

| EBITDA | ₹1.79 | ₹3.31 | ₹3.49 |

| EBITDA Margin (%) | 4.39% | 4.72% | 4.88% |

| Profit Before Tax (PBT) | ₹0.49 | ₹2.41 | ₹2.30 |

| Profit After Tax (PAT) | ₹0.40 | ₹1.95 | ₹1.80 |

| PAT Margin (%) | 0.97% | 2.78% | 2.52% |

| Net Worth | ₹4.14 | ₹6.09 | ₹7.90 |

| Debt-to-Equity Ratio | 4.31 | 2.45 | 1.71 |

| Return on Net Worth (RONW) | 9.54% | 32.00% | 22.83% |

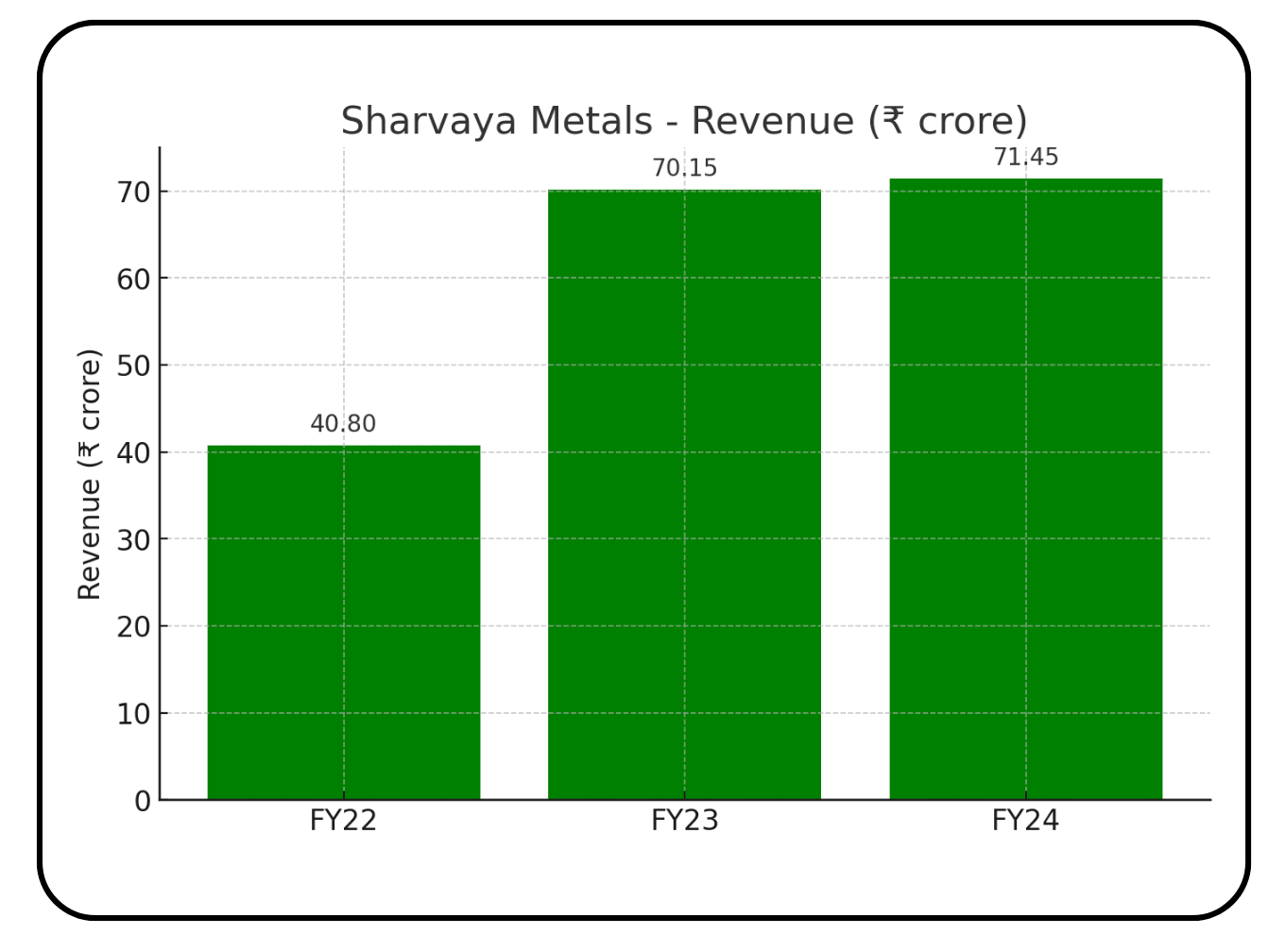

Revenue

Sharvaya Metals grew its revenue from ₹40.80 crore in FY22 to ₹71.45 crore in FY24, reflecting a healthy CAGR of ~20%. This steady top-line growth shows strong demand from domestic and international aluminium customers.

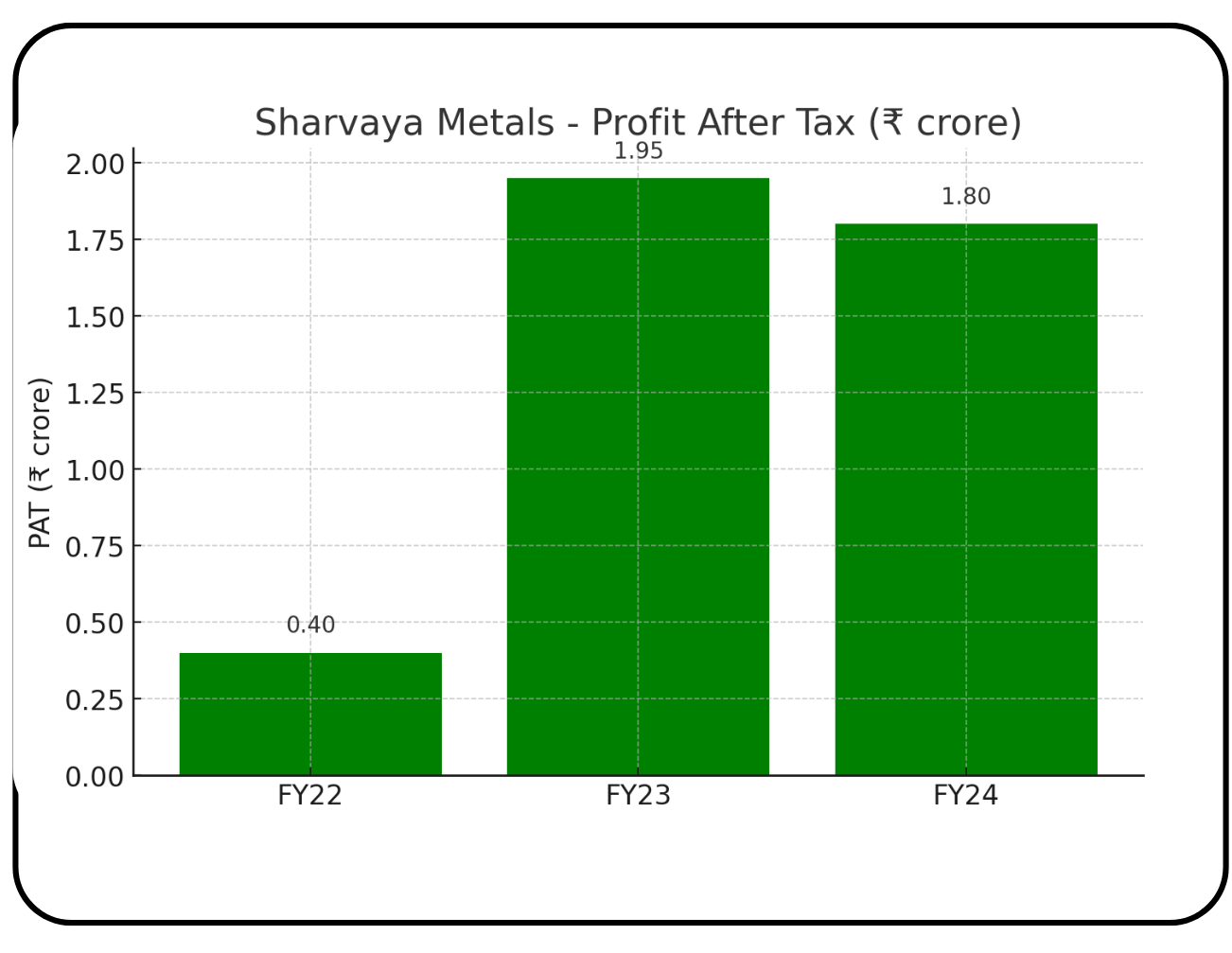

PAT (Profit After Tax)

Profitability improved from ₹0.40 crore in FY22 to ₹1.95 crore in FY23, before stabilizing at ₹1.80 crore in FY24. The company has managed to sustain profits despite operating in a highly competitive commodity space.

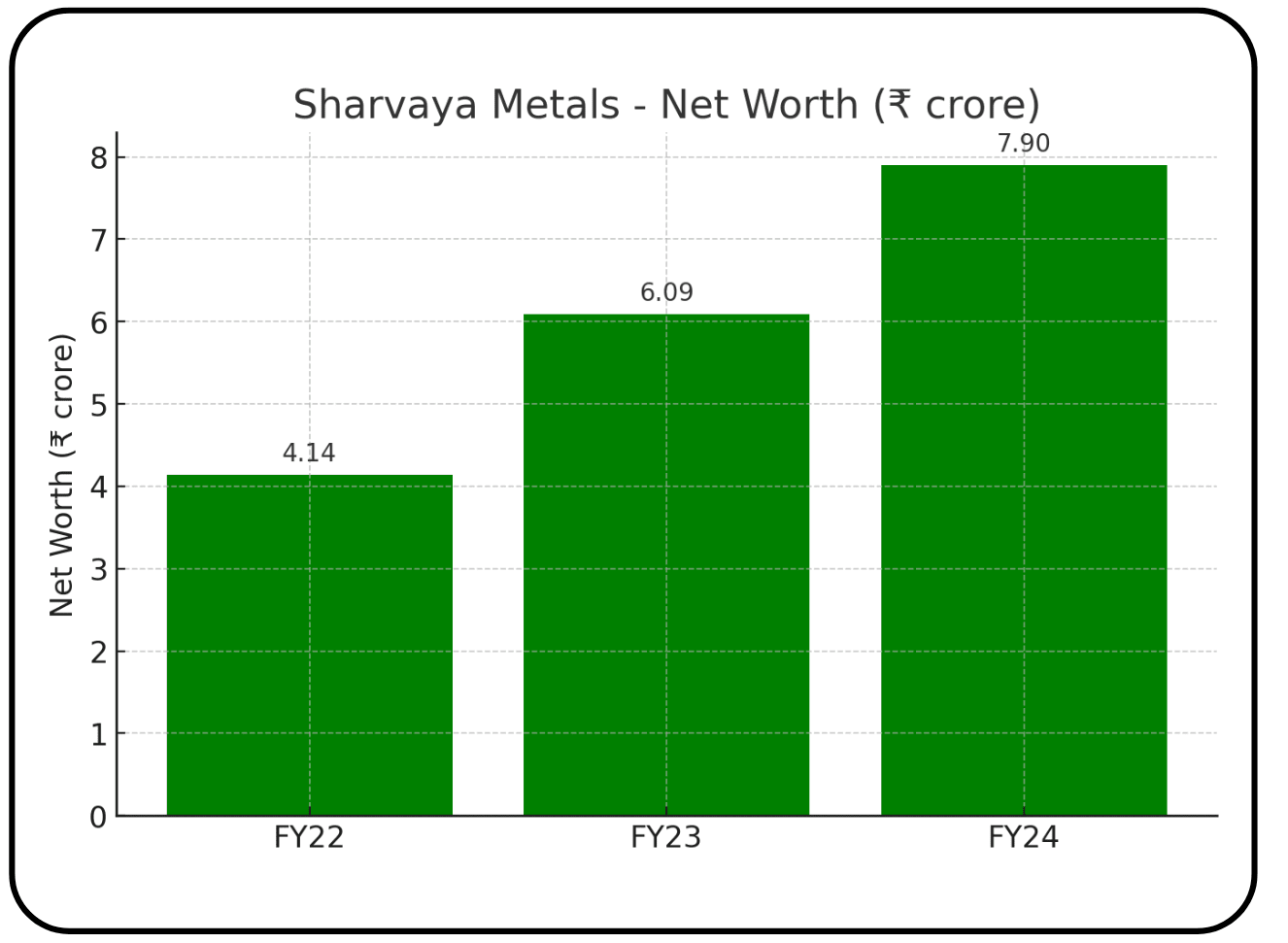

Net Worth

Net worth strengthened from ₹4.14 crore in FY22 to ₹7.90 crore in FY24, supported by internal accruals. This indicates better capital strength and reduced dependence on debt.

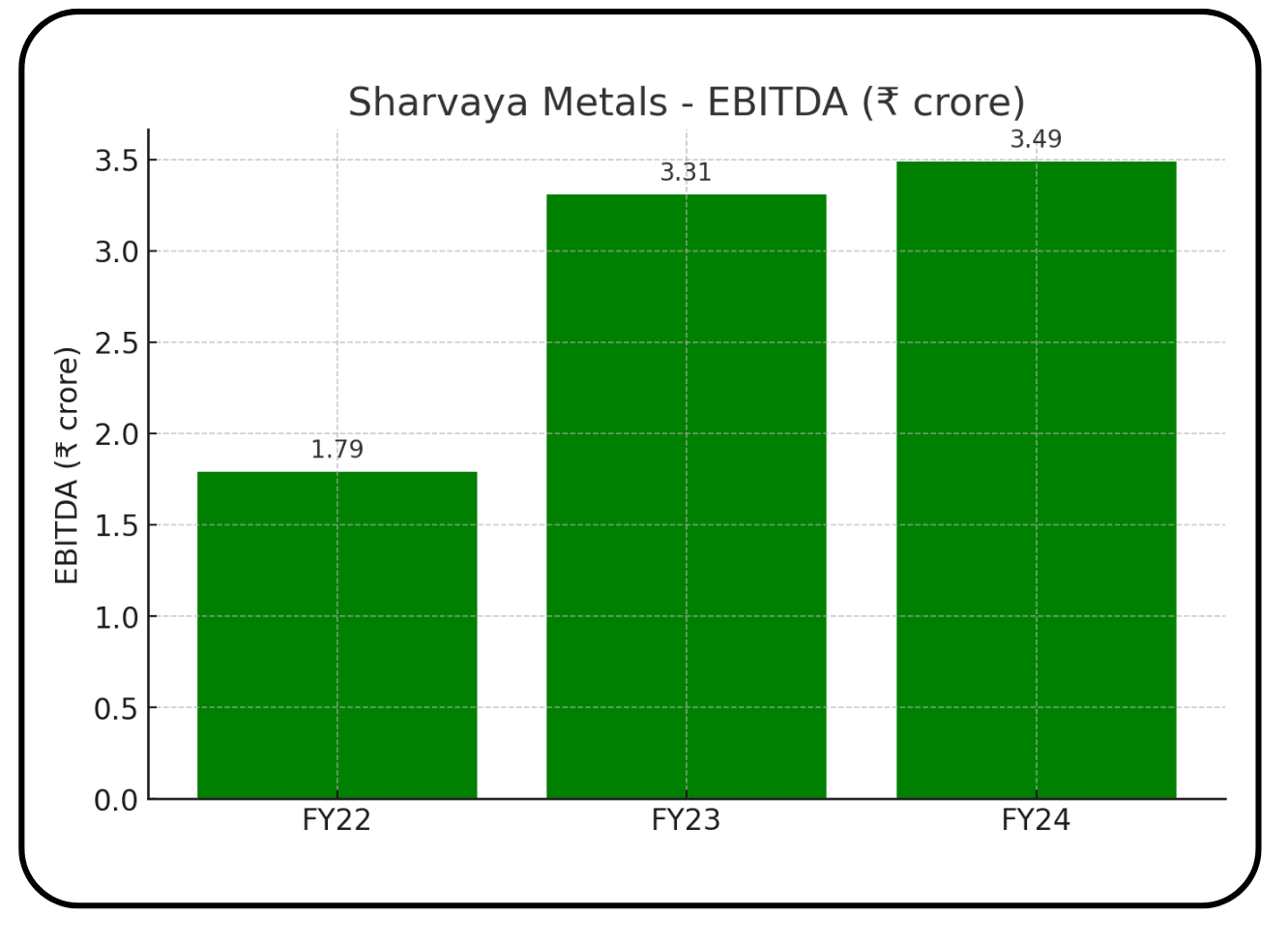

EBITDA

Operating profit rose from ₹1.79 crore in FY22 to ₹3.49 crore in FY24, showing consistent efficiency improvements. Margins remain modest but demonstrate the company’s ability to maintain stability in input cost cycles.

Also read : Lifestyle Inflation, the Hidden Cost of a Pay Raise

Peer comparison

| Company | Revenue | PAT | Net Worth | EPS (₹) | RONW (%) | Industry Segment |

|---|---|---|---|---|---|---|

| Sharvaya Metals Ltd | ₹71.45 | ₹1.80 | ₹7.90 | 2.49 | 22.83% | Aluminium alloys, billets, sheets, circles |

| Maithan Alloys Ltd | ₹3,094.00 | ₹268.00 | ₹1,804.00 | 88.90 | 14.8% | Ferro alloys (larger scale) |

| Gravita India Ltd | ₹2,834.00 | ₹208.00 | ₹946.00 | 29.70 | 22.0% | Lead, aluminium recycling |

| Arfin India Ltd (SME listed) | ₹1,132.00 | ₹21.00 | ₹205.00 | 4.80 | 10.2% | Aluminium wire rods, conductors |

| Shyam Metallics Ltd | ₹14,322.00 | ₹1,051.00 | ₹6,947.00 | 43.80 | 15.1% | Ferro alloys, aluminium flat products |

.webp?alt=media&token=271b2ffe-37ff-4a12-8ace-f9fd1a1a0ad6)

Sharvaya Metals: With revenue of ₹71.45 crore and PAT of ₹1.80 crore, the company is significantly smaller in scale but shows competitive return ratios. Its exposure to EV battery housings gives it a unique growth edge.

Maithan Alloys: A large ferro-alloy producer with ₹3,094 crore revenue and ₹268 crore PAT, it enjoys economies of scale. However, its size makes its growth rate slower compared to a nimble SME like Sharvaya.

Gravita India: Posted ₹2,834 crore revenue and ₹208 crore PAT, backed by aluminium and lead recycling. It shows strong margins comparable to Sharvaya, but at a much larger operational scale.

Arfin India (SME peer): With ₹1,132 crore revenue and ₹21 crore PAT, it is closer in scale to Sharvaya but still much larger. It focuses on aluminium wire rods, whereas Sharvaya has a broader product basket.

Shyam Metalics: A giant with ₹14,322 crore revenue and ₹1,051 crore PAT, it dwarfs SME peers. Sharvaya cannot match its scale but differentiates by focusing on specialized aluminium alloys for EV and appliances. Also read : Setting Rules for Financial Influencers and Why They Matter

Risks

- Commodity Price Volatility: Aluminium price fluctuations directly affect margins.

- Market Liquidity: As an SME IPO, trading volumes post-listing may remain limited despite market maker reservation.

- Sector Cyclicality: Dependence on demand from automotive and consumer appliances can be cyclical.

- Competition: Larger aluminium producers with economies of scale may undercut SME players.

- Export Risk: A slowdown in international customers could impact overall revenue.

Strengths

- Extensive product range across billets, ingots, slabs, circles, and sheets.

- Strategically located manufacturing unit in Ahmednagar, Maharashtra, near industrial hubs.

- Diversified customer base across domestic and international markets.

- Strong presence in the emerging EV ecosystem via aluminium battery housings.

- Capital expenditure and modernization plans funded by IPO proceeds.

- Experienced promoters with deep industry knowledge.

Conclusion

The Sharvaya Metals IPO provides an opportunity to invest in a growing SME company well-positioned in the aluminium value chain. Its product diversification, focus on consumer appliances and EVs, and expansion-driven IPO proceeds make it attractive for investors looking at long-term growth in the metals sector.

However, investors must weigh the risks of commodity volatility, SME market liquidity, and sector cyclicality before subscribing. The net offer, comprising both retail and NII categories, ensures wider participation.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.

%252FAnalysis%2520of%2520FII%2520Positioning%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D1405f6f4-6738-4f13-99c7-288e6fede0b6&w=3840&q=75)

%2520Every%2520Trader%2520Should%2520Know%252FCAS%2520Blog%2520Thumbnail.webp%3Falt%3Dmedia%26token%3D397e2566-b93f-4420-b41d-378b1483f837&w=3840&q=75)