Part 1 focused on the structure and deployment of the Cash Secured Put strategy, including strike selection, implied volatility, payoff structure, and execution using NxtOption. Part 2 continues from that foundation and focuses on what happens after the trade is active. Position management, assignment handling, and covered call writing play a significant role in determining the long-term effectiveness of the strategy.

Managing a Position Before Expiry

Once a Cash Secured Put is active, the position does not necessarily require constant adjustment. Many traders allow theta decay, which refers to the gradual erosion of option premium over time, to work in their favour while monitoring price movement and implied volatility.

If the stock remains comfortably above the strike price, the position may simply be held toward expiry or closed early once a substantial portion of the premium has decayed.

Some traders prefer exiting positions after capturing 50–70% of the maximum premium rather than waiting for the final days before expiry. This reduces exposure to sudden volatility spikes while freeing capital for new opportunities.

When the Stock Approaches the Strike

Position management becomes more important when the underlying stock starts approaching the selected strike price.

At this stage, the trader generally has three possible choices:

| Situation | Common Response |

|---|---|

| Stock remains fundamentally strong | Continue holding the position |

| Stock weakens moderately | Roll the position to a later expiry |

| Stock thesis changes materially | Exit the trade |

The correct response depends less on short-term price fluctuations and more on whether the trader still wants to own the underlying stock at the selected price.

Also read: How to Read OI Profile on NxtOption

Understanding Rolling

Rolling refers to closing the current option contract and simultaneously initiating a new contract with a later expiry.

The purpose of rolling is not to avoid losses entirely. Instead, it allows the trader to extend trade duration, collect additional premium, improve breakeven levels, and provide more time for the stock to stabilise.

For example, if a put option is nearing expiry while the stock trades close to the strike price, the trader may buy back the existing contract and sell another put in the following monthly expiry cycle.

This process allows additional premium collection while maintaining the broader CSP framework.

Rolling works best when the underlying stock remains fundamentally intact, implied volatility is still elevated, and the trader is comfortable extending the holding period.

Assignment in Indian Markets

Indian stock options are physically settled. If the put option expires in the money, the trader receives delivery of shares at the strike price.

Within a Cash Secured Put framework, assignment is not automatically a negative outcome. The shares are acquired at an adjusted cost basis after accounting for the premium collected during the trade.

For example, if a trader sells a ₹1,500 put option and collects ₹40 in premium, the effective acquisition cost becomes ₹1,460 if assignment occurs.

This adjusted cost basis becomes important for future position management.

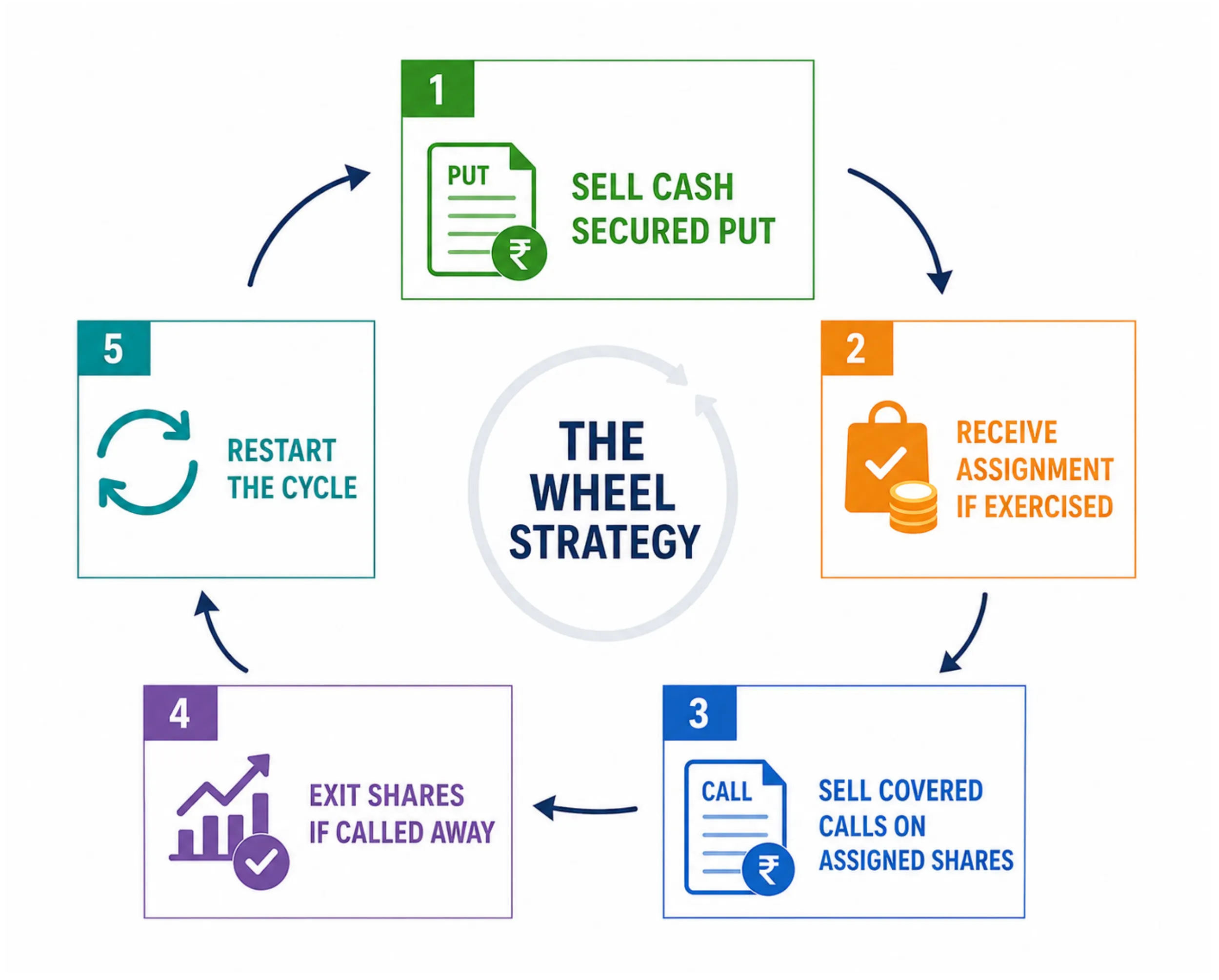

Transitioning Into the Wheel Strategy

Many traders continue the process after assignment through covered call writing, commonly referred to as the Wheel strategy.

Once shares are assigned, call options are sold against the stock position to generate additional premium income.

The objective shifts from acquiring shares through put selling to generating additional yield from owned shares.

The structure typically follows a cyclical process:

- Sell Cash Secured Put

- Receive assignment if exercised

- Sell Covered Calls on assigned shares

- Exit shares if called away

- Restart the cycle

Covered Call Strike Selection

Strike selection remains important even after assignment.

Many traders avoid selling covered calls below their adjusted acquisition cost because doing so can lock in realised losses if the shares are called away.

For example, if the effective acquisition cost is ₹1,460 and a covered call is sold at ₹1,420, assignment would result in the shares being exited below the effective purchase cost.

Because of this, covered call strikes are often selected above the adjusted cost basis, near resistance zones, or at levels where the trader is comfortable exiting the stock.

Also read: Trading Volatility Across Time with Calendar Spreads Part 2/2

Volatility and Position Management

Implied volatility continues to influence management decisions after entry.

Implied volatility continues to influence management decisions after entry.

Higher implied volatility generally benefits option sellers because premiums remain elevated, rolling opportunities improve, and covered call premiums become richer.

However, elevated volatility also reflects increased uncertainty in the underlying stock. Position sizing therefore remains important throughout the process.

The analytics tools in NxtOption can help traders evaluate implied volatility, option Greeks, premium changes, and expiry structures during both CSP and covered call phases.

Position Sizing and Capital Allocation

One of the most common mistakes in options selling is excessive concentration.

Even though Cash Secured Puts are comparatively conservative relative to naked leveraged option selling, they still carry substantial downside exposure if the underlying stock declines sharply.

Many traders therefore prefer diversified exposure across multiple stocks, limited allocation per position, and avoiding excessive exposure to a single sector.

Large-cap stocks with stable liquidity and consistent option activity generally remain more suitable for this framework than highly volatile low-liquidity counters.

Earnings Events and Gap Risk

Earnings announcements can significantly alter the behaviour of option positions.

Before earnings, implied volatility often expands, premiums become richer, and option selling may appear more attractive.

However, large overnight price gaps can exceed the premium collected from the trade.

For this reason, many CSP traders avoid initiating new positions immediately before earnings unless the elevated risk is fully understood and intentionally accepted.

Final Observation

The Cash Secured Put strategy is often viewed as a method of premium collection, but over longer periods it functions more as a structured stock acquisition and position management framework.

The effectiveness of the strategy depends less on predicting short-term market direction and more on disciplined strike selection, controlled position sizing, volatility awareness, and consistent management after entry.

Used selectively on liquid large-cap stocks, the combination of Cash Secured Puts and covered calls can provide a systematic approach to both stock ownership and premium generation across different market conditions.

The strategy rewards patience, disciplined capital allocation, and consistency more than aggressive directional prediction.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.