There is a pattern that repeats itself in financial markets with remarkable consistency, one that has played out through every major bull run, every crash, and every slow grind of recovery. And yet, each time it arrives, most participants respond as if it has never happened before.

This piece explores that pattern: why markets move the way they do, who tends to benefit, and what retail investors can learn from decades of market behaviour.

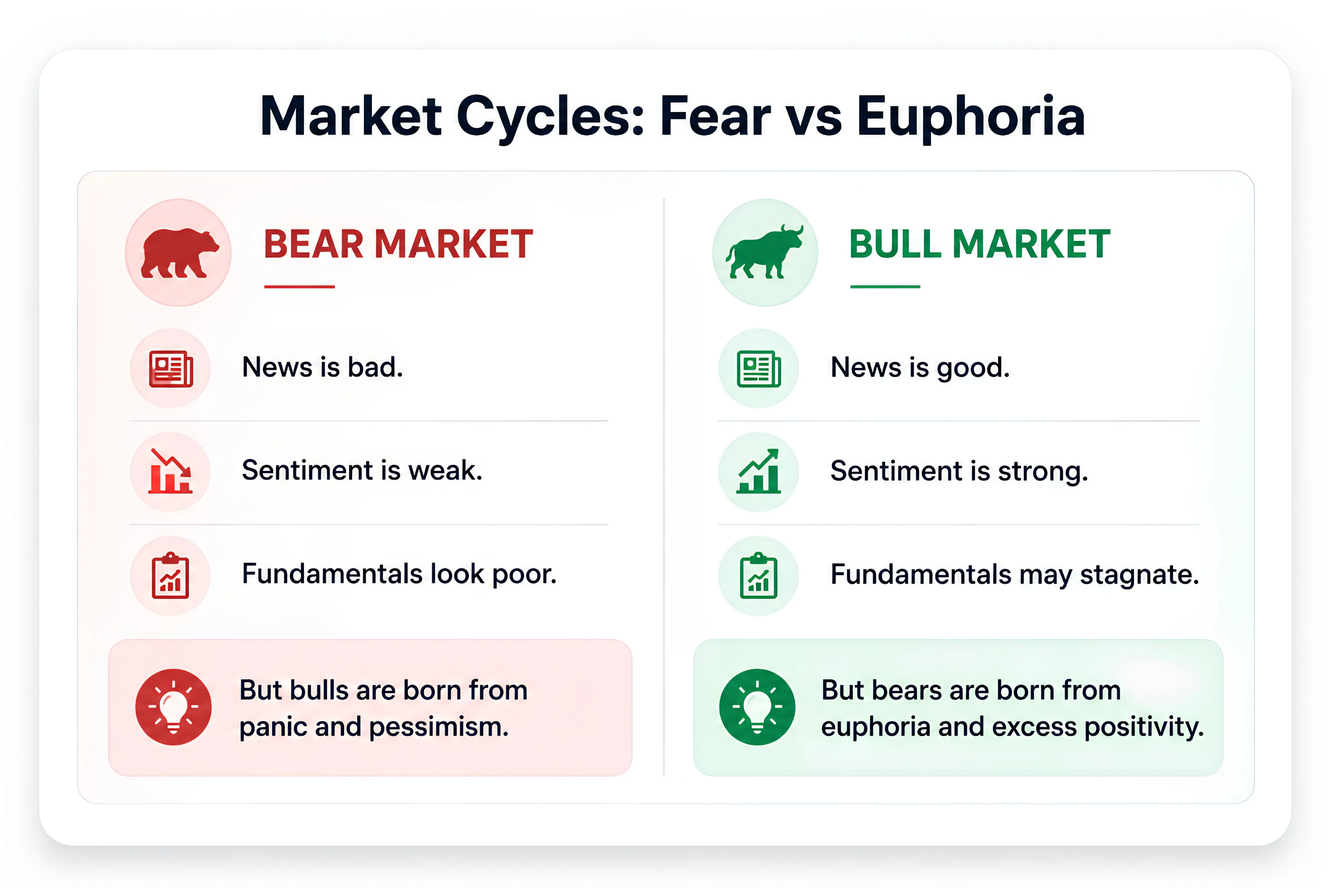

Bull Markets Are Born in Pessimism. Bear Markets in Euphoria.

It sounds counterintuitive, but market history bears it out. In a bear market, news is bad, sentiment is weak, and fundamentals look fragile. The headlines reinforce the fear. And yet, bull markets are born precisely out of this pessimism and panic.

Conversely, when a bull market matures, news is good, sentiment is buoyant, and optimism is widespread. But it is often during this very period of collective confidence that the seeds of the next bear market are sown.

The logic is simple. When everyone is already optimistic and invested, there is little buying power left to push prices higher. When everyone has already sold in fear, there is little selling pressure left to push prices lower.

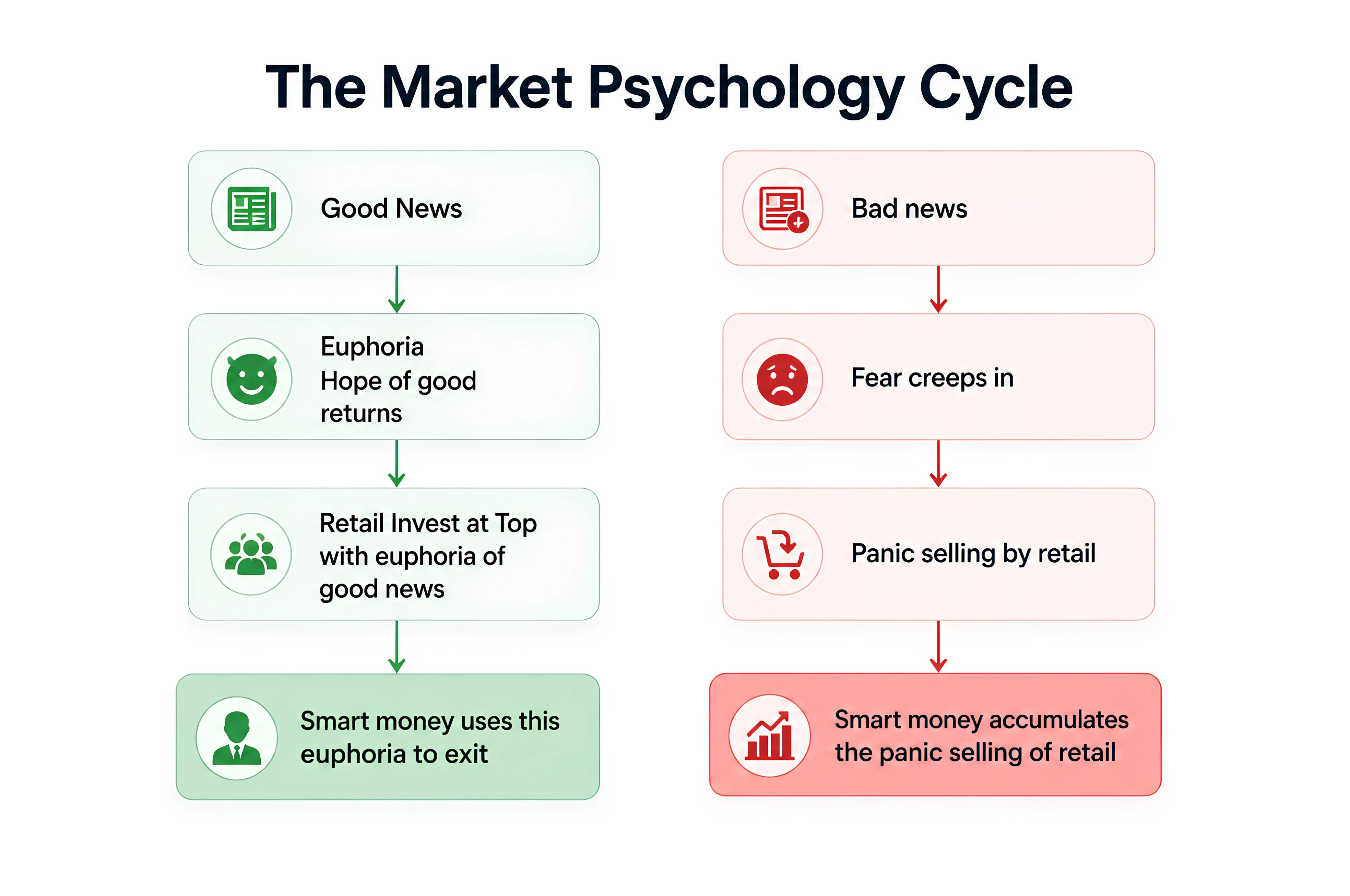

Retail and Smart Money

One of the most documented patterns in market behaviour involves the divergence between retail participation and institutional or experienced investors.

During good news cycles, euphoria builds. Hope of strong returns draws retail investors in, often near market tops. This is precisely when informed, patient investors, often referred to as ‘smart money,’ begin to exit positions into that buying pressure.

During bad news cycles, fear takes hold. Panic selling by retail participants creates an exit at precisely the wrong moment. This selling is quietly absorbed by the same patient capital that was distributing at the top.

This is not a conspiracy. It is the natural outcome of two different relationships with information, emotion, and time horizon.

Are We News Creators or News Consumers?

A useful question to ask: does the market react to news, or does it discount news before it is even published?

More often than not, the evidence suggests the latter. The market tends to price in outcomes, positive or negative, before those outcomes become headlines. By the time retail investors read the news and act on it, the market has already moved.

As one way to think about it: the market has a kind of perverse logic, it rises when you expect it to fall, falls when you expect it to rise, and very often, the move happens for reasons that never make it into any headline.

This does not mean news is irrelevant. It means that acting on news as the primary signal, rather than on price and volume behaviour, carries a structural disadvantage.

A Pattern That Repeats Every Cycle

Across major market crashes, whether in 2004, 2008, 2011, or more recently, retail investor behaviour has been strikingly consistent: panic at or near the bottom, hesitation at the start of the recovery, and then buying back in near the next top.

Historical examples from Indian markets illustrate this clearly:

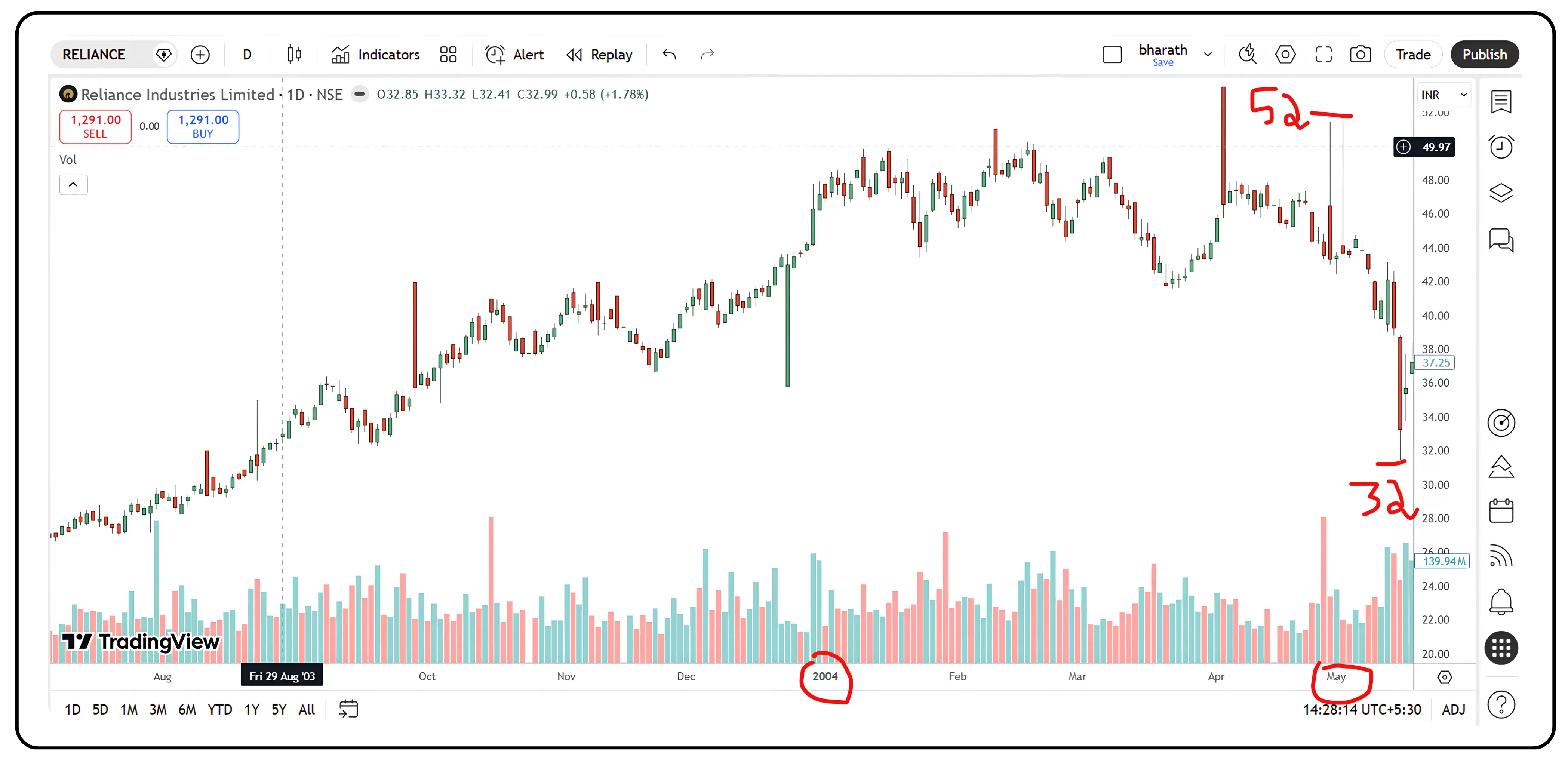

2004

The market was sideways for 4 months and shows classic distribution. Every rally was sold since Jan 2004.

When election results arrived and the market corrected sharply, nearly 40% in two trading sessions, those who had bought on hope and opinion polls that the BJP would resume power had already absorbed the distribution of those who had accumulated at the bottom.

2008

In 2008, markets topped before the real crisis fully unfolded. Prices began falling while optimism still lingered, but as major news like Lehman’s collapse hit the news in September 2008, panic selling took over. Retail investors exited in fear near the bottom, exactly when the worst news was already priced in, and long-term buyers quietly started accumulating and created a bottom in October. But by September 2008, the market had lost substantially, and the panic in September was used by smart investors to buy at the lows and create the bottom very next month.

2020

In March 2020, fear spread faster than the virus itself. As COVID lockdowns were announced across the world and economic activity came to a sudden halt, investors rushed to exit risk assets. Every bounce was met with fresh selling as uncertainty dominated sentiment. Following India's nationwide lockdown announcement on March 24, panic reached its peak, pushing markets into one of their fastest declines in history. Yet, as often happens in extreme fear-driven selloffs, the strongest hands began accumulating while the majority were still focused on the crisis unfolding around them. So the market bottomed out on the day of India’s lockdown when the COVID-19 case count in India was around 500. Before the larger public fathomed the magnitude of the impact of COVID, the market already discounted the damage and even bottomed out. So any retailer who would have sold after the March 24th lockdown is selling out at the bottom.

In each case, the sequence is the same: the market moves first. The news follows. Retail reacts to the news. Informed capital acts on what the price is already telling them.

Statistics Behind the Pattern

The pattern is not anecdotal. It is measurable. A widely cited figure in market circles suggests that roughly 90% of retail traders lose money over time. In India, SEBI's own study of equity futures and options traders found that over 89% of individual traders incurred losses in FY22 and FY23. The average loss per losing trader was approximately ₹1.1 lakh per year.

These numbers do not suggest that retail investors lack intelligence or discipline. They suggest something more structural: that most market participants are making decisions based on news, sentiment, and gut feel while the actual drivers of price movement play out in the price and volume data that sits on every chart, largely unexamined.

What This Means for the Individual Investor

Understand the cycle you are in: Fear and pessimism are historical companions of market bottoms. Euphoria and consensus optimism tend to arrive closer to tops.

Be cautious of acting on news as a primary signal: By the time a narrative is universally accepted, the market has often already priced it in or overpriced it.

Pay attention to price and volume behaviour: Distribution (selling into rallies) and accumulation (buying into weakness) are visible in market data before they become visible in headlines.

Separate emotional response from analytical response: The discomfort of acting against prevailing sentiment is often precisely what separates profitable decisions from costly ones.

The Real Insight

Markets are not random, but they are designed by their very nature to frustrate the majority. The crowd, seeking comfort, moves toward certainty: buying when the news is good, selling when the news is bad. The market, rewarding a different kind of discipline, tends to move against that comfort.

Understanding this dynamic does not guarantee outcomes. But it does offer something more durable than a hot tip or a trending headline: a framework for thinking about when the odds are more likely to be in your favour, and when they probably are not.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.