For years, the Indian power sector sat at the edges of a broader industrial story, often weighed down by legacy distribution challenges and coal dependency. That is beginning to change. A combination of forces that rarely align at the same time is now coming together. Global supply chains are transitioning towards clean energy, data centers and industrial expansion are demanding unprecedented base-load power, and closer to home, India is quietly putting massive capital, policy, and strategic intent behind building a resilient hybrid energy ecosystem. This is not a cyclical upswing driven by short-term tariffs. It is a structural shift.

Across the post-pandemic decade, few industries have been repositioned as deliberately as energy, and India's power sector is among the most consequential of these transformations. What was once viewed primarily as a utility service is now moving to the centre of industrial policy, backed by massive renewable capital expenditure, infrastructure expansion, and global decarbonisation mandates.

This report examines the structural drivers, policy environment, and competitive dynamics shaping India’s power and renewable energy industry.

Size and Structural Positioning

Of all infrastructure industries tied to economic growth, power generation carries among the highest capital intensity, the longest lead times, and the most concentrated policy focus. The global renewable energy capacity reached 585 GW in new additions in 2024, marking an annual increase of over 15%. Global renewable capacity is projected to grow by 2.7x, with 5,500 GW of new renewable capacity becoming operational by 2030.

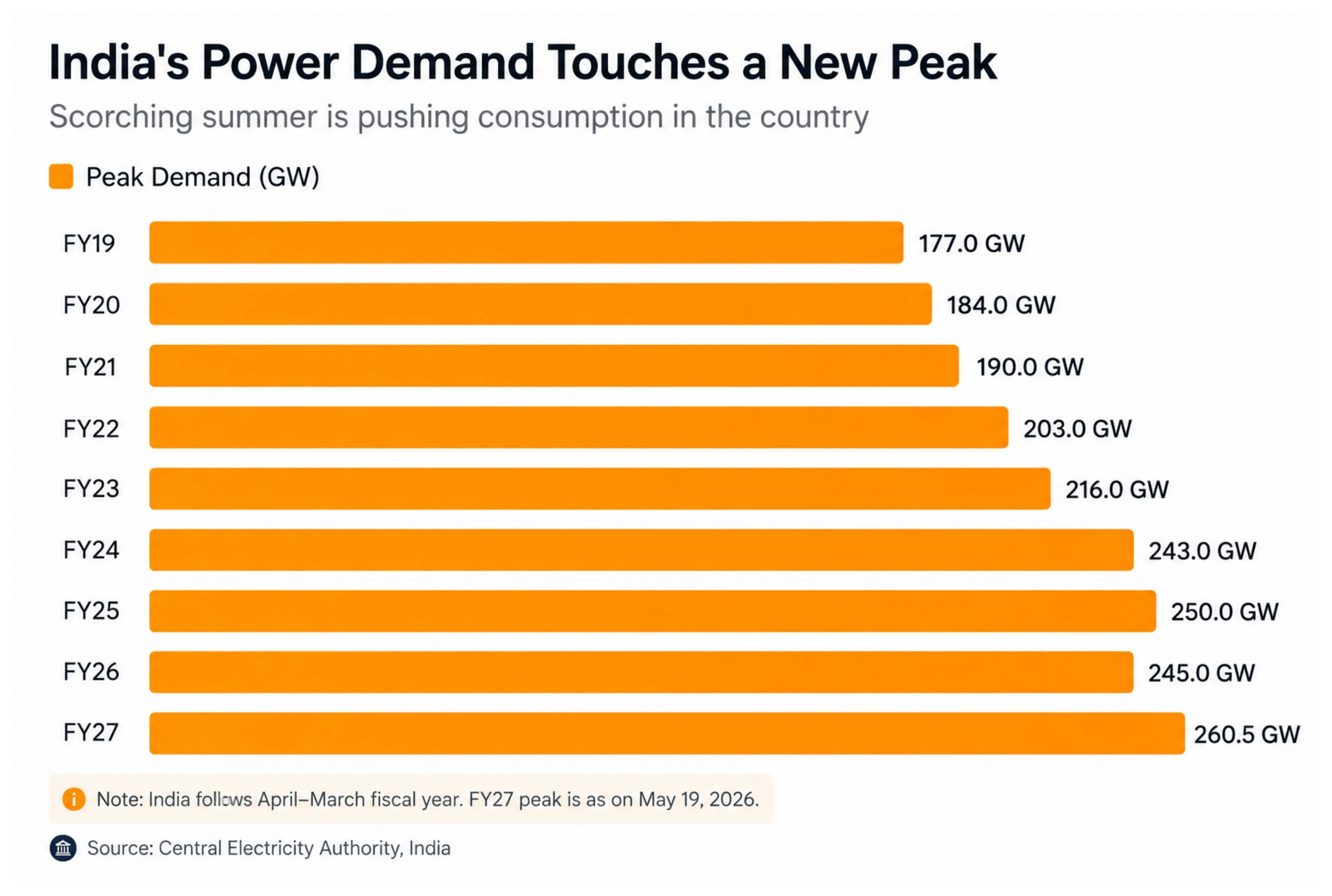

That growth trajectory understates the structural shift underway in India. Domestic electricity demand is expected to grow at a 5-6% CAGR over the next decade. In FY 2024-25, India’s peak energy demand reached 250 GW, and it is projected to hit 388 GW by FY32. India added an unprecedented 25 GW of renewable capacity in FY 2024-25 alone.

For nations seeking to build massive industrial and digital infrastructure, this concentration of power demand presents both the opportunity and the challenge: the requirement for uninterrupted power is absolute, and the cost and execution gap to deliver it is substantial.

Demand Trends and Global Tailwinds

Several distinct forces are converging to sustain capacity growth. Electrification and Industrialization stand out as the most non-discretionary drivers. As manufacturing hubs expand under the Production-Linked Incentive (PLI) scheme, and rural electrification reaches deeper penetration, base-load demand is soaring.

The rise of Data Centers reinforces this demand cycle. With artificial intelligence and cloud computing expanding rapidly, Indian data centers require massive, uninterrupted, and increasingly "green" power. This is forcing operators to sign long-term Corporate PPAs (Power Purchase Agreements) with renewable developers, creating a new, highly lucrative merchant and Commercial & Industrial (C&I) revenue stream independent of state discoms.

Furthermore, India has exhibited unwavering commitment to achieving its ambitious target of 500 GW of non-fossil fuel energy capacity by 2030. The policy architecture supporting this ambition is gaining tangibility. The Union Budget has significantly increased allocations for the Ministry of New and Renewable Energy (over ₹26,500 crore) and introduced 100% exemptions on Basic Customs Duty (BCD) for critical minerals like lithium and cobalt to directly accelerate India battery storage BESS deployment and pumped hydro storage development.

Also read: India Renewable Energy Sector & Stocks Outlook

Core Power Generators, Transmitters & Integrated Players

Adani Power Limited (APL)

As India's largest private thermal power producer, Adani Power base load supply provides the crucial grid-stabilising power that underpins national electricity reliability . The company is actively scaling its capacity to 30.67 GW through a mix of organic growth and acquisitions. Currently operating 18,150 MW of capacity, APL is pursuing an additional 30,000 MW of new coal-fired capacity. Despite the green transition, the government's projection of 80 GW of new thermal requirement by 2032 ensures strong long-term visibility, highlighted by recent moves like a 25-year PSA for 1,496 MW with MSEDCL.

Adani Green Energy Limited (AGEL)

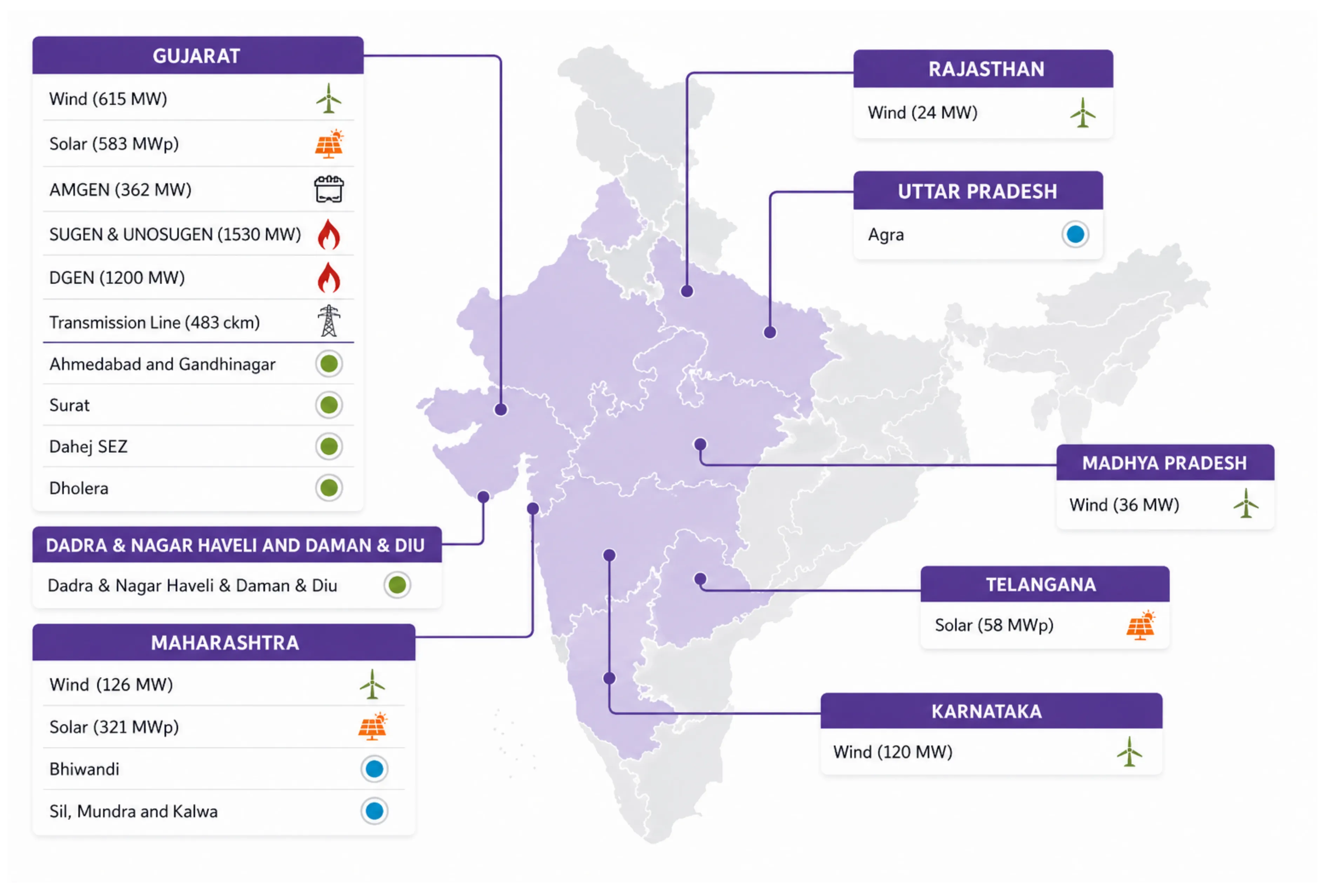

Any serious Adani Green Energy analysis must begin with its scale, India's largest pure-play renewable company, with an operational portfolio of 14.2 GW as of FY25 and a target of 50 GW by 2030 . AGEL is developing a massive 30 GW renewable energy plant at Khavda, Gujarat, the world's largest single-location power plant. With an industry-leading EBITDA margin of over 90 driven by advanced analytics via its Energy Network Operation Center (ENOC) and a 19-year amortising debt structure matching its PPA cashflows, AGEL sets a global benchmark for execution speed and operational efficiency.

Tata Power Company Limited

Tata Power, as a fully integrated utility, occupies a unique position spanning generation, transmission, distribution, and EPC. The company is aggressively scaling its clean energy footprint, including a partnership to develop 5,100 MW in Bhutan and 2,800 MW of pumped storage projects (Shirawata and Bhivpuri) set to commission by 2028. Additionally, its dominance in the EV infrastructure, its 4.3 GW cell and module manufacturing plant, and 100 MW BESS installations in Mumbai position the company to capture value across the entire hybrid power value chain.

JSW Energy Limited

JSW Energy has transitioned rapidly from a purely thermal generator to a hybrid energy player. With 13.3 GW of installed capacity and a massive under-construction pipeline, the company has recently upgraded its target to reach 30 GW of generation capacity and 40 GWh of energy storage by FY30. Driven by sector-leading organic wind additions and the 1,800 MW KSK Mahanadi acquisition, JSW's agile capital allocation is expected to deliver an FY30 EBITDA run-rate of 2.5x to 3.0x of its FY25 proforma EBITDA.

Torrent Power Limited

Operating as a highly efficient integrated utility, Torrent Power combines a generation capacity of 7,992 MWp (expected to grow to ~10.6 GWp) with lucrative franchisee distribution markets. The company is heavily targeting the Commercial & Industrial (C&I) sector with 815 MWp of dedicated projects and has a 3 GW Pumped Storage Hydro Project under development. Prudent financial management has allowed the company to improve its Net Debt to EBITDA ratio by 37% over the previous year, highlighting superior capital efficiency compared to state-owned distribution entities.

Power Grid Corporation of India Limited

As the backbone of India's electrical infrastructure, Power Grid operates approx 101 GW of inter-regional transmission capacity, representing roughly 84% of the country's total. The company is the critical enabler for integrating the massive renewable pipeline, expanding its network to support the nation's target of >600 GW non-fossil fuel capacity and ~71 GW of new demand from green hydrogen by 2032. Furthermore, POWERGRID is directly participating in the energy storage transition, recently securing a Letter of Award for a 150 MW / 300 MWh standalone BESS project.

For investors assessing Indian power stocks, the segments of pure-play renewables, integrated utilities, transmission monopolies, and thermal base-load providers require entirely different valuation frameworks, as their revenue drivers, margin structures, and risk profiles share little in common.

Comparative Peer Snapshot

| Company | Core Focus | Operational Highlights & EBITDA Trajectory | Capacity Target / Profile |

|---|---|---|---|

| Adani Green Energy | Pure-Play Renewable Energy | Consistently maintaining EBITDA margin above 90% | 50 GW target by 2030 (14.2 GW active) |

| Adani Power | Thermal Base-Load | Consolidated EBITDA of ₹10,893 crore in FY25 | 30.67 GW target (18,150 MW active) |

| Power Grid Corporation of India | Transmission | Dominates ~84% of India's inter-regional transmission capacity | Enabling over 600 GW renewable energy and 150 MW BESS |

| Tata Power | Integrated Power / Storage | Scaling 2,800 MW of high-margin pumped storage projects | 4.3 GW cell and module manufacturing plant |

| JSW Energy | Hybrid / Merchant Power | Targeting 2.5x–3.0x EBITDA growth by FY30 | 30 GW generation and 40 GWh storage by FY30 |

| Torrent Power | Distribution + Generation | Net Debt-to-EBITDA improved by 37% YoY | Operational capacity growing to 10.6 GWp |

Also read: Catching the Tailwind of Indian Shipbuilding Growth

Commodity Dependence and Cyclicality

The power sector's cost structure creates inherent margin vulnerability. For thermal generators like NTPC, coal availability and pricing remain the primary variables, though pass-through mechanisms in long-term PPAs largely insulate them from raw material shocks. However, for renewable developers like Adani Green and Tata Power, the cost of solar modules (largely imported from China) and wind turbines dictates capital expenditure. The recent Approved List of Models and Manufacturers (ALMM) mandate restricts the import of cheaper modules, forcing reliance on domestic manufacturing, which is still scaling up.

For companies with exposure to the short-term merchant market, cyclicality operates through power exchange rates rather than input costs. Earnings can be volatile, as peak demand deficits (like those seen during summer heatwaves) can drive exchange prices to the regulatory cap, yielding massive short-term cash flows, but reverting quickly when hydro generation picks up during the monsoon.

Distribution companies (and integrated players supplying to them) face a different form of cyclicality tied to state government finances. The most consequential financial characteristic of the sector is the length of the receivable cycle. Any investor analysis of this sector must treat receivable quality from state DISCOMs as the primary financial risk variable.

Long-Term Tailwinds

The sector carries structural tailwinds that extend well beyond a single investment cycle. Three are particularly durable:

1. India's 500 GW Non-Fossil Ambition is non-negotiable: The renewable pipeline has multi-decade visibility, creating a captive demand base for developers that is largely insulated from broader economic cyclicality.

2. Energy Storage Integration: As the grid greens, intermittency must be managed. The massive push for Pumped Storage Projects (PSP) and BESS ensures that the next leg of capital expenditure will yield high-margin infrastructure monopolies.

3. The Rise of the C&I Market: Corporate decarbonisation mandates are driving industries and data centers to bypass state utilities and buy power directly from developers, providing higher tariffs and zero default risk.

Against these tailwinds, a weak ancillary supply chain (specifically in solar cells and critical minerals for batteries) and the historical financial fragility of state distribution companies limit how quickly the sector realises its potential.

What unites these companies is the structural underinvestment in India's energy transition over the past decade, which is now being corrected with massive, targeted capital. The policy intent to close this gap is credible and increasingly funded. Whether execution matches the ambition over the coming decade is the operative question for anyone assessing this sector with a long horizon.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2026 — Tradejini. All Rights Reserved.