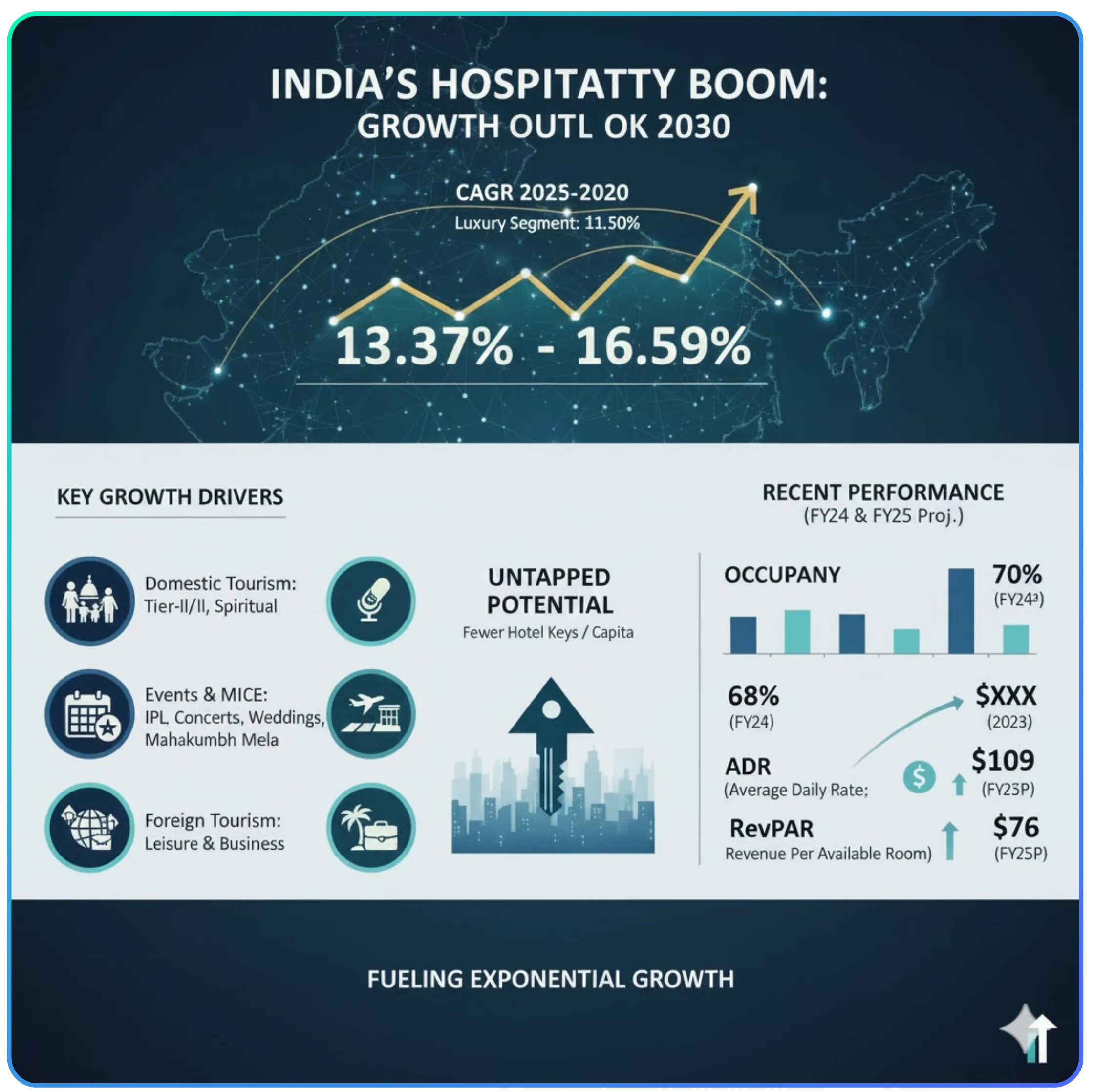

India’s hotel industry is experiencing robust growth, with projections showing strong double-digits CAGRs ( around 9-11% ) through 2030,driven by surging domestic leisure travel, large-scale events, improved connectivity, and increasing foreign tourist arrivals, leading to higher occupancy and average daily rates (ADR). While FY24 showed strong recovery, FY25 forecasts anticipate continued high occupancy ( around 70% ) and rising REvPAR ( Revenue Per Available Room ), with potential for exponential growth fueled by infrastructure and a massive untapped market for hotel keys.

Key Growth Drivers :

Domestic Tourism : A large population with increasing disposable income fuels demand, especially for Tier-II/III cities and spiritual destinations.

Events & MICE : Big events like the IPL, concerts, weddings, and the mahakumbh mela significantly boost occupancy.

Infrastructure : Better air connectivity and new convention centers support growth.

Foreign Tourism : Growing international interest in India for leisure and business.

Untapped Potential : India has significantly fewer hotel keys per capita compared to developed nations, indicating massive room for expansion. Forecast (CAGR 2025-2030):

Overall Market : 13.37% to 16.59%.

Luxury Segment : 11.50%.

Recent Performance ( FY 24 & FY 25 Projections ) :

Occupancy : Reached 68% in FY24, projected to hit 70% in FY25

ADR ( Average Daily Rate ) Saw significant jumps in 2023, with further increases expected in FY25 ( around ₹ 9800/- ).

RevPAR : Expected to rise to ₹6840 in FY25 from ₹ 5940 in FY24.

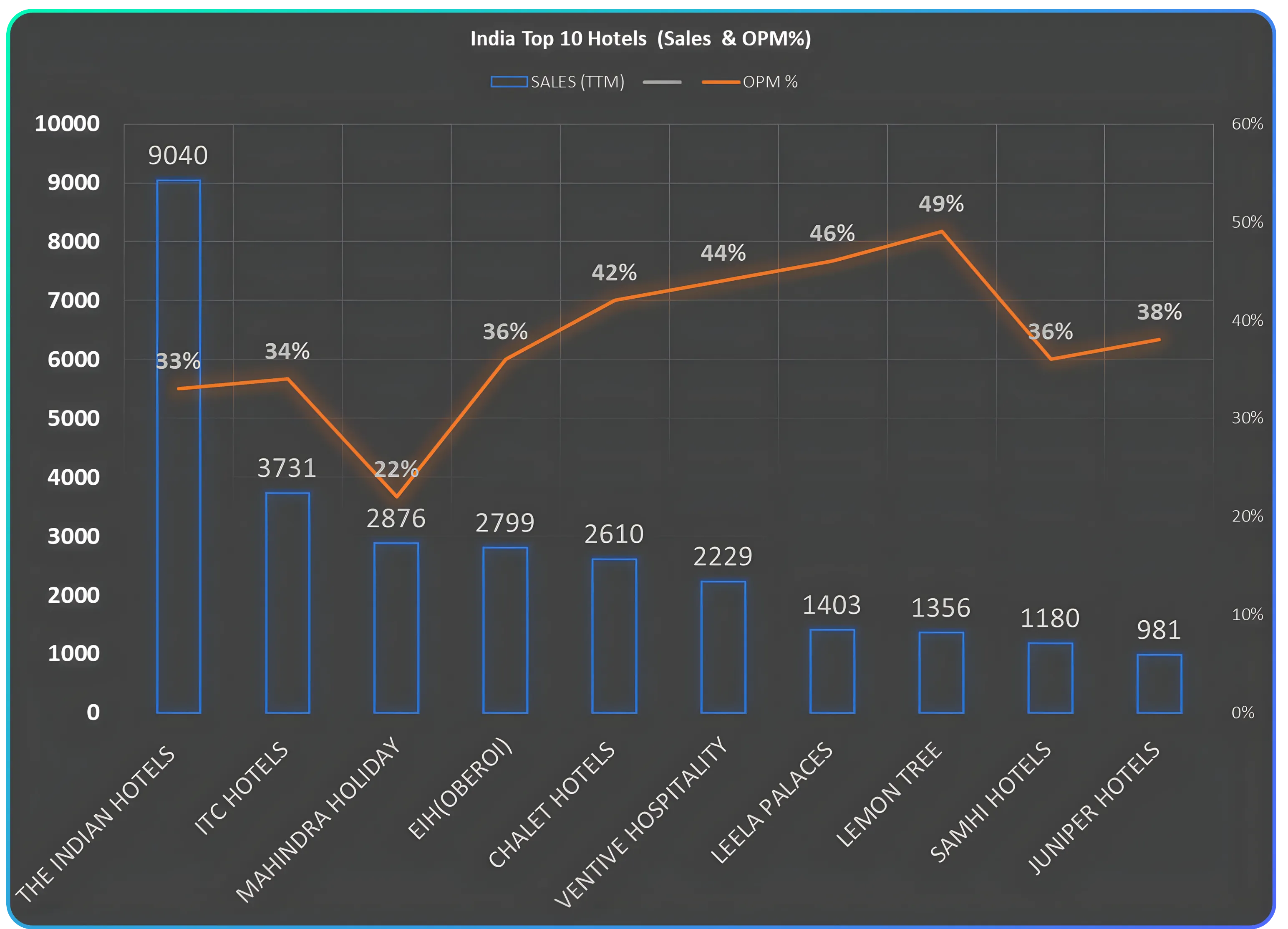

The Financial year Landscape of Indian Hospitality

This compelling visualization captures the financial pulse of India's top 10 hotel chains, offering a dual-lens view of their performance through Sales (TTM) and Operating Profit Margin (OPM%). The chart reveals a fascinating divergence between market share and operational efficiency. While revenue indicates the sheer scale and market footprint of industry giants, the OPM percentage peels back the layers to show who is actually managing their operations most profitably. From massive conglomerates to focused luxury players, this data highlights that in the hospitality business, being the biggest doesn't always mean being the most efficient. It sets the stage for a deeper look into how these brands balance top-line growth with bottom-line health in a competitive market.

Also read ABS Marine Anchoring Growth with Long-Term Offshore Contracts

Key Insights & Market Movers

Here are 7 interesting takeaways from the data that highlight the story behind the numbers:

- The Unrivaled Goliath: The Indian Hotels Company (Taj) is in a league of its own. With sales of 9,040cr, it generates more than double the revenue of its nearest competitor (ITC Hotels), cementing its status as the absolute market leader in terms of scale.

- The Efficiency Champion: Despite ranking 8th in total sales, Lemon Tree Hotels claims the crown for efficiency with a staggering 49% OPM. This proves that a leaner business model can often yield better profit margins than massive revenue streams.

- The "Sweet Spot" Mid-Tier: There is a distinct cluster of high performers—Chalet Hotels (42%), Ventive Hospitality (44%), and Leela Palaces (46%)—that maintain exceptionally high margins while operating with mid-range revenue, indicating premium positioning and tight cost controls.

- The Margin Dip: Mahindra Holiday presents a notable outlier with the lowest OPM at 22%. While their sales are strong (ranking 3rd), their operational costs appear significantly higher compared to their peers, creating a "V-shape" dip in the trend line.

- ITC vs. Oberoi (EIH): A battle of giants. While ITC Hotels leads significantly in sales (3,731 vs. 2,799), EIH (Oberoi) edges them out slightly in profitability margins (36% vs. 34%), showcasing the classic volume vs. value trade-off.

- Consistency at the Tail End: Even the smaller players by revenue, Samhi Hotels and Juniper Hotels, are maintaining healthy margins of 36% and 38% respectively. This indicates a generally healthy ecosystem where even the bottom of the top 10 is profitable.

- Revenue Concentration: The chart visualizes a "Pareto-like" distribution where the top player (Indian Hotels) holds a disproportionately large share of the total revenue pie compared to the gradual decline seen across the other nine competitors.

Also Read Control Print Ltd at the Center of India’s Coding and Marking Ecosystem

The Indian hospitality industry stands at an unprecedented inflection point, demonstrating remarkable resilience and growth potential that positions it among the world’s most dynamic hospitality markets. With revenue projected to exceed ₹5.2Lakhs cr by 2028 and occupancy rates surpassing pre-pandemic levels, India’s hospitality sector has not only recovered from the pandemic disruption but is experiencing a transformational expansion across multiple dimensions.

This comprehensive analysis examines the current performance metrics, growth trajectories, and strategic opportunities that define the modern landscape of Indian hospitality. From luxury resort developments to mid-scale branded hotels expanding into tier-2 cities, the sector’s evolution reflects broader economic trends, changing consumer preferences, and government initiatives that collectively drive sustained growth across various segments of the tourism and hospitality sector.

Market Overview and Current Performance

The hospitality industry has achieved remarkable performance metrics that underscore its robust recovery trajectory. Current data reveals that occupancy rates have reached 68%, marking a significant milestone that surpasses pre-pandemic levels and represents the highest occupancy figures in recent memory. This achievement reflects strong domestic demand coupled with recovering international visitation patterns.

Revenue performance indicators demonstrate equally impressive trends, with average daily rate growing 4.7% year-on-year while revenue per available room (RevPAR) has expanded by 5.7%. These metrics indicate not only volume recovery but also pricing power that hotels have successfully maintained despite increased supply in many markets. The combination of sustained occupancy with rate growth suggests healthy demand fundamentals across the sector.

International visitor spending reached a record Rs. 3.1 trillion in 2024, highlighting the sector’s ability to capture higher-yield international tourism segments. Foreign tourist arrivals are projected to reach 30.5 million by 2028, representing substantial growth potential for operators positioned to serve this premium segment. The recovery in international travel has been particularly beneficial for luxury and upper-upscale properties in gateway cities and iconic leisure destinations.

Monthly performance data from early 2025 shows occupancies reaching 72-74% in the first quarter, with RevPAR approaching ₹7,600 by February. This sustained momentum indicates that the recovery is not merely a temporary rebound but reflects structural demand improvements that support continued growth expectations across the hospitality sector.

Market Size and Growth Projections

The tourism industry presents compelling growth projections that position it as a critical economic sector for the next decade. Market analysis indicates the hospitality market will reach USD 45.40 billion by 2030, driven by an expected compound annual growth rate (CAGR) of 13.38%. This growth trajectory reflects both luxury segment expansion and accelerating digital sales channels that enhance market reach and operational efficiency.

Broader tourism industry estimates suggest the sector could reach $460 billion by 2028, encompassing hotels, restaurants, transportation, and related services. The hotel industry specifically is growing at 7% annually, while food and beverages segments are expanding at 10.4% per year. These differential growth rates highlight opportunities for operators with strong food and beverage operations to outperform pure accommodation-focused strategies.

Supply pipeline analysis reveals ambitious expansion plans, with a 58% increase in branded rooms over the next five years. This represents the first time in over a decade that the proposed supply of branded rooms has crossed the 100,000-room milestone. Branded hotels are slated to enter 177 new markets, indicating geographic diversification that extends hospitality infrastructure into previously underserved regions.

The scale of this expansion reflects investor confidence in long-term demand fundamentals, but also raises important questions about market absorption capacity and timing of new supply. Markets experiencing multiple simultaneous openings may face temporary rate pressure as new properties establish market position and build occupancy levels.

Key Market Segments and Consumer Trends

The luxury segment leads growth expectations with a projected CAGR of 12.13%, outpacing other segments and reflecting rising disposable incomes among India’s expanding affluent population. This growth is driven by both domestic luxury consumption and international visitor spending patterns that favor premium experiences and personalized service offerings.

Mid-scale chains including OYO and lemon tree hotels are expanding rapidly through asset-light models that enable faster market penetration without significant capital requirements. This approach has proven particularly effective in secondary cities where real estate costs are lower and local partnerships can facilitate market entry and operational scaling.

Spiritual and wellness tourism represents a rapidly growing segment, with destinations like Ayodhya attracting 110 million visitors in the first half of 2024. This demonstrates the massive scale of religious tourism and its economic impact on hospitality infrastructure. Wellness tourism specifically is gaining traction as consumers prioritize health and mindfulness experiences that combine traditional practices with modern amenities.

Consumer preferences are shifting toward authentic, wellness-focused experiences that prioritize personal well-being over traditional luxury markers. Gen Z travelers particularly prioritize sustainability credentials and seamless digital experiences throughout their journey. This generational shift influences hotel design, service delivery, and marketing strategies across all segments.

The rise in short, spontaneous leisure trips reflects changing work patterns and lifestyle preferences, while hybrid work-leisure stays (bleisure travel) have become mainstream. Industry surveys indicate that 92% of Indian respondents intend to combine work and leisure in their travel plans, creating demand for hotels that support both productivity and relaxation needs.

Also Read Why India could become the World’s Fastest-Growing Hospitality Market

Major Industry Players and Market Structure\

Independent hotels maintain significant market presence with 57.98% market share, despite ongoing consolidation trends that show chain properties growing at 10.76% CAGR. This market structure reflects India’s diverse hospitality landscape where independent operators continue to serve local markets while branded chains expand their geographic footprint and service standardization.

Indian Hotels Co. Ltd., operating Taj hotels and other premium brands, leads the domestic market through asset-light contracts and strong brand recognition. Their strategy emphasizes management agreements and franchising that enables expansion without heavy capital investment while maintaining brand standards and guest experience consistency.

OYO Hotels & Homes has focused expansion efforts on secondary cities through budget and mid-scale offerings that target price-sensitive travelers and business guests. Their technology-driven approach to operations and revenue management has enabled rapid scaling, though the company continues to refine its model for sustained profitability.

International chains including Marriott, Hilton, and Radisson hotel group are expanding through strategic partnerships with local developers and management agreements. These arrangements leverage global brand recognition and reservation systems while utilizing local market knowledge and development capabilities. Accor has similarly pursued expansion through a mix of management contracts and franchise agreements.

ITC Hotels emphasizes luxury positioning and sustainability initiatives that appeal to environmentally conscious premium travelers. Their integrated approach combines hotel operations with other ITC business segments, creating operational synergies and cross-marketing opportunities that differentiate their market position.

Lemon Tree hotels operates 116 properties with 10,700 rooms across the mid-scale market segment, demonstrating successful scaling in the practical business travel segment. Their standardized approach to mid-scale hospitality has proven effective in both metro and tier-2 city markets.

Regional Performance Analysis

West India leads revenue generation with 29.74% market share, benefiting from Mumbai’s status as the country’s financial hub and its concentration of corporate headquarters and high-value business travel. The region’s established airport infrastructure and road connectivity support both domestic and international visitor flows that sustain high occupancy and rate levels.

South India benefits from technology corridor demand, particularly in cities like Bengaluru and Hyderabad, where IT and business process outsourcing companies generate consistent corporate travel demand. Airport infrastructure expansions in the region support increased connectivity that facilitates both business and leisure travel growth.

North-East India shows emerging growth potential with improved connectivity through government infrastructure investments and the UDAN regional connectivity scheme. These developments are making previously inaccessible destinations viable for tourism development, though infrastructure and market development remain in early stages.

Tier-2 and tier-3 cities are receiving focused development attention through the union budget 2025 allocation of 2500cr for tourism destination development. This investment targets 100+ new tourist destinations with integrated infrastructure development that includes accommodation capacity and last-mile connectivity improvements.

Infrastructure projects like the Mumbai-Ahmedabad high-speed rail corridor are expected to drive regional growth by reducing travel times and creating new patterns of business and leisure travel. Such projects create opportunities for hotel development at intermediate stations and strengthen regional connectivity that supports tourism circuit development.

The government’s plan to invest ₹20,000 crore in developing 50 key tourist destinations represents substantial commitment to tourism infrastructure. These destinations are being positioned as world-class tourism hubs with integrated infrastructure that includes accommodation, transportation, and experience offerings designed to attract both domestic and international visitors.

Technology and Digital Transformation

Online travel agencies (OTAs) maintain significant market influence with 45.54% market share, while direct digital bookings are growing at 15.53% CAGR as hotels invest in customer relationship management and direct booking incentives. This dual trend reflects both the continued importance of third-party distribution and hotels’ efforts to build direct guest relationships.

AI-powered upselling and mobile payment systems are transforming the booking experience by enabling personalized offers and streamlined transaction processes. Hotels are implementing predictive analytics that anticipate guest preferences and automate room assignments, temperature controls, and service recommendations based on historical data and stated preferences.

Enterprise-wide customer relationship management systems and IoT-based energy management are improving operational efficiency while reducing costs. These systems enable hotels to optimize staffing levels, predict maintenance needs, and manage utility consumption based on occupancy patterns and guest behavior analytics.

Omni-channel guest experiences now include personalized recommendations, digital check-ins, and mobile-enabled service requests that reduce wait times and improve service consistency. The integration of these technologies allows hotels to deliver more personalized service while managing labor costs and improving staff productivity.

Technology platforms are enabling seamless connections between domestic operators and global hotel networks, facilitating brand standard implementation and reservation system integration. This technological integration supports the asset-light expansion model by ensuring operational consistency across diverse property types and geographic markets.

Also Read Q2 FY26 Performance Review of Entero, Senores, Acutaas, Alkem and Laurus

Industry Challenges and Barriers

Construction and fit-out costs have increased by 15-20% over recent years, creating pressure on development economics and project returns. Rising material costs, labor wages, and compliance requirements have extended project timelines and increased capital requirements for new hotel development, particularly affecting independent operators with limited access to capital.

High attrition rates of 20-25% across the hospitality sector create ongoing talent retention challenges that impact service quality and operational costs. Competition from other service industries, particularly technology and financial services, has intensified pressure on hospitality wages and benefits packages.

The 18% goods and services tax (GST) on premium rooms above INR 7,500 affects demand for luxury and MICE segments by increasing effective rates for corporate and leisure travelers. This tax structure creates pricing pressure on upper-end properties and may influence booking patterns toward lower-rated room categories.

Limited access to favorable financing remains a challenge for hotel development, with long project gestation periods and cyclical industry performance affecting lender appetite. Traditional bank financing for hospitality projects often requires substantial equity contributions and personal guarantees that limit development by smaller operators.

Capital-intensive sustainability investments in renewable energy and waste management systems require significant upfront expenditure with longer payback periods. While these investments improve long-term operating efficiency and brand positioning, they create near-term cash flow challenges for operators with limited capital resources.

Skilled talent is increasingly shifting to the gig economy and technology sectors, creating labor shortages and wage inflation pressure across operational roles. Training and retention of front-line staff becomes more challenging as alternative employment opportunities expand and worker expectations for flexibility and compensation increase.

Government Initiatives and Policy Support

E-visa expansion to 166 countries has simplified entry procedures for international visitors, reducing bureaucratic barriers and processing times that previously deterred tourism. This policy change particularly benefits leisure and business travel from key source markets in Europe, North America, and East Asia.

The government has invested Rs. 60 crore (USD 7 million) to develop 75 lighthouses and spiritual tourism infrastructure, recognizing the significant visitor draw of religious and cultural sites. This investment supports destination development that creates demand for nearby accommodation and related hospitality services.

Union budget 2025 allocated 2500cr for tourism destination development across 100+ new locations, representing substantial public sector commitment to tourism infrastructure. These investments include accommodation development, transportation connectivity, and visitor experience facilities that support private sector hospitality investment.

Regulatory liberalization has attracted global real-estate funds to the hospitality sector, increasing available capital for development and acquisition activities. Reforms to foreign direct investment policies and approval processes have reduced barriers to international investment and partnership arrangements.

The “Atithi Devo Bhava” cultural philosophy, meaning “guest is god,” supports broader hospitality industry growth by emphasizing service excellence and guest satisfaction as cultural values. Government marketing campaigns promote this philosophy internationally as part of destination India branding that benefits all hospitality operators.

Infrastructure status designation for hotels in 50 key tourist destinations provides access to longer-term, lower-cost financing that improves project economics. This policy change addresses one of the industry’s key challenges by improving capital access and project viability in priority destinations.

Economic Contribution and Employment Impact

The tourism and hospitality sector makes significant contributions to India’s gross domestic product through direct operations, taxes, and GST revenue generation. Industry estimates suggest the sector contributed approximately 5% of GDP in FY2023, with projections for continued growth as domestic tourism expands and international arrivals recover.

Theme parks alone employ over 80,000 people while generating 17.5% annual revenue growth, demonstrating the employment-intensive nature of entertainment and leisure segments. These operations create both direct employment in park operations and indirect employment in supporting services including hotels, restaurants, and transportation.

The food and drink sector, closely linked to hospitality operations, is estimated to reach 5.5 trillion rupees by 2022, highlighting the significant economic scale of F&B operations within hotels and standalone establishments. This segment’s growth creates employment opportunities across skill levels from kitchen staff to management positions.

Theme parks generated approximately 17 billion rupees annually before the pandemic, illustrating the substantial revenue potential of entertainment tourism. The recovery and expansion of this segment creates multiplier effects that benefit nearby hotels, restaurants, and related tourism services.

Employment opportunities across the hospitality sector are expected to increase significantly with continued expansion. Industry projections suggest employment could exceed 48 million jobs in 2025, growing to nearly 64 million by 2035 as the sector expands both domestically and through international visitor growth.

The sector provides employment opportunities across skill levels and educational backgrounds, making it an important source of inclusive economic growth. From housekeeping and food service to management and technical roles, the industry offers career advancement opportunities that support social mobility and regional development.

Future Outlook and Opportunities

Industry analysts expect the hospitality sector to grow at a CAGR of 10-12% over the next 3-5 years, driven by continued domestic market expansion and recovering international travel. This growth rate positions hospitality among India’s fastest-growing service sectors and creates substantial opportunities for operators, investors, and service providers.

Leisure destinations near metropolitan areas are leading growth opportunities as domestic travelers seek weekend and short-break destinations within driving distance of major cities. This trend supports resort development, alternative accommodation options, and experience-based tourism offerings in previously underutilized locations.

Market consolidation is accelerating with private equity firms targeting family-run assets for acquisition and professional management implementation. This trend creates opportunities for family-owned properties to access capital and management expertise while maintaining local market knowledge and relationships.

Alternative lodging platforms are expanding to cater to millennials and long-stay guests who prioritize authentic experiences and flexible arrangements over traditional hotel services. These platforms create new distribution channels and accommodation categories that serve evolving traveler preferences.

Sustainability credentials are becoming competitive differentiators rather than optional features, particularly for luxury and corporate segments. Hotels that invest early in renewable energy, waste reduction, and social sustainability programs gain competitive advantages in market segments that increasingly prioritize environmental and social responsibility.

The achievement of 100,000 branded rooms in the development pipeline for the first time in over a decade represents a milestone that demonstrates industry confidence and growth ambition. This expansion creates opportunities throughout the value chain from construction and design services to operations and management companies.

Strategic Implications for Industry Stakeholders

The Indian hospitality industry’s transformation from a recovery phase to sustainable growth creates multiple strategic opportunities for different stakeholder groups. Investors can capitalize on favorable demand-supply dynamics and government infrastructure investments, while operators can leverage technology adoption and asset-light expansion models to achieve efficient scaling.

Market data indicates that demand for premium hotels is expected to grow at 8-10% CAGR through FY2027-28, outpacing supply growth of 5-6% CAGR. This demand-supply gap supports pricing power and occupancy growth that benefits existing operators and creates attractive investment opportunities in well-positioned properties.

The expansion into tier-2 and tier-3 cities represents both opportunity and risk, as operators must balance growth ambitions with market development timelines and local competitive dynamics. Success in these markets requires understanding of local consumer behavior, appropriate service level positioning, and efficient operational models adapted to a smaller market scale.

Technology integration emerges as a critical success factor, with leading operators demonstrating how AI-powered revenue management, mobile-first guest experiences, and operational automation can improve both guest satisfaction and financial performance. The companies that effectively combine technology adoption with human service excellence are best positioned for sustained competitive advantage.

Sustainability investments, while requiring significant upfront capital, are increasingly necessary for competitiveness in premium segments and regulatory compliance. Early movers in renewable energy, waste management, and social sustainability programs can establish market leadership and operational cost advantages that compound over time.

The hospitality industry’s evolution reflects broader economic and social trends that position it as both a beneficiary and driver of India’s continued economic development. As rising disposable incomes, urbanization, and infrastructure improvements expand the addressable market, operators who successfully navigate current challenges while positioning for future growth opportunities will capture disproportionate value in this dynamic and expanding sector.

The convergence of domestic market maturation, international visitor recovery, government policy support, and technological advancement creates a unique set of conditions that favor sustained growth across multiple hospitality segments. For stakeholders who understand these dynamics and position accordingly, the Indian hospitality industry represents one of the world’s most compelling growth stories in the travel and tourism sector.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.