Definition & Core Mechanics

At its core, the Put Ratio Spread is a moderately bearish-to-neutral options trading strategy designed to profit from limited declines in the price of an underlying asset. The strategy involves buying one higher strike put and selling two lower strike puts of the same expiry. This configuration, often called a 1:2 put ratio spread, creates a net credit or near-zero-cost structure that allows the trader to benefit from slight downward moves while risking losses if the market collapses sharply.

Mechanically, it is a three-leg bearish options strategy:

- Buy 1 ITM/ATM Put (protection leg)

- Sell 2 OTM Puts (income legs)

- Same expiry date across all legs

The premium collected from the short puts often offsets the cost of the long put, creating a net credit or zero-debit entry. The position reaches its maximum profit when the stock closes near the strike of the short puts at expiry. Below that level, the losses grow exponentially as one of the short puts becomes uncovered.

Also Read: Call Ratio Spread Explained Through Real Trades

Unlike simpler spreads such as the Bear Put Spread, which limits both profit and loss, the Put Ratio Spread sacrifices downside protection in exchange for higher reward potential and lower entry cost. It’s a volatility trading strategy for traders who anticipate a controlled decline or range-bound behavior, rather than a crash.

The 1:2 ratio spread is the most common configuration because it balances premium generation with manageable margin exposure.

(Footnote: More aggressive traders occasionally use a 1:3 ratio, which amplifies both reward and risk.)

Structure and Objective

Structure (1:2 Put Ratio Spread):

- Buy 1 ATM/ITM Put at higher strike (e.g., ₹25,500 NIFTY Put)

- Sell 2 OTM Puts at lower strike (e.g., ₹25,600 NIFTY Puts)

- Same expiry date

Net Position: Typically results in a net credit or small debit.

Objective: To capitalize on a small to moderate decline in the underlying price while collecting option premiums. Profits come primarily from the time decay of options of sold puts and the narrowing difference between strike prices near expiry.

Deployment Conditions Table

| Feature | 1:2 Put Ratio Spread |

|---|---|

| Market View | Mildly bearish or range-bound; ideal when expecting a limited fall in price. |

| Implied Volatility (IV) | Best when IV is high but expected to decline. High IV allows richer premiums on the sold puts, improving credit received. |

| Use Case | Deployed before an event where volatility is elevated (e.g., earnings or policy announcements) and expected to normalize post-event. |

| Profit Zone | When the underlying settles around the short strike price at expiry. |

| Loss Scenario | Sharp crash below the lower strike causes theoretically unlimited loss. |

| Margin Requirement | High, since short puts expose the trader to downside assignment risk. |

Also Read: How to Dominate Volatility with Strip and Strap Strategies

Practical Example

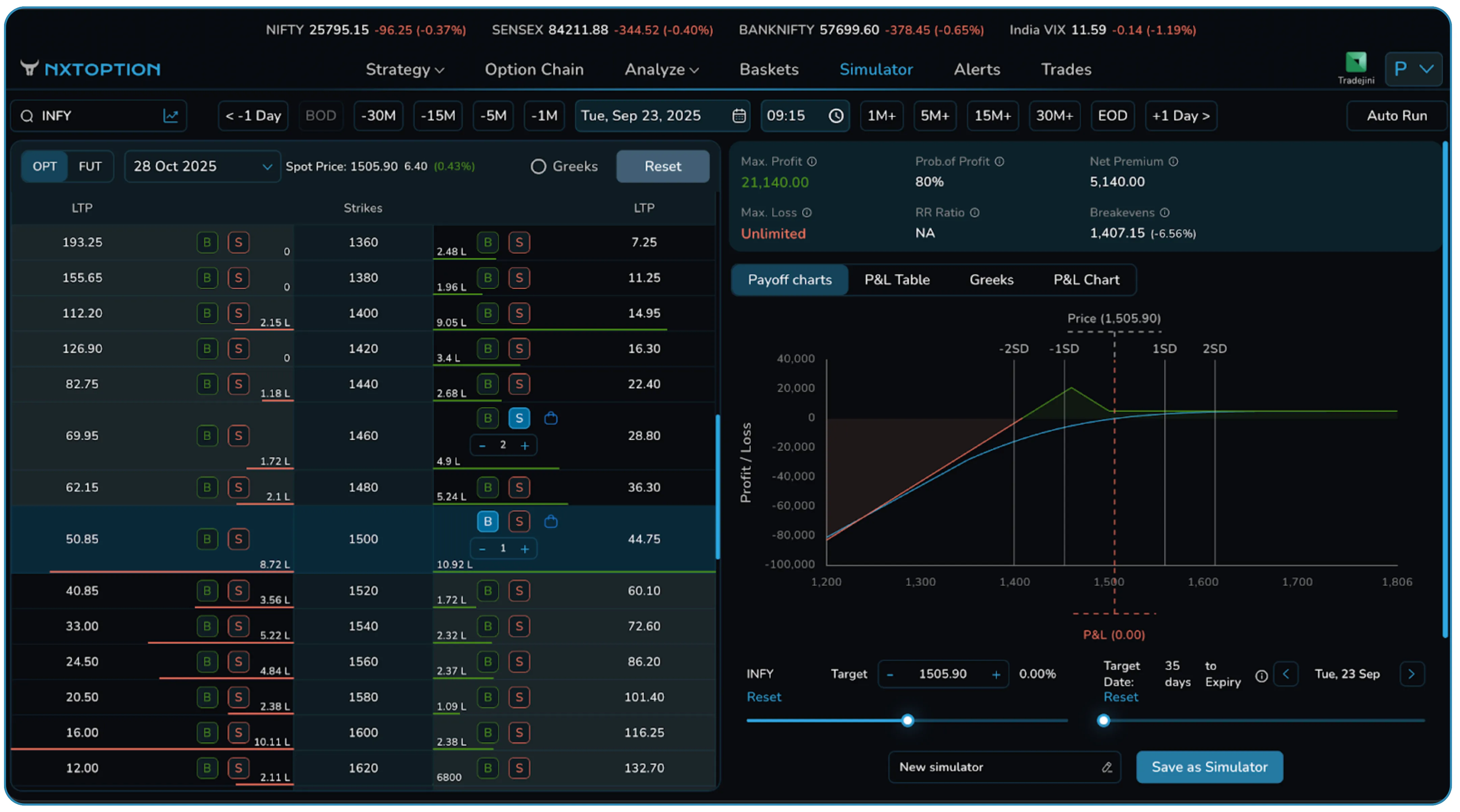

1:2 Put Ratio Spread with Infosys options

On 23rd September 2023, we entered into a put ratio spread position in Infosys which was trading at ₹1505.90 by trading in options expiring on 28th October Expiry.

Legs of the Strategy:

- Buy 1 INFY 1500 ATM Put at ₹44.75

- Sell 2 INFY 1460 OTM Puts at ₹28.80

Trade Metrics:

- Net Credit: ₹5,140

- Maximum Profit: ₹21,140.00

- Maximum Loss: Unlimited below ₹1,407.15

- Breakeven Point(s): ₹1,407.15

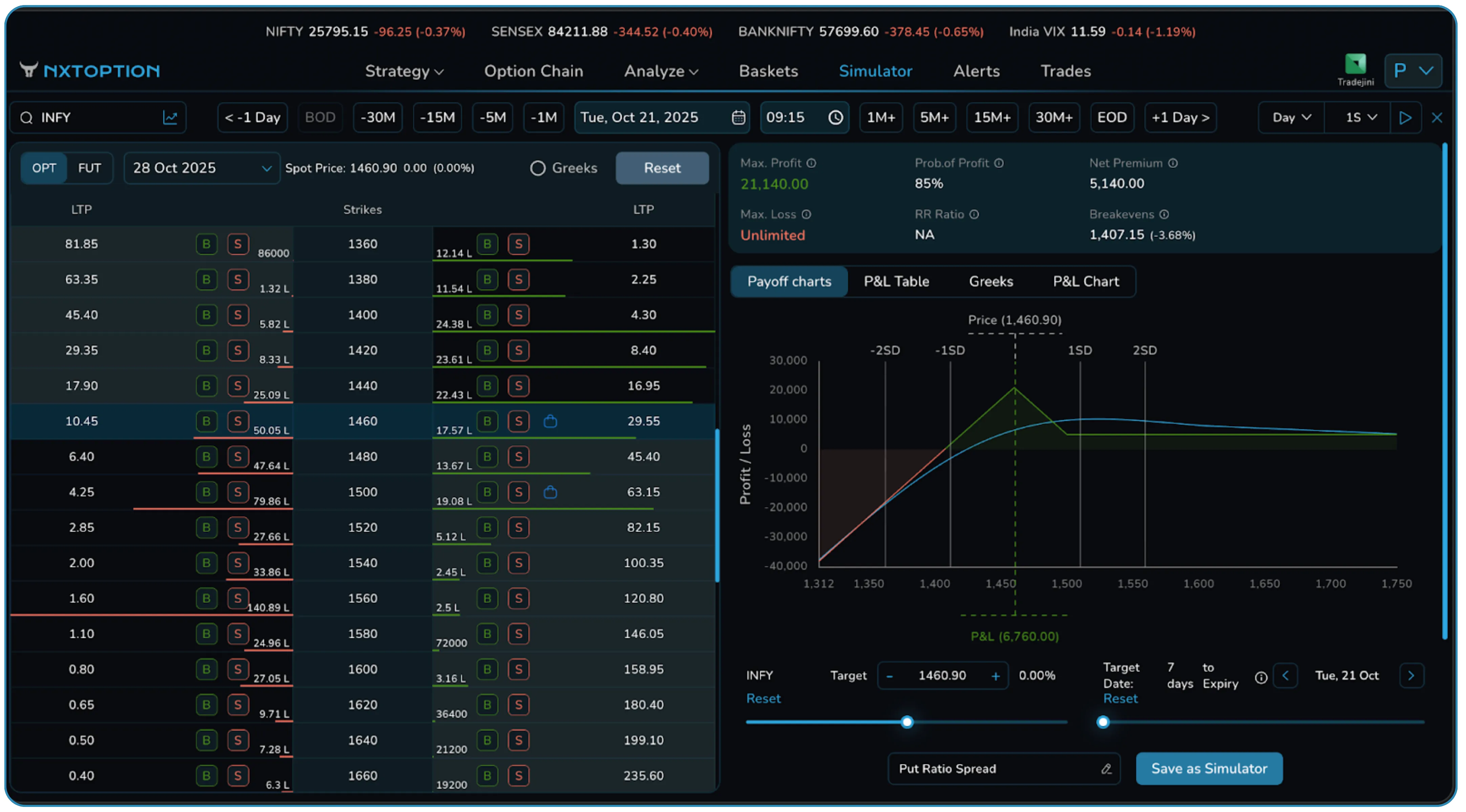

Outcome at exit:

- Exit Date: 21st October 2025 (7 days to expiry)

- Closing Price: ₹1,460.90

- Actual P&L: ₹6,760 profit

Analysis:

The setup performed as intended. The stock drifted downward from ₹1,505.90 to ₹1,460.90 landing near the short strike creating ideal theta-positive strategy conditions. The short puts (1460) lost value faster than the long 1500 put, allowing the positions to retain most of the premium as profit.

Implied volatility also compressed, adding further gains since the strategy was short vega. Profit peaked near the short strike validating the deployment when volatility has high and expected to decline. Had INFY breached ₹1,407, the losses would have increased rapidly, but controlled price movement made this trade successful.

Risk Management

Mitigation Techniques

Strike Selection: Choose short strikes 2–3% below the current price. Avoid clustering strikes too close; wider spacing reduces the probability of breaching the lower strike.

Exit Triggers: Close or adjust the spread if the underlying breaks below the short strike or if losses exceed 2x the premium collected. Alternatively, unwind once 70–80% of potential profit is realized.

Position Adjustment: Convert to a Bear Put Spread or roll down short puts to longer expiry if the trend continues.

Delta Hedge: For experienced traders, short futures or ETFs to neutralize further downside exposure.

Position Sizing: Allocate limited capital — no more than 5–10% of the portfolio — to avoid margin pressure from sudden drawdowns.

Market Condition Warnings

Avoid initiating a Put Ratio Spread:

- Ahead of major crash catalysts or uncertain global events

- When implied volatility is already very low (since premiums are poor)

- When you lack margin to handle assignment risk

Advanced Techniques

Professional traders use dynamic delta hedging and vega monitoring to maintain neutrality. Adjusting strike spacing based on real-time IV percentile data can also optimize credit-to-risk balance.

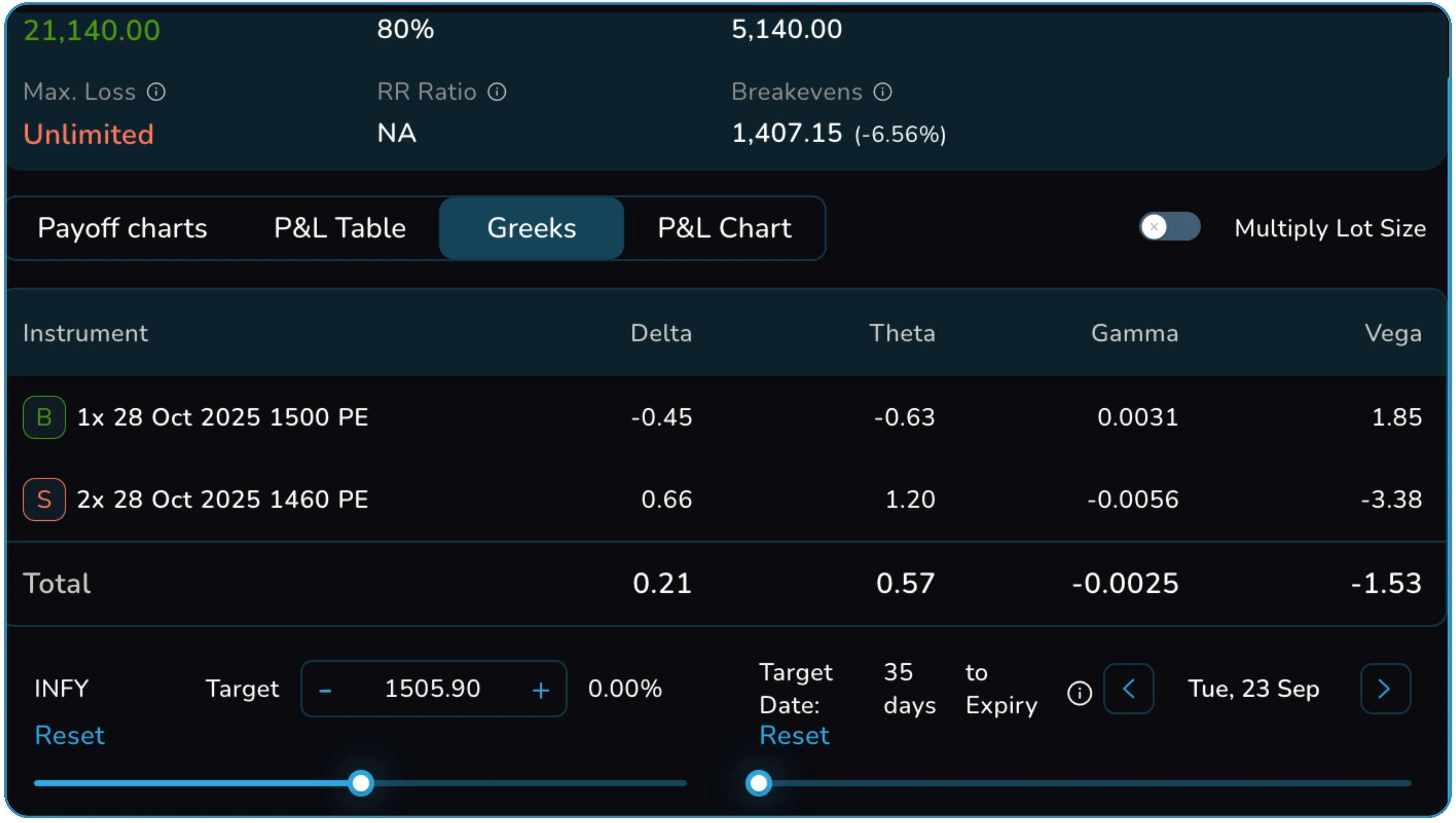

Greeks Interpretation

Delta

The strategy begins with a slightly positive delta (≈ +0.21), meaning it initially benefits from mild upward or stable price movements. This positive bias occurs because the sold puts (1460 strike) dominate the long 1500 put in quantity, producing a small bullish tilt at initiation.

However, as the price of INFY falls toward the short strike, delta gradually turns negative, aligning with a bearish bias near expiry. Below the breakeven of ₹1,407.15, delta accelerates further negative, magnifying losses.

To Know More About Delta Read: A practical guide for new traders learning Delta

Theta

The position is strongly theta-positive (+0.57), which is its main advantage. The two short puts generate more time decay than the single long put loses. Each passing day without major price movement adds to profit as premium erosion favors the net seller.

In the INFY trade, this effect was evident—the strategy gained steadily as time decay eroded the short options’ extrinsic value faster than the long put’s, particularly once the price hovered around ₹1,460.

To Understand How Theta Eats Into Option Premiums: Understanding Theta and the HIgh Cost of Time

Gamma

Gamma is slightly negative (–0.0025), which represents the main risk of the setup. Being net short gamma means the position’s delta will change unfavorably during rapid price swings. If INFY were to decline sharply, delta would turn heavily negative, amplifying losses. Conversely, in calm markets, low gamma benefits the trader by stabilizing the position and maintaining a predictable P&L curve.

Also Read: Beyond Delta a Practical guide to Understanding Gamma

Vega

Vega is negative (–1.53), indicating a short volatility exposure. The position profits when implied volatility falls, as it did during the INFY trade.

A drop in volatility reduces the value of all options, but since the trader is a net option seller, this works favorably. The opposite is true for volatility expansion, an unexpected spike in IV would temporarily inflate option premiums and cause unrealized losses.

Strategic Positioning

The Put Ratio Spread is a tactical tool for moderate bearishness with limited cost. It lies between a protective long put (high cost, limited loss) and a naked short put. The strategy requires precision and discipline, not aggression. It thrives when the market drifts, decays, or consolidates near a predictable support level.

Traders should approach it with the mindset of timing decay rather than chasing momentum. Its edge lies in correct strike spacing and volatility timing, not in predicting large directional moves. When volatility is inflated and expected to revert, this spread outperforms simpler bearish tools like the bear put spread or outright put buying.

However, it demands constant monitoring. While the entry may be credit-positive, the exit discipline determines survival,especially when a moderate fall turns into a crash.

Conclusion

The Put Ratio Spread, particularly the 1:2 configuration, represents a precision instrument in the options strategist’s toolkit. It allows profit from limited downside or stable conditions with minimal upfront cost, yet demands active vigilance due to asymmetric downside risk.

Before deploying, ask yourself:

- Am I expecting a small decline or a deep fall?

- Do I want time decay and volatility contraction working in my favor?

- Do I have the margin capacity to handle adverse assignment?

Understanding the Greek profile is non-negotiable. Theta and vega work for you, but gamma and delta can quickly turn against you if volatility spikes or prices collapse.

Used correctly, the Put Ratio Spread is a versatile, low-cost method to express tactical bearish views. Used carelessly, it becomes an uncovered short put in disguise.

Ready to take your options trading to the next level? Sign up with CubePlus today and explore how advanced option analytics work seamlessly on Nxtoption. Track Put Ratio Spread Payoffs, option Greeks, and real-time volatility trading strategies to optimize your trades and manage risk seamlessly. Start trading smarter with CubePlus now!

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.