Retirement planning in India is becoming more complex than ever. With rising life expectancy, soaring healthcare costs, and the gradual shift away from traditional family support systems, it's no longer as simple as saving a fixed sum and hoping for the best.. Yet, most working professionals underestimate how much money they actually need to retire comfortably. Many only plan for just 10-15 years after retirement, when in reality, they should be preparing for 25-30 years of retired life.

So, how much money do you need to retire in India? There is no one-size-fits-all answer, but this comprehensive guide will help you calculate your specific retirement corpus based on your current age, income, lifestyle, and retirement goals. We will walk you through proven calculation methods, real-life examples, and investment strategies to ensure you can maintain your desired standard of living throughout your golden years.

Quick answer: retirement corpus needed in India

Most Indians need anywhere between ₹3-8 crores to retire comfortably, depending on their lifestyle expectations and location. Here’s the quick framework for calculating your retirement corpus:

- Target 25-30 times your annual retirement expenses as your total corpus goal

- Plan for 25-30 years of post-retirement life with consistent 6-7% annual inflation

- Expect your monthly expenses to typically reduce to 70-80% of your pre-retirement income

- Set aside separate funds for healthcare (₹1-2 crores) and emergencies beyond basic living expenses

- Start early: A 30-year-old can save significantly less monthly than someone starting retirement planning at 40

Also Read: Types of Savings Accounts With Examples You’ll Relate To

The retirement calculator approach works best when you account for India-specific factors like higher healthcare inflation, changing family structures, and varying costs across different cities.

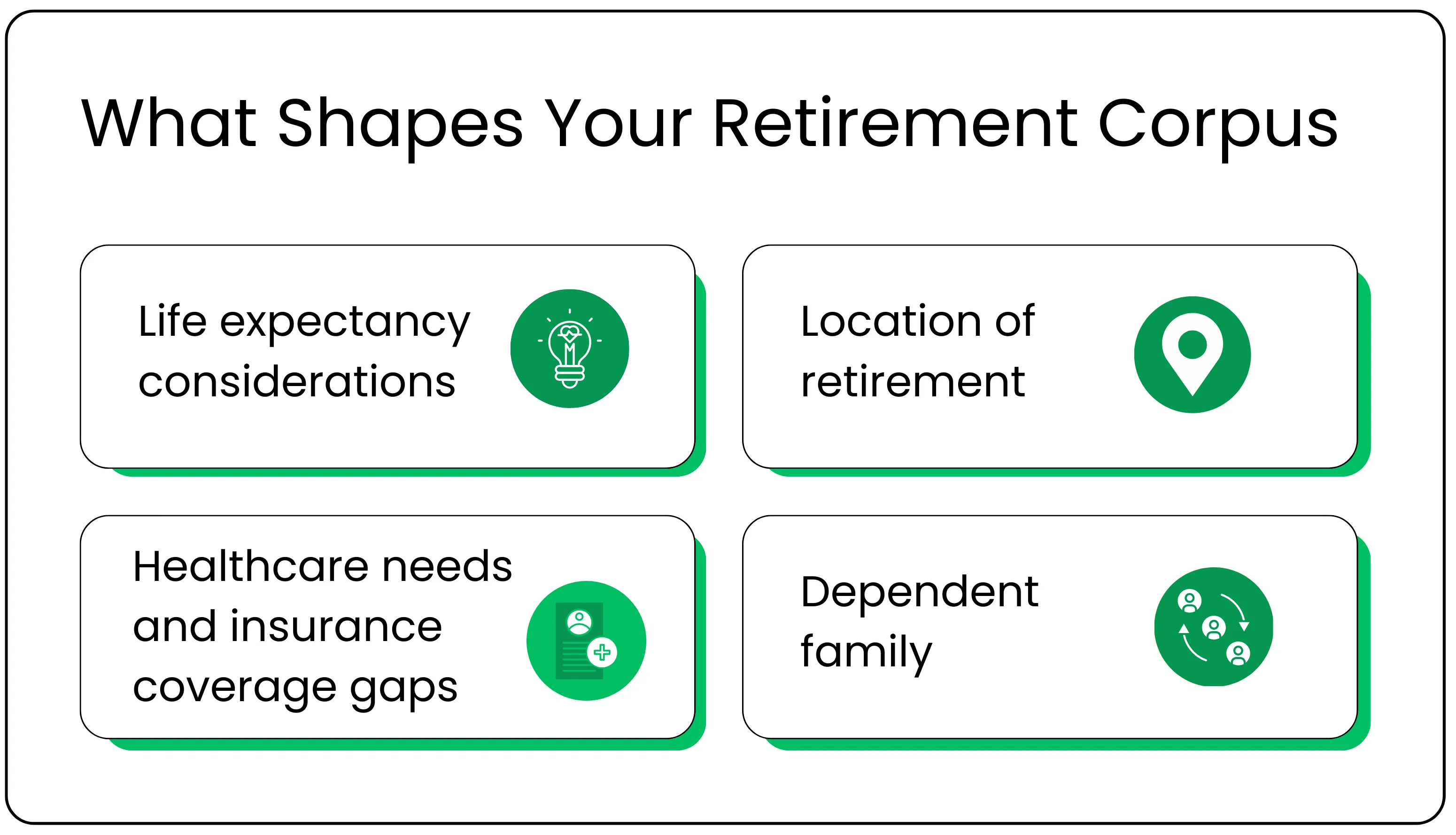

Your retirement corpus requirements depend on several interconnected factors that compound over time. Understanding these variables helps you create a more accurate estimate for your personal finance needs.

Current monthly expenses and expected lifestyle changes. Your present monthly expenses form the base of your retirement. Most financial planners recommend planning for 70-80% of your current expenses, as certain costs like children’s education, home loans, and daily commuting and work-related expenses tend to disappear after retirement age.

Inflation rate projections: Inflation plays a huge role in how much your money will be worth in the future. India’s historical inflation has averaged 6-7% annually, but healthcare costs inflate at 10-15% per year. This means your current monthly expense of ₹1 lakh could become ₹5.4 lakhs in 30 years at 6% inflation.

Life expectancy considerations: With improving healthcare, you should plan for living until 80-85 years, meaning a retirement span of 20-25 years if you retire early at 60. Some experts suggest planning for even longer to avoid outliving your retirement savings.

Location of retirement: Where you retire can dramatically affect your corpus requirements. Metro cities like Mumbai and Delhi require ₹6-10 crores for a comfortable retirement, while tier-2 cities might need ₹3-5 crores for the same lifestyle. Many retirees relocate to smaller cities to stretch their retirement benefits further.

Healthcare needs and insurance coverage gaps: One of the biggest risks to retirement security is rising healthcare costs. As you age, health insurance premiums increase substantially, and many policies stop covering pre-existing conditions after a certain age, requiring additional financial independence planning.

Dependent family members: Your retirement plan should also consider the financial needs of dependents. This could include aging parents, family members with special needs, or adult children who might need support during economic downturns.

Also Read: Lifestyle Inflation, the Hidden Cost of a Pay Raise

Step-by-step calculation method

Calculating how much money you need to retire in India requires a systematic approach that accounts for inflation, lifestyle changes, and investment returns. Follow this proven methodology used by financial planners across India.

Step 1: Calculate post-retirement monthly expenses

Start by analyzing your current monthly expenses and then determine what they will look like after retirement age. Take your present monthly spending and multiply it by 0.7-0.8 to apply the 70-80% rule.

Example calculation: If you currently spend ₹1 lakh per month, then plan for ₹70,000-80,000 in post-retirement expenses in today’s purchasing power.

Remove expenses that would not exist after retirement:

- Children’s education costs (assuming they are financially independent)

- Home loan EMIs (if paid off before retirement)

- Office commute and work-related expenses

- Professional clothing and equipment costs

Add new retirement-specific expenses:

- Increased healthcare and medical emergency costs

- Domestic help for daily activities

- Travel and leisure activities during active retirement years

- Potential long-term care assistance

Step 2: Adjust for inflation until retirement

Apply India’s projected inflation rate to calculate future expense values. For conservative retirement planning, use an annual inflation rate of 6-7%. Keep in mind that some categories, like healthcare, may require even higher estimates.

Inflation impact example: Current monthly expenses of ₹80,000 will become approximately ₹1.6 lakhs in 10 years, considering an inflation of 7% year-on-year. , ₹3.2 lakhs in 20 years, and ₹6.4 lakhs in 30 years.

The formula for future expenses is: Future Monthly Expense = Current Expense × (1 + Inflation Rate)^Number of Years

While online retirement calculators can help project these values accurately, understanding the manual calculation helps you appreciate the power of compounding inflation and its impact on your retirement corpus.

Step 3: Calculate the total corpus using the 4% withdrawal rule

The globally recognized 4% withdrawal rule suggests that you can safely withdraw 4% of your retirement corpus annually without depleting it. This translates to needing 25 times your annual retirement expenses as your total retirement corpus.

Example calculation: If your projected annual expenses at retirement are ₹19.2 lakhs (₹1.6 lakhs monthly), you would need a corpus of ₹4.8 crores using the 25X rule.

However, many Indian financial planners recommend a more conservative 30X multiplier, accounting for:

- Higher inflation volatility in emerging markets

- Longer life expectancy requiring extended retirement funding

- Unexpected healthcare costs and medical emergencies

- Market volatility affecting investment returns

It’s wise to add a 20-30% buffer to your calculated corpus, which will help cover unexpected expenses, market downturns, and peace of mind during your retired life.

Real-life examples by age and income

Understanding how retirement corpus calculations work in practice can help you benchmark your own retirement planning. These examples show how age, income, and savings timeline influence the monthly investment required to achieve a secure retirement.

30-year-old software engineer (₹15 LPA)

Current financial profile:

- Current monthly expenses: ₹60,000

- Target retirement expenses: ₹42,000 (70% of current, in today’s value)

- Years to retirement: 30 years

- Expected retirement age: 60

Retirement corpus calculation:

Let’s walk through the key numbers assuming 30 years to retirement and 7%

annual inflation:

- ₹42,000 becomes approximately ₹3.19 lakhs in 30 years at 7% inflation.

- Annual expenses: ₹20.16 lakhs

- Required corpus using 30X rule: ₹6.05 crores

Investment strategy needed:

To achieve the target corpus of ₹6.05 crores in 30 years, a smart and consistent investment approach is essential.

- Monthly SIP required: ₹25,000-30,000 in equity mutual funds

- Expected returns: 12-14% annually over 30 years

- Advantage: Long investment horizon allows higher equity exposure and compounding benefits

This example shows how starting early provides a significant advantage in retirement planning, requiring a manageable monthly investment despite the large corpus needed.

40-year-old mid-level manager (₹25 LPA)

Current financial profile:

- Current monthly expenses: ₹1.2 lakhs

- Target retirement expenses: ₹90,000 (75% of current)

- Years to retirement: 20 years

- Existing savings: ₹50 lakhs in various investments

Retirement corpus calculation:

- Monthly expenses at retirement (after 20 years of 7% inflation): ₹3.6 lakhs

- Annual expenses: ₹43.2 lakhs

- Required corpus: ₹12.96 crores using 30X rule

- Corpus still needed: ₹11-12 crores (accounting for existing savings growth)

Investment strategy needed:

- Monthly SIP required: ₹1,00,000-1,20,000 across mutual funds and other investments

- Portfolio allocation: 60-70% equity, 30-40% debt instruments

- Higher monthly investment compensates for a shorter time horizon

50-year-old senior executive (₹40 LPA)

Current financial profile:

- Current monthly expenses: ₹2 lakhs

- Target retirement expenses: ₹1.5 lakhs (75% of current)

- Years to retirement: 10 years

- Existing savings: ₹2 crores in EPF, mutual funds, and real estate

Retirement corpus calculation:

- Monthly expenses at retirement (after 10 years of 7% inflation): ₹3 lakhs

- Annual expenses: ₹36 lakhs

- Required corpus: ₹10.8 crores

- Additional corpus needed: ₹7-8 crores (after accounting for existing savings growth)

Also Read: Money Habits That Matter Before Teenage Years Begin

Investment strategy needed:

To build the additional corpus of ₹7–8 crores in 10 years, a carefully balanced and diversified investment approach is crucial.

- Monthly investment required: ₹1.5-2 lakhs across a diversified portfolio

- Portfolio allocation: 40-50% equity, 50-60% debt, and stable instruments

- Focus on capital preservation while achieving necessary growth

These examples demonstrate that while the corpus required seems daunting, systematic investing over time makes financial independence achievable across different income levels and ages.

Additional funds beyond the basic corpus

Your basic retirement corpus covers standard living expenses, but smart retirement planning includes separate funds for specific needs that could otherwise derail your financial security.

Healthcare emergency fund

Allocate ₹1-2 crores specifically for medical emergencies and long-term care needs, as healthcare inflation in India averages 10-15% annually, significantly outpacing general inflation.

Healthcare cost considerations:

- Health insurance premiums increase dramatically for senior citizens, often doubling every 5-7 years.

- Many insurance policies exclude pre-existing conditions or have sub-limits that become inadequate over time.

- Critical illness treatments can cost ₹10-50 lakhs, even with insurance coverage.

- Long-term care for conditions like dementia or mobility issues requires substantial ongoing investment for care and support.

Consider purchasing dedicated critical illness insurance and long-term care policies during your working years, when premiums are more affordable and coverage is easier to obtain.

Lifestyle and travel fund

Allocate an additional ₹50 lakhs to ₹1 crore for travel, hobbies, and lifestyle enhancements, especially during the early, active years of retirement. Many retirees want to travel extensively, pursue expensive hobbies, or maintain vacation homes.

Lifestyle planning factors:

- Travel costs inflate faster than general expenses, especially international travel.

- Hobbies like golf, photography, or adventure sports require ongoing equipment, memberships, and participation costs.

- Many couples want to maintain multiple residences or spend seasons in different locations, increasing housing and utility expenses.

- Social activities and entertainment costs may increase when you have more free time.

Legacy and family support fund

Plan for an additional corpus if you want to leave an inheritance for your children or support extended family members. This fund should also cover unexpected family financial emergencies.

Legacy planning considerations:

- The cost of a wedding for children or grandchildren continues rising due to social inflation, and families often feel compelled to meet cultural or societal expectations.

- Supporting higher education costs for grandchildren, especially international education, can require substantial financial commitments.

- Support for aging parents or in-laws who may not have adequate retirement savings or insurance coverage.

- An emergency fund for family members can provide financial relief in case of job loss, medical emergencies, or business failures.

This additional planning ensures your core retirement corpus remains intact while you can still provide family support when needed.

Investment strategy for retirement corpus

Building your retirement corpus requires a strategic investment approach that balances growth potential with risk management across different life stages.

Tax-advantaged investment vehicles:

- PPF (Public Provident Fund): A 15-year lock-in investment with tax benefits and guaranteed returns.

- EPF (Employee Provident Fund): Features employer matching with current returns of around 8-8.5%.

- NPS (National Pension System): Provides market-linked returns along with additional tax deduction up to ₹50,000.

- ELSS mutual funds: Equity-linked savings scheme with a 3-year lock-in period offering Section 80C tax benefits and equity growth potential.

Diversification across asset classes:

- Equity mutual funds: Target for 60-70% of portfolio during the accumulation phase for inflation-beating returns.

- Debt instruments: Include government bonds, corporate bonds, and debt funds for stability.

- Real estate: Consider REITs or direct property ownership, but limit to 20-30% of total portfolio.

- Gold and commodities: Allocate 5-10% allocation as an inflation hedge and portfolio diversifier.

Common investment mistakes to avoid:

- Over-reliance on traditional fixed deposits that fail to beat inflation

- Putting the entire retirement corpus in a single asset class or investment

- Ignoring the power of compounding by starting too late

- Not reviewing and rebalancing the portfolio annually based on market conditions and life changes

Regular monitoring and rebalancing ensure your retirement savings stay on track to meet your financial independence goals while managing risk appropriately for your age and risk appetite.

Common retirement planning mistakes to avoid

Even the most well-intentioned retirement plans can go wrong without awareness of these critical mistakes that could jeopardize your financial independence.

Underestimating inflation impact represents the biggest threat to retirement security. Many people calculate their retirement corpus using today’s expense values without properly accounting for 25-30 years of compounding inflation. What may seem like sufficient money today becomes insufficient when inflation erodes purchasing power over decades.

Healthcare cost miscalculation trips up many retirees who budget for general inflation but ignore that medical expenses inflate at 10-15% annually. This miscalculation can severely strain your retirement funds, especially in later years when medical needs tend to increase. A health emergency fund separate from your basic retirement corpus provides essential protection against this risk.

An over-conservative investment approach during the accumulation phase prevents many from building an adequate corpus. Keeping entire retirement savings in fixed deposits or traditional pension plans fails to generate inflation-beating returns necessary for long-term wealth creation.

Starting retirement planning too late forces people into impossible savings rates. Someone beginning serious retirement planning at 45 might need to invest 40-50% of their income to achieve the same corpus that someone starting at 30 could build with a 15-20% savings rate.

Ignoring a spouse’s financial needs and different life expectancy creates problems for surviving partners. On average, women live 3-5 years longer than men, requiring additional planning for extended retirement periods and potential single-person expenses. Not updating retirement plans based on salary increases, lifestyle changes, or family circumstances leads to inadequate corpus calculations. Review your retirement goals annually and adjust investments accordingly.

Failing to create separate emergency funds beyond the retirement corpus leaves you vulnerable to unexpected expenses that could force early withdrawal from long-term investments, disrupting your retirement planning timeline.

Retirement corpus by city

Where you choose to retire has a big impact on how much money you will need. Living costs can vary dramatically across Indian cities. Understanding these cost differences can help you in both corpus planning and potential relocation decisions.

Metro cities (Mumbai, Delhi, Bangalore, Chennai):

- Required corpus: ₹6-10 crores for a comfortable middle-class retirement

- Monthly expenses: ₹1.5-3 lakhs for a decent lifestyle, including housing, healthcare, and entertainment

- Advantages: Better healthcare facilities, cultural amenities, family proximity

- Disadvantages: Higher housing costs, air pollution, and traffic congestion

Tier-1 cities (Pune, Hyderabad, Ahmedabad, Kolkata):

- Required corpus: ₹4-7 crores, depending on specific location and lifestyle expectations

- Monthly expenses: ₹1-2 lakhs for comfortable living with good amenities

- Sweet spot: Offers a good balance of infrastructure, healthcare, and reasonable costs

Tier-2 cities (Indore, Jaipur, Kochi, Coimbatore):

- Required corpus: ₹3-5 crores for a middle-class lifestyle with domestic help and regular travel

- Monthly expenses: ₹60,000-1.2 lakhs for a comfortable lifestyle

- Advantages: Lower cost of living, less pollution, closer community connections

- Considerations: Limited access to healthcare specialties or advanced medical infrastructure and fewer entertainment options

Small towns and rural areas:

- Required corpus: ₹2-4 crores, especially advantageous if you own land or property

- Monthly expenses: ₹40,000-80,000 for a decent and comfortable lifestyle

- Benefits: Very low cost of living, peaceful and quiet environment, strong social connections

- Challenges: Limited access to quality healthcare facilities, dependency on nearby cities for specialized medical and lifestyle services

Strategic relocation planning: Many retirees successfully stretch their retirement corpus by moving from metros to tier-2 cities or their ancestral towns. This strategy can effectively increase your retirement corpus value by 30-50% while often improving your quality of life.

To make the most of this strategy, consider maintaining flexibility in your retirement plans, allowing you to take advantage of geographic arbitrage opportunities while ensuring access to quality healthcare and family connections.

Conclusion

So, how much money is needed to retire in India? Planning for retirement in India requires careful consideration of multiple factors, including inflation, healthcare costs, life expectancy, and location preferences. While the numbers may seem daunting, with most Indians needing between ₹3-8 crores for a comfortable retirement, systematic planning and early investment make these goals achievable.

The key to successful retirement planning lies in starting early, using the power of compounding through equity mutual funds and tax-advantaged instruments, and regularly reviewing your progress. Whether you are a 30-year-old just beginning your career or a 50-year-old accelerating your retirement savings, the principles remain the same: calculate your specific needs, invest systematically, and avoid common planning mistakes.

Remember that retirement planning is not just about accumulating money; it’s about ensuring financial independence and peace of mind during your golden years. Use retirement calculators to refine your estimates, consult with financial advisors for personalized strategies, and most importantly, start investing today rather than waiting for the ‘perfect’ time.

Your retirement should be a time of fulfillment and security, not financial stress. With proper planning and disciplined execution, you can build a retirement corpus that supports your desired lifestyle while providing the flexibility to handle unexpected challenges. The best time to start is now. Your future self will thank you for the strong financial foundation you build today.

Thinking of starting to invest? Begin with Tradejini’s CubePlus and start investing in equities, mutual funds, and more.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.